You might also like

- Lgu PFM Reform Roadmap and Implementation StrategiesDocument34 pagesLgu PFM Reform Roadmap and Implementation StrategiesJerdy Mercene100% (1)

- PFMAT For LGUs ConceptsDocument23 pagesPFMAT For LGUs ConceptsJosephine Templa-Jamolod100% (1)

- Public Financial ManagementDocument41 pagesPublic Financial ManagementDenalynn100% (1)

- Financing Philippine Local GovernmentDocument33 pagesFinancing Philippine Local GovernmentJUDY ANN GASPARNo ratings yet

- Local Fiscal Administration: Gilbert R. HufanaDocument27 pagesLocal Fiscal Administration: Gilbert R. Hufanagilberthufana446877100% (1)

- Public Fiscal Administration and Bureaucratic BehaviorDocument27 pagesPublic Fiscal Administration and Bureaucratic BehaviorCarmela Kim SicatNo ratings yet

- Public Debt ManagementDocument12 pagesPublic Debt ManagementKenneth Delos SantosNo ratings yet

- Public Debt and Fiscal Consolidation: A Closer Look at Public DebtsDocument7 pagesPublic Debt and Fiscal Consolidation: A Closer Look at Public DebtsVinn EcoNo ratings yet

- What Is Fiscal Administration?: Nonprofit Budgeting Fiscal ResponsibilityDocument11 pagesWhat Is Fiscal Administration?: Nonprofit Budgeting Fiscal ResponsibilityApril MaeNo ratings yet

- Public PoliciesDocument29 pagesPublic Policiessubhidra100% (1)

- Philippine Budget CycleDocument35 pagesPhilippine Budget CycleJetJet Linso100% (11)

- Fiscal AdministrationDocument8 pagesFiscal AdministrationMeg AldayNo ratings yet

- Introduction To Fiscal AdministrationDocument10 pagesIntroduction To Fiscal Administrationcharydel.oretaNo ratings yet

- What Is Government BudgetingDocument13 pagesWhat Is Government BudgetingVienna Mei Romero100% (7)

- The Philippine Budget CycleDocument4 pagesThe Philippine Budget CyclePalaboy67% (3)

- Public Policy Formulation SlidesDocument29 pagesPublic Policy Formulation SlidesMarliezel Sarda100% (1)

- Local Fiscal AdministrationDocument18 pagesLocal Fiscal AdministrationLander Dean S. ALCORANONo ratings yet

- INTRODUCTION TO PUBLIC FINANCE THEORYDocument36 pagesINTRODUCTION TO PUBLIC FINANCE THEORYelizabeth nyasakaNo ratings yet

- Philippine Budget ProcessDocument44 pagesPhilippine Budget Processfrancis ralph valdezNo ratings yet

- Management Accounting EssayDocument5 pagesManagement Accounting EssayvardaNo ratings yet

- Pfmat For Lgus-Part 1Document54 pagesPfmat For Lgus-Part 1Josephine Templa-Jamolod100% (2)

- Philippine Government Budget ProcessDocument48 pagesPhilippine Government Budget ProcessCarlo Ray Diase100% (3)

- Enhancing Participation in Local GovernanceDocument211 pagesEnhancing Participation in Local GovernanceDazzle Labapis100% (1)

- Topic 2.1 Budget Process Budget Prepartion Budget LegislationDocument24 pagesTopic 2.1 Budget Process Budget Prepartion Budget LegislationLeila Ouano100% (1)

- Public Fiscal AdministrationDocument119 pagesPublic Fiscal AdministrationWilson King B. SALARDANo ratings yet

- Property and Supply Management in The Local GovernDocument2 pagesProperty and Supply Management in The Local GovernMaria Angelica PanongNo ratings yet

- Local Fiscal AdministrationDocument12 pagesLocal Fiscal AdministrationJanice Aguila Suarez - Madarang100% (1)

- Narrative Local Fiscal AdministrationDocument6 pagesNarrative Local Fiscal AdministrationOliver SantosNo ratings yet

- What is Public Policy: Goals, Process & TypesDocument26 pagesWhat is Public Policy: Goals, Process & TypesRico EdureseNo ratings yet

- Lesson 3 Fiscal Administration and Policy RolesDocument5 pagesLesson 3 Fiscal Administration and Policy Rolesmitzi samsonNo ratings yet

