You might also like

- Summary of The Only Game in Town: by Mohamed A. El Erian | Includes AnalysisFrom EverandSummary of The Only Game in Town: by Mohamed A. El Erian | Includes AnalysisNo ratings yet

- Assignment 4 What Is MoneyDocument6 pagesAssignment 4 What Is MoneyMuhammad HarisNo ratings yet

- CHINA-SDR - jrfm-12-00060-v2Document15 pagesCHINA-SDR - jrfm-12-00060-v2GANESHNo ratings yet

- China and The SDR-JRFM-Final-ProofDocument15 pagesChina and The SDR-JRFM-Final-ProofMik SerranoNo ratings yet

- Banking Crises Are Usually Followed by Low Credit and GDP GrowthDocument4 pagesBanking Crises Are Usually Followed by Low Credit and GDP GrowthKiran MahaNo ratings yet

- Macro 7Document12 pagesMacro 7Àlex SolàNo ratings yet

- Economist-Insights 1 JulyDocument2 pagesEconomist-Insights 1 JulybuyanalystlondonNo ratings yet

- Economics ProjectDocument20 pagesEconomics ProjectSiddhesh DalviNo ratings yet

- ZebrawhiteDocument12 pagesZebrawhitechrisNo ratings yet

- Multinational Financial Management 10th Edition Shapiro Solutions ManualDocument24 pagesMultinational Financial Management 10th Edition Shapiro Solutions ManualRobertCookynwk100% (26)

- b23194 Assignment 4 Divyansh KhareDocument4 pagesb23194 Assignment 4 Divyansh KhareDivyansh Khare B23194No ratings yet

- The Loans That Were - Sec BDocument12 pagesThe Loans That Were - Sec BhihiNo ratings yet

- Marking The 11th Hour - Corona Associates Capital Management - Year End Investment Letter - December 24th 2015Document13 pagesMarking The 11th Hour - Corona Associates Capital Management - Year End Investment Letter - December 24th 2015Julian ScurciNo ratings yet

- US FinPolicy 2019Document6 pagesUS FinPolicy 2019Ankur ShardaNo ratings yet

- Beijing's Lessons for Central BanksDocument3 pagesBeijing's Lessons for Central Banks3bandhuNo ratings yet

- "This Is Our Currency, But Your Problem" Foreign Debt Accumulation and Its ImplicationsDocument12 pages"This Is Our Currency, But Your Problem" Foreign Debt Accumulation and Its ImplicationsJohnPapaspanosNo ratings yet

- BRICs Exchange Rate RegimesDocument4 pagesBRICs Exchange Rate RegimesDipti KamdarNo ratings yet

- The Immoderate World Economy: Maurice ObstfeldDocument23 pagesThe Immoderate World Economy: Maurice ObstfeldDmitry PreobrazhenskyNo ratings yet

- Apapaper 4Document9 pagesApapaper 4api-356947179No ratings yet

- Manmohan Singh and Sonia Gandhi Are The CIA Agents of UsaDocument13 pagesManmohan Singh and Sonia Gandhi Are The CIA Agents of UsaSogno100% (3)

- Impossible Trinity ThesisDocument8 pagesImpossible Trinity Thesisgogelegepev2100% (1)

- 3-20-12 Fed Liquidity: Good As GoldDocument4 pages3-20-12 Fed Liquidity: Good As GoldThe Gold SpeculatorNo ratings yet

- Prof. Lalith Samarakoon As US Interest Rates Rise, No Space For Sri Lanka To Wait and SeeDocument8 pagesProf. Lalith Samarakoon As US Interest Rates Rise, No Space For Sri Lanka To Wait and SeeThavam RatnaNo ratings yet

- Managing financial risks in an era of global capital mobilityDocument22 pagesManaging financial risks in an era of global capital mobilitySunil SunitaNo ratings yet

- Side DishesDocument3 pagesSide Dishesnosheen90No ratings yet

- Ending Financial Repression in China, Cato Economic Development Bulletin No. 5Document4 pagesEnding Financial Repression in China, Cato Economic Development Bulletin No. 5Cato InstituteNo ratings yet

- BP 103Document12 pagesBP 103Mona AldarabieNo ratings yet

- Atharva: The Finance Magazine of IIM RaipurDocument32 pagesAtharva: The Finance Magazine of IIM RaipurFinatixIIMRaipurNo ratings yet

- IMF's Role in The Asian Financial Crisis: by Walden BelloDocument3 pagesIMF's Role in The Asian Financial Crisis: by Walden BelloPravin BirjeNo ratings yet

- AmericanProspect 1998 TheIMFandtheAsianFlu March-April1998Document8 pagesAmericanProspect 1998 TheIMFandtheAsianFlu March-April1998Abdurrohim NurNo ratings yet

