You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- I405 80HrClosure MapDocument1 pageI405 80HrClosure MapPatrick LeeNo ratings yet

- LASD - Obstruction IndictmentDocument18 pagesLASD - Obstruction IndictmentPatrick LeeNo ratings yet

- Charged Up: Southern California Edison's Key Learnings About Electric Vehicles, Customers and Grid ReliabilityDocument7 pagesCharged Up: Southern California Edison's Key Learnings About Electric Vehicles, Customers and Grid ReliabilityPatrick LeeNo ratings yet

- War of The Welles PDFDocument15 pagesWar of The Welles PDFPatrick Lee100% (1)

- Covered California: Health Plans & Rates For 2014Document86 pagesCovered California: Health Plans & Rates For 2014Tim McGheeNo ratings yet

- Integrated Voter EngagementDocument48 pagesIntegrated Voter EngagementPatrick LeeNo ratings yet

- DORNER Dispatch LogsDocument30 pagesDORNER Dispatch LogsGina DvorakNo ratings yet

- Mahony Statement On PopeDocument2 pagesMahony Statement On PopePatrick LeeNo ratings yet

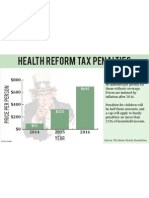

- Health Reform Tax PenaltiesDocument1 pageHealth Reform Tax PenaltiesPatrick LeeNo ratings yet

- LAPD Chief Charlie Beck's Statement On Ex-Officer-Turned-Fugitive Christopher DornerDocument1 pageLAPD Chief Charlie Beck's Statement On Ex-Officer-Turned-Fugitive Christopher DornerLos Angeles Daily NewsNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 3.NPER Function Excel Template 1Document9 pages3.NPER Function Excel Template 1w_fibNo ratings yet

- Types of Transaction: Being Name of Person's Cheque Returned ChequeDocument2 pagesTypes of Transaction: Being Name of Person's Cheque Returned ChequeDipendra GiriNo ratings yet

- BBL Cheque Book Authorization LetterDocument1 pageBBL Cheque Book Authorization Letterkazi shahriar mannan Maruf100% (1)

- Plagiarism Declaration Form (T-DF)Document8 pagesPlagiarism Declaration Form (T-DF)Nur HidayahNo ratings yet

- Composition of Cash and Cash EquivalentDocument20 pagesComposition of Cash and Cash EquivalentYenelyn Apistar CambarijanNo ratings yet

- 21-Spring 2019 - FA - SA - Sp-19Document8 pages21-Spring 2019 - FA - SA - Sp-19Muhammad KashifNo ratings yet

- Minimal Conditions For The Survival of The Euro - PRINTEDDocument57 pagesMinimal Conditions For The Survival of The Euro - PRINTEDAdrianaNo ratings yet

- Fabozzi Ch15 BMAS 7thedDocument42 pagesFabozzi Ch15 BMAS 7thedAbby PalomoNo ratings yet

- Credit Risk ManagementDocument17 pagesCredit Risk Managementarefayne wodajoNo ratings yet

- BSc2 Principles of Banking and Finance 2021-22Document8 pagesBSc2 Principles of Banking and Finance 2021-22loNo ratings yet

- Unit 7 Equity Financing (HH)Document35 pagesUnit 7 Equity Financing (HH)Nikhila SanapalaNo ratings yet

- Unit-Ii: Foreign Exchange Regulations and FormalitiesDocument27 pagesUnit-Ii: Foreign Exchange Regulations and FormalitiesLAKSHMIKANTH.B MEC-AP/MCNo ratings yet

- W13 Jurnal Forward Dan SwapDocument14 pagesW13 Jurnal Forward Dan Swapalberth sitorusNo ratings yet

- PRESENTATION On Merchant BankingDocument12 pagesPRESENTATION On Merchant Bankingsarthak1826No ratings yet

- Revise Tatq4Document19 pagesRevise Tatq4Tuyết TuyếtNo ratings yet

- AA153501 1427378053 BookDocument193 pagesAA153501 1427378053 BooklentinieNo ratings yet

- Vertical Balance Sheet Particulars RsDocument2 pagesVertical Balance Sheet Particulars Rsamit2201No ratings yet

- FTX (Uk) JDocument4 pagesFTX (Uk) JpavishneNo ratings yet

- Asahi Case SolutionDocument1 pageAsahi Case SolutionAmit BiswalNo ratings yet

- CH 1Document17 pagesCH 1Jin CaiNo ratings yet

- p2 Atlas Questionnaire - Income TaxationDocument9 pagesp2 Atlas Questionnaire - Income TaxationThe CollectorNo ratings yet

- 144084533r33 PDFDocument10 pages144084533r33 PDFRAJ TUWARNo ratings yet

- Daftar Isi Manajemen StrategikDocument3 pagesDaftar Isi Manajemen StrategikbudiNo ratings yet

- Sample Computation: 10% Bank FinDocument1 pageSample Computation: 10% Bank FinjonNo ratings yet

- Accounting Quick Update - IFRS 16 - Leases and IFRS 15 - RevenueDocument50 pagesAccounting Quick Update - IFRS 16 - Leases and IFRS 15 - RevenueTAWANDA CHIZARIRANo ratings yet

- T24 Induction Business - AccountDocument73 pagesT24 Induction Business - AccountprathaNo ratings yet

- Maa Durga Industries: C-1 Chandpole Anaj MandiDocument1 pageMaa Durga Industries: C-1 Chandpole Anaj Mandiragavaga453No ratings yet

- Dillon Read & The Aristocracy of Stock Profits - Catherine Austin FittsDocument231 pagesDillon Read & The Aristocracy of Stock Profits - Catherine Austin Fittsfourcade100% (2)

- Final Pyramid of Ratios: Strictly ConfidentialDocument3 pagesFinal Pyramid of Ratios: Strictly ConfidentialaeqlehczeNo ratings yet

- Bank On Yourself Special ReportDocument25 pagesBank On Yourself Special Reportblcksource100% (1)