- LGU BudgetingDocument14 pagesLGU BudgetingYasminNo ratings yet

- Budget ProcessDocument6 pagesBudget Processjd_prgrin_coNo ratings yet

- BudgetingDocument2 pagesBudgetingjhericz100% (2)

- What is Local Fiscal AdministrationDocument5 pagesWhat is Local Fiscal AdministrationOliver SantosNo ratings yet

- Understanding the National Budget ProcessDocument47 pagesUnderstanding the National Budget Processenaportillo13100% (9)

- Budget Process of The Philippine National GovernmentDocument3 pagesBudget Process of The Philippine National GovernmentMary Ann Tan100% (1)

- Public Fiscal Administration AssignmentDocument14 pagesPublic Fiscal Administration AssignmentJonathan Rivera100% (6)

- Public Fiscal AdministrationDocument21 pagesPublic Fiscal AdministrationNeal MicutuanNo ratings yet

- Philippine Public DebtDocument20 pagesPhilippine Public Debtmark genove100% (3)

- MODULE 1 Overview of Public Fiscal AdministrationDocument8 pagesMODULE 1 Overview of Public Fiscal AdministrationRica GalvezNo ratings yet

- Sources of RevenuesDocument6 pagesSources of RevenuesTabangz ArNo ratings yet

- Local Fiscal Administration & Resource Management PresentationDocument39 pagesLocal Fiscal Administration & Resource Management PresentationKen-ken Chua GerolinNo ratings yet

- Government Accounting and Budgeting Module at Don Mariano Marcos Memorial State UniversityDocument36 pagesGovernment Accounting and Budgeting Module at Don Mariano Marcos Memorial State UniversityErika MonisNo ratings yet

- Local Fiscal AdministrationDocument15 pagesLocal Fiscal AdministrationRoy Basanez100% (2)

- Government Accounting Ch1Document31 pagesGovernment Accounting Ch1John Evan Raymund Besid100% (1)

- Local Revenue GenerationDocument9 pagesLocal Revenue GenerationIsnihaya I. AbubacarNo ratings yet

- Chapter III: Managerial Approach To Government BudgetingDocument58 pagesChapter III: Managerial Approach To Government BudgetingkNo ratings yet

- Fiscal FunctionsDocument3 pagesFiscal FunctionsAshashwatmeNo ratings yet

- What Is Bottom-Up Budgeting?Document10 pagesWhat Is Bottom-Up Budgeting?Mikki Eugenio88% (16)

- Public Finance CourseoutlineDocument13 pagesPublic Finance CourseoutlineDuay Guadalupe Villaestiva0% (1)

- Week 1 .04 - Philippine Budgetary ProcessDocument70 pagesWeek 1 .04 - Philippine Budgetary ProcessElaineJrV-Igot100% (1)

- The Politics-Administration Dichotomy: Was Woodrow Wilson MisunderstoodDocument10 pagesThe Politics-Administration Dichotomy: Was Woodrow Wilson MisunderstoodPhương VõNo ratings yet

- Local Fiscal Administration: Prepared byDocument105 pagesLocal Fiscal Administration: Prepared byNathaniel DiazNo ratings yet

- Philippine Administrative SystemDocument42 pagesPhilippine Administrative SystemElanie LozanoNo ratings yet

- PFMAT For LGUsDocument101 pagesPFMAT For LGUssarahvelNo ratings yet

- Budget and Budgetary SystemDocument6 pagesBudget and Budgetary SystemunicornNo ratings yet

- PFMAT forLGUsDocument35 pagesPFMAT forLGUsbaningssNo ratings yet

- Pfmat IntroDocument12 pagesPfmat IntroBernNo ratings yet

- 3-Slides Session 1.0 UACS Foundation of PFM Oct2014Document46 pages3-Slides Session 1.0 UACS Foundation of PFM Oct2014Husni HamsijaniNo ratings yet

- Procurement Service - Philippine Government Electronic Procurement SystemDocument1 pageProcurement Service - Philippine Government Electronic Procurement SystemEarthAngel OrganicsNo ratings yet

- DBM 86th Anniversary Celebration ProgramDocument1 pageDBM 86th Anniversary Celebration ProgramEarthAngel OrganicsNo ratings yet

- PART I - DEPOT OPERATIONS-converted As of December 2019Document41 pagesPART I - DEPOT OPERATIONS-converted As of December 2019EarthAngel OrganicsNo ratings yet

- MPhilGEPS Training Presentation - v2Document19 pagesMPhilGEPS Training Presentation - v2EarthAngel OrganicsNo ratings yet