- Japan Asia AugustDocument27 pagesJapan Asia AugustIronHarborNo ratings yet

- Evolution of Banking FinalDocument7 pagesEvolution of Banking FinalDouglasNo ratings yet

- Discussion Around The Article Linked BelowDocument12 pagesDiscussion Around The Article Linked BelowAllan WortNo ratings yet

- Faces of Death: The US Dollar in CrisisDocument12 pagesFaces of Death: The US Dollar in CrisisRon HeraNo ratings yet

- Trial of Strength: Will Today's Currency Interventions Hurt or Help The World Economy?Document3 pagesTrial of Strength: Will Today's Currency Interventions Hurt or Help The World Economy?Anja MihajlovaNo ratings yet

- Investment Insights - 30-03-2008 - Quantitative Easing and Buying Toxic DebtDocument3 pagesInvestment Insights - 30-03-2008 - Quantitative Easing and Buying Toxic DebtDemocracia real YANo ratings yet

- TPL The Latest PunchLine PresentationDocument20 pagesTPL The Latest PunchLine Presentationabe8840No ratings yet

- Lucky Yona Paper FinalDocument20 pagesLucky Yona Paper FinalluckyyonajrNo ratings yet

- Vietnam National University final assignment analyzes 2008 US financial crisisDocument17 pagesVietnam National University final assignment analyzes 2008 US financial crisisTrang TrầnNo ratings yet

- The Structure and Functions of The Federal Reserve System: Policy, Banking Supervision, Financial ServicesDocument18 pagesThe Structure and Functions of The Federal Reserve System: Policy, Banking Supervision, Financial ServicesJapish MehtaNo ratings yet

- Dwnload Full Foundations of Multinational Financial Management 6th Edition Shapiro Solutions Manual PDFDocument35 pagesDwnload Full Foundations of Multinational Financial Management 6th Edition Shapiro Solutions Manual PDFbologna.galleon7qhnrf100% (11)

- Full Download Foundations of Multinational Financial Management 6th Edition Shapiro Solutions ManualDocument35 pagesFull Download Foundations of Multinational Financial Management 6th Edition Shapiro Solutions Manualkyackvicary.n62kje100% (27)

- Chasing The DragonDocument2 pagesChasing The Dragonkeithxiaoxiao096No ratings yet

- US Interest Rate HikeDocument10 pagesUS Interest Rate HikeThavam RatnaNo ratings yet

- The Hutch Report - Volume 1 - Insights Top 50 Wealth Management InstitutionsDocument34 pagesThe Hutch Report - Volume 1 - Insights Top 50 Wealth Management InstitutionsldhutchNo ratings yet

- Brief History of Federal ReserveDocument11 pagesBrief History of Federal ReserveDuyen TranNo ratings yet

- Summary of The Only Game in Town: by Mohamed A. El Erian | Includes AnalysisFrom EverandSummary of The Only Game in Town: by Mohamed A. El Erian | Includes AnalysisNo ratings yet

- Price Insensitive Sellers and Ten Quick Topics To Ruin Your SummerDocument24 pagesPrice Insensitive Sellers and Ten Quick Topics To Ruin Your SummerCanadianValue0% (1)

- Creating New Money Padova Dez 2011Document14 pagesCreating New Money Padova Dez 2011MonetaProprietaNo ratings yet

- MONEY AND BANKING (School Work)Document9 pagesMONEY AND BANKING (School Work)Lan Mr-aNo ratings yet

- Acknowledgments and Case Study IntroductionDocument17 pagesAcknowledgments and Case Study Introductions_alimazharNo ratings yet

- Fixing The CrisisDocument8 pagesFixing The Crisisckarsharma1989No ratings yet

- Institutii de Credit Articol 10Document10 pagesInstitutii de Credit Articol 10Liliana DNo ratings yet

- Volume 2.4 Still Bullish Apr 13 2010Document12 pagesVolume 2.4 Still Bullish Apr 13 2010Denis OuelletNo ratings yet

- Final Days of The Dollar 11 22 10Document13 pagesFinal Days of The Dollar 11 22 10exDemocratNo ratings yet

- Market Insight - The Unbearable Lightness of Money 12-14-12-1Document2 pagesMarket Insight - The Unbearable Lightness of Money 12-14-12-1pgrat10No ratings yet

- Unconventional Policies and Their Effects On Financial Markets PDFDocument36 pagesUnconventional Policies and Their Effects On Financial Markets PDFSoberLookNo ratings yet

- The New Depression: The Breakdown of the Paper Money EconomyFrom EverandThe New Depression: The Breakdown of the Paper Money EconomyRating: 4 out of 5 stars4/5 (5)

- LAC Semiannual Report April 2014: International Flows to Latin America †“ Rocking the Boat?From EverandLAC Semiannual Report April 2014: International Flows to Latin America †“ Rocking the Boat?No ratings yet

