You might also like

- Economic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Document3 pagesEconomic Highlights - Inflation Unexpectedly Eased in September - 25/10/2010Rhb InvestNo ratings yet

- Mandarin Version: Market Technical Reading - Short-Term Outlook Remains Positive... - 25/10/2010Document6 pagesMandarin Version: Market Technical Reading - Short-Term Outlook Remains Positive... - 25/10/2010Rhb InvestNo ratings yet

- LBS Bina Group Berhad: Removing The Recent High Will Spell More Rallies Ahead - 25/10/2010Document2 pagesLBS Bina Group Berhad: Removing The Recent High Will Spell More Rallies Ahead - 25/10/2010Rhb InvestNo ratings yet

- Wah Seong Corp Berhad: Gladstone and Curtis LNG Projects Contract Get Environmental Green Light - 25/10/2010Document2 pagesWah Seong Corp Berhad: Gladstone and Curtis LNG Projects Contract Get Environmental Green Light - 25/10/2010Rhb InvestNo ratings yet

- QL Resources Berhad: Expansions To Start Contributing From FY12 Onwards - 25/10/2010Document5 pagesQL Resources Berhad: Expansions To Start Contributing From FY12 Onwards - 25/10/2010Rhb InvestNo ratings yet

- Economic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Document2 pagesEconomic Highlights - Foreign Exchange Reserves Rose To US$104.6bn As at 15 October - 25/10/2010Rhb InvestNo ratings yet

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Document4 pagesRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestNo ratings yet

- Commodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Document3 pagesCommodities & Currencies - Yet Another Sign of A Rebound On The Greenback - 25/10/2010Rhb InvestNo ratings yet

- RHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Document4 pagesRHB Equity 360° - 25 October 2010 (QL, Wah Seong, Hunza Technical: TSH, LBS)Rhb InvestNo ratings yet

- Corporate Highlights - 25/10/2010Document2 pagesCorporate Highlights - 25/10/2010Rhb InvestNo ratings yet

- Market Technical Reading - Fresh Opportunity To Retest 1,500... - 22/10/2010Document6 pagesMarket Technical Reading - Fresh Opportunity To Retest 1,500... - 22/10/2010Rhb InvestNo ratings yet

- Hunza Properties Berhad: Headline Net Profit Skewed by EIs - 25/10/2010Document3 pagesHunza Properties Berhad: Headline Net Profit Skewed by EIs - 25/10/2010Rhb InvestNo ratings yet

- Fajarbaru Builder Group Berhad: Lands RM36.5m Pasir Mas Halal Park Infrastructure Job - 22/10/2010Document3 pagesFajarbaru Builder Group Berhad: Lands RM36.5m Pasir Mas Halal Park Infrastructure Job - 22/10/2010Rhb InvestNo ratings yet

- Telecommunications Sector Update: Sizing Up The Pure Mobile Domestic Players - Maxis vs. DiGi - 22/10/2010Document13 pagesTelecommunications Sector Update: Sizing Up The Pure Mobile Domestic Players - Maxis vs. DiGi - 22/10/2010Rhb InvestNo ratings yet

- Malaysia Airports Holdings Berhad: Sabiha-Gokcen For Long-Term Prospects - 22/10/2010Document7 pagesMalaysia Airports Holdings Berhad: Sabiha-Gokcen For Long-Term Prospects - 22/10/2010Rhb InvestNo ratings yet

- WCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Document3 pagesWCT Berhad: Secures RM1.36bn Building Job in Qatar and RM128m Hospital Project in Sabah - 21/10/2010Rhb InvestNo ratings yet

- Corporate Highlights - 21/10/2010Document2 pagesCorporate Highlights - 21/10/2010Rhb InvestNo ratings yet

- RHB Equity 360° - 22 October 2010 (Telecom, MAHB, Fajarbaru Technical: B-Corp)Document4 pagesRHB Equity 360° - 22 October 2010 (Telecom, MAHB, Fajarbaru Technical: B-Corp)Rhb InvestNo ratings yet

- Market Technical Reading - Recapturing The 10-Day SMA Will Renew Upbeat Sentiment... - 21/10/2010Document6 pagesMarket Technical Reading - Recapturing The 10-Day SMA Will Renew Upbeat Sentiment... - 21/10/2010Rhb InvestNo ratings yet

- Rubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Document2 pagesRubber Glove Sector Update: Still Cautious On Near-Term Outlook - 21/10/2010Rhb InvestNo ratings yet

- Corporate Highlights - 22/10/2010Document2 pagesCorporate Highlights - 22/10/2010Rhb InvestNo ratings yet

- Axis REIT: Quattro West Started To Contribute - 21/10/2010Document3 pagesAxis REIT: Quattro West Started To Contribute - 21/10/2010Rhb InvestNo ratings yet

- Puncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Document2 pagesPuncak Niaga Berhad: Eyeing Hogenakkal Water Project in India - 21/10/2010Rhb InvestNo ratings yet

- British American Tobacco: Corporate HighlightsDocument4 pagesBritish American Tobacco: Corporate HighlightsRhb InvestNo ratings yet