- (Letterhead of The Procuring Entity) : RESOLUTION NO. PB14-023-001Document2 pages(Letterhead of The Procuring Entity) : RESOLUTION NO. PB14-023-001EarthAngel OrganicsNo ratings yet

- Performance Review and Evaluation Form: Total RatingDocument2 pagesPerformance Review and Evaluation Form: Total RatingEarthAngel OrganicsNo ratings yet

- UACS Object CodeDocument42 pagesUACS Object CodeEric Luis CabridoNo ratings yet

- CS Form No. 212 Attachment - Work Experience SheetDocument2 pagesCS Form No. 212 Attachment - Work Experience SheetEarthAngel OrganicsNo ratings yet

- TRAIN PresentationDocument17 pagesTRAIN PresentationApril Mae Niego MaputeNo ratings yet

- Briefer - PS Depot - Revised - 3Document49 pagesBriefer - PS Depot - Revised - 3EarthAngel OrganicsNo ratings yet

- Office Order No. 207, S. 2022Document21 pagesOffice Order No. 207, S. 2022EarthAngel OrganicsNo ratings yet

- Memorandum No. NGY 20-166 Guidelines On The Grant of Year-End Bonus and Cash Gift For FY 2020Document3 pagesMemorandum No. NGY 20-166 Guidelines On The Grant of Year-End Bonus and Cash Gift For FY 2020EarthAngel OrganicsNo ratings yet

- SEC-PSE - Press Release - Q3 2020 PerformanceDocument9 pagesSEC-PSE - Press Release - Q3 2020 PerformanceEarthAngel OrganicsNo ratings yet

- PhilGEPS Orientation For Merchants - UpdatedDocument22 pagesPhilGEPS Orientation For Merchants - UpdatedEarthAngel OrganicsNo ratings yet

- COA - C2017-001 - Expenses Below 300 Not Requiring ReceiptsDocument2 pagesCOA - C2017-001 - Expenses Below 300 Not Requiring ReceiptsJuan Luis Lusong100% (3)

- CSC-COA-DBM Joint Circular Amended on Contract WorkersDocument2 pagesCSC-COA-DBM Joint Circular Amended on Contract Workersrenz100No ratings yet

- Investing in Small Cap Stocks Explained (Definition, Indexes, Strategy, Risks & FTSE ExampleDocument10 pagesInvesting in Small Cap Stocks Explained (Definition, Indexes, Strategy, Risks & FTSE ExampleJulian KrujaNo ratings yet

- Press Release Pag-IBIG Lowers Mandatory Contribution Makes MembershipDocument1 pagePress Release Pag-IBIG Lowers Mandatory Contribution Makes MembershipEarthAngel OrganicsNo ratings yet

- New Barangay Budget Review 5-28-14Document16 pagesNew Barangay Budget Review 5-28-14EarthAngel OrganicsNo ratings yet

- Application of The Unfairness Doctrine To Marketing CommunicationsDocument8 pagesApplication of The Unfairness Doctrine To Marketing CommunicationsEarthAngel OrganicsNo ratings yet

- Coaching ConversationDocument2 pagesCoaching ConversationEarthAngel OrganicsNo ratings yet

- Connecting Plans To The Budget - 2014Document91 pagesConnecting Plans To The Budget - 2014EarthAngel OrganicsNo ratings yet

- CSC Resolution No. 1500088 Sworn Statement of Assets FormDocument4 pagesCSC Resolution No. 1500088 Sworn Statement of Assets Formwyclef_chin100% (6)

- Coaching ScenariosDocument1 pageCoaching ScenariosEarthAngel OrganicsNo ratings yet

- DBM Dilg Joint Memorandum Circular (JMC) No. 2019 2 Dated December 18, 2019Document15 pagesDBM Dilg Joint Memorandum Circular (JMC) No. 2019 2 Dated December 18, 2019c lazaroNo ratings yet

- 2 PhilGEPS UpdatesDocument31 pages2 PhilGEPS UpdatesEarthAngel OrganicsNo ratings yet

- THE BUDGET CYCLE: WHEN DOES THE BUDGET AUTHORIZATION PHASE BEGINDocument40 pagesTHE BUDGET CYCLE: WHEN DOES THE BUDGET AUTHORIZATION PHASE BEGINEarthAngel OrganicsNo ratings yet

- Budget Preparation Working Paper-HonorariumDocument120 pagesBudget Preparation Working Paper-HonorariumEarthAngel OrganicsNo ratings yet