- HSBC vs. National SteelDocument21 pagesHSBC vs. National SteelDexter CircaNo ratings yet

- Equipment Ledger CardDocument5 pagesEquipment Ledger CardDana A Daspit ConteNo ratings yet

- Customers Perception For Taking Life Insurance: A Critical Analysis of Life Insurance Sector in Virudhunagar District Mrs.S.Jeyalakshmi & Dr.V.KanagavelDocument7 pagesCustomers Perception For Taking Life Insurance: A Critical Analysis of Life Insurance Sector in Virudhunagar District Mrs.S.Jeyalakshmi & Dr.V.KanagavelPARTH PATELNo ratings yet

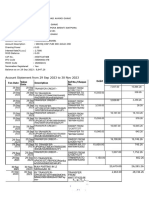

- Central Bank Statement From 22-Apr-2023 To 22-Jul-2023.Document20 pagesCentral Bank Statement From 22-Apr-2023 To 22-Jul-2023.Shafi MuhimtuleNo ratings yet

- Emerging Trends in Financial ServicesDocument2 pagesEmerging Trends in Financial ServicesAlok Ranjan100% (1)

- Unit-1 Introduction To Indian Banking SystemDocument40 pagesUnit-1 Introduction To Indian Banking SystemKruti BhattNo ratings yet

- Review Questions - Doc - EthicsDocument35 pagesReview Questions - Doc - EthicsExam Dost100% (1)

- Mother 4 343 Dongaon (1933) 23rd Aug 2013Document172 pagesMother 4 343 Dongaon (1933) 23rd Aug 2013माझ्या मनातलेNo ratings yet

- Financial Awareness Capsule July 2016 PDF 2Document19 pagesFinancial Awareness Capsule July 2016 PDF 2vamsiprasannakoduruNo ratings yet

- EPG REST Integration v.1.3.1Document37 pagesEPG REST Integration v.1.3.1Sain S - iRoid0% (1)

- FB Marketplace New FormatDocument7 pagesFB Marketplace New Formatwisdomdurojaiye80% (5)

- Orden de Venta - 372 - 20181123 - 123904Document2 pagesOrden de Venta - 372 - 20181123 - 123904l2oNnYNo ratings yet

- Terms and ConditionsDocument4 pagesTerms and Conditionsvikalpsharma96No ratings yet

- HCL It City Lucknow Private LimitedDocument10 pagesHCL It City Lucknow Private Limitedmathur1995No ratings yet

- 7e Ch5 Mini Case AnalyticsDocument6 pages7e Ch5 Mini Case AnalyticsDaniela667100% (9)

- Account Details and Transaction History SummaryDocument11 pagesAccount Details and Transaction History Summaryizzat emirNo ratings yet

- 397 SCRA 651 - Producers Bank of The Philippines Vs Hon. Court of AppealsDocument3 pages397 SCRA 651 - Producers Bank of The Philippines Vs Hon. Court of AppealsRengie GaloNo ratings yet

- #11Document2 pages#11Annabelle Bustamante100% (1)

- Letter of AuthorizationDocument1 pageLetter of AuthorizationGabriel de VeraNo ratings yet

- Christopher P. Mittleman's LetterDocument5 pagesChristopher P. Mittleman's LetterDealBook100% (2)

- Accounting Treatment of Goodwill at The Time of AdmissionDocument25 pagesAccounting Treatment of Goodwill at The Time of AdmissionMayurRawool100% (2)

- Solutions - LiabilitiesDocument10 pagesSolutions - LiabilitiesjhobsNo ratings yet

- Raoul S.V. Bonnevie and Honesto v. Bonnevie vs. The Honorable Court of AppealsDocument2 pagesRaoul S.V. Bonnevie and Honesto v. Bonnevie vs. The Honorable Court of AppealsVin LacsieNo ratings yet

- AgostoDocument6 pagesAgostodakpi479No ratings yet

- Barrel Race Entry FormDocument2 pagesBarrel Race Entry Formapi-245044768No ratings yet

- Universal Banking HDFCDocument16 pagesUniversal Banking HDFCrajesh bathulaNo ratings yet

- Bank Statement2023 12 02 15 56 04 7980Document5 pagesBank Statement2023 12 02 15 56 04 7980kazeemshaikNo ratings yet

- 1990 2014 Merc Law Bar Exam Q and ADocument260 pages1990 2014 Merc Law Bar Exam Q and ADahlia Claudine May Perral0% (1)

- A Simple Explanation of How Money Moves Around The Banking System - Richard Gendal BrownDocument12 pagesA Simple Explanation of How Money Moves Around The Banking System - Richard Gendal BrownAlijaNuhićNo ratings yet

- When Does A Letter of Comfort Becomes A Contract of GuaranteeDocument11 pagesWhen Does A Letter of Comfort Becomes A Contract of GuaranteeJ Imam100% (3)