- Connecting Plans To The Budget - 2014Document91 pagesConnecting Plans To The Budget - 2014EarthAngel OrganicsNo ratings yet

- PART I - DEPOT OPERATIONS-converted As of December 2019Document41 pagesPART I - DEPOT OPERATIONS-converted As of December 2019EarthAngel OrganicsNo ratings yet

- Factors Affecting Audit Firms Rotation Jordanian CaseDocument20 pagesFactors Affecting Audit Firms Rotation Jordanian CaseSarah FawazNo ratings yet

- Freshasia Foods LTD Profit & Loss (With Prior Year Values)Document2 pagesFreshasia Foods LTD Profit & Loss (With Prior Year Values)Anonymous wgslM3koNo ratings yet

- Meralco Internal ControlDocument4 pagesMeralco Internal ControlLalaine De JesusNo ratings yet

- Regional Mock Board Examination 2019: General GuidelinesDocument12 pagesRegional Mock Board Examination 2019: General GuidelinesXyzzielleNo ratings yet

- IPCC Auditing NotesDocument17 pagesIPCC Auditing NotesAshish Bhojwani50% (4)

- Internal Controls Exam ReviewDocument63 pagesInternal Controls Exam ReviewQuynh AnhNo ratings yet

- Regas and GilesDocument5 pagesRegas and GilesAtira BahrunNo ratings yet

- Transmittal Letter CoaDocument1 pageTransmittal Letter CoaJanine PigaoNo ratings yet

- ADGM General Rulebook GENDocument114 pagesADGM General Rulebook GENAdrin AshNo ratings yet

- Philippine Contractor's License Application RequirementsDocument25 pagesPhilippine Contractor's License Application RequirementsAljohn SebucNo ratings yet

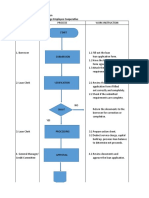

- Process Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeDocument4 pagesProcess Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeJao FloresNo ratings yet

- ACCT1AB Chapter 1 PDFDocument3 pagesACCT1AB Chapter 1 PDFErica Jane Garcia DuqueNo ratings yet

- Ledger Accounting and Double Entry Bookkeeping: Chapter Learning ObjectivesDocument46 pagesLedger Accounting and Double Entry Bookkeeping: Chapter Learning Objectiveskoti kebele100% (1)

- Pertemuan #8Document35 pagesPertemuan #8Daniel Pandapotan MarpaungNo ratings yet

- Tatenda Jasi CVDocument4 pagesTatenda Jasi CVAnonymous Z1hrD6IowNo ratings yet

- About ASA PhilippinesDocument5 pagesAbout ASA PhilippinesjolinaNo ratings yet

- Internal Audit For Finance SectorDocument1 pageInternal Audit For Finance SectorSURYA SNo ratings yet

- C3 Ethics, Fraud, and Internal ControlDocument12 pagesC3 Ethics, Fraud, and Internal ControlLee SuarezNo ratings yet

- Apex Foods Limited Annual Report 2019-20Document75 pagesApex Foods Limited Annual Report 2019-20Neamul hasan AdnanNo ratings yet

- Chennai Institute Controlling ProcessDocument22 pagesChennai Institute Controlling ProcessManimegalaiNo ratings yet

- CLA215 - FASB, Statement of Financial Accounting Concepts No 6Document58 pagesCLA215 - FASB, Statement of Financial Accounting Concepts No 6Eric Lie100% (1)

- Risk AssessmentDocument34 pagesRisk AssessmentIrfan AriellaNo ratings yet

- Delima ReportDocument16 pagesDelima ReportEstrada Alf100% (7)

- Accountancy FirmDocument2 pagesAccountancy FirmAarti SarafNo ratings yet

- Listing Agreement - BseDocument7 pagesListing Agreement - BseBhavyesh JainNo ratings yet

- Bill Snow Financial Model 2004-03-09Document35 pagesBill Snow Financial Model 2004-03-09nsadnanNo ratings yet

- Eslao vs. Commission On AuditDocument18 pagesEslao vs. Commission On Auditvince005No ratings yet

- Audit Evidence AssignmentDocument15 pagesAudit Evidence Assignmentakber62No ratings yet

- The key elements of management control systems according to Kenneth MerchantDocument15 pagesThe key elements of management control systems according to Kenneth MerchantAntora HoqueNo ratings yet

- Types of Internal ControlsDocument12 pagesTypes of Internal Controlsshazana_ak100% (5)