- Economic Highlights - Business Conditions Weakened But Consumer Sentiment Improved in The 3Q - 20/10/2010Document2 pagesEconomic Highlights - Business Conditions Weakened But Consumer Sentiment Improved in The 3Q - 20/10/2010Rhb InvestNo ratings yet

- Media Sector Update - 9M10 Print and TV Adex Up by 18.2% - 21/10/2010Document6 pagesMedia Sector Update - 9M10 Print and TV Adex Up by 18.2% - 21/10/2010Rhb InvestNo ratings yet

- RHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Document4 pagesRHB Equity 360° - 21 October 2010 (Media, Rubber Gloves, Puncak Niaga, WCT, Axis REIT, BAT Technical: AFG)Rhb InvestNo ratings yet

- Economic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Document2 pagesEconomic Highlights - Leading Index Bounced Back in August, Pointing To A Resilient Economic Activities Ahead - 20/10/2010Rhb InvestNo ratings yet

- Economic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Document3 pagesEconomic Highlights - Decline in Manufacturing Investment Approvals Narrowed in The 2Q - 20/10/2010Rhb InvestNo ratings yet

- Market Technical Reading - Tracking The Regional Volatile Sentiment... - 20/10/2010Document6 pagesMarket Technical Reading - Tracking The Regional Volatile Sentiment... - 20/10/2010Rhb InvestNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- COVID-19 and Its Impact On The Indian EconomyDocument17 pagesCOVID-19 and Its Impact On The Indian Economyuday xeroxNo ratings yet

- History of Competition LawDocument17 pagesHistory of Competition LawshubhamNo ratings yet

- CASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Document1 pageCASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Ataur RahmanNo ratings yet

- Harold O. Fried, Shelton S. Schmidt, C. A. Knox Lovell-The Measurement of Productive Efficiency - Techniques and Applications (1993)Document439 pagesHarold O. Fried, Shelton S. Schmidt, C. A. Knox Lovell-The Measurement of Productive Efficiency - Techniques and Applications (1993)pedrosoares__No ratings yet

- Challenges For Omnichannel StoreDocument5 pagesChallenges For Omnichannel StoreAnjali SrivastvaNo ratings yet

- Governance Letter To CompaniesDocument3 pagesGovernance Letter To CompaniesTBP_Think_TankNo ratings yet

- Poultry Farm Business PlanDocument4 pagesPoultry Farm Business PlanAbdul Basit Bazaz100% (1)

- Appointment Letter-New DraftDocument3 pagesAppointment Letter-New DraftNikita JaiswalNo ratings yet

- Nominal vs Effective Interest Rates & Equivalence CalculationsDocument28 pagesNominal vs Effective Interest Rates & Equivalence CalculationsLyle Dominic AtienzaNo ratings yet

- Japan Since 1980Document330 pagesJapan Since 1980JianBre100% (3)

- Ducati, Case Analysis: Nitin Dangwal 13P094 Section BDocument4 pagesDucati, Case Analysis: Nitin Dangwal 13P094 Section BJames Kudrow100% (2)

- Draft MP Net Metering Policy - 4.11Document11 pagesDraft MP Net Metering Policy - 4.11Anand PuntambekarNo ratings yet

- Intercompany Inventory TransactionsDocument4 pagesIntercompany Inventory Transactionszsaw zsawNo ratings yet

- Pom AssignmentDocument13 pagesPom AssignmentParth SharmaNo ratings yet

- Mobile App Business PlanDocument12 pagesMobile App Business PlanMuhammad Hidayah0% (1)

- AUG 10 Danske EMEADailyDocument3 pagesAUG 10 Danske EMEADailyMiir ViirNo ratings yet

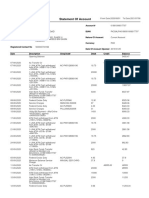

- 'Account StatementDocument11 pages'Account StatementSikander Qazi100% (2)

- Solution Manual For Mcgraw Hills Taxation of Individuals and Business Entities 2020 Edition 11th by SpilkerDocument37 pagesSolution Manual For Mcgraw Hills Taxation of Individuals and Business Entities 2020 Edition 11th by Spilkeractinozoalionizem7k7100% (21)

- IFC and Partners Invest $1.1 Billion To Build The Largest Solar Plant and Wind Farm in EgyptDocument4 pagesIFC and Partners Invest $1.1 Billion To Build The Largest Solar Plant and Wind Farm in EgyptviNo ratings yet

- Accounting Information System at Sonali Bank LimitedDocument24 pagesAccounting Information System at Sonali Bank LimitedsaidulNo ratings yet

- Unit - III Labour CostDocument38 pagesUnit - III Labour CosttheriyathuNo ratings yet

- Sustainability 13 02422 v3Document22 pagesSustainability 13 02422 v3Pierre MillotNo ratings yet

- Vidhey Patel ResumeDocument2 pagesVidhey Patel ResumeadelaideglxNo ratings yet

- Regional Integration in Africa by Victor AdetulaDocument32 pagesRegional Integration in Africa by Victor AdetulaJeremy JordanNo ratings yet

- HR Project ReportDocument5 pagesHR Project ReportSolo BgmNo ratings yet

- Internship Program.: ProposalDocument5 pagesInternship Program.: ProposalstrangerNo ratings yet

- Solutions Manual: 1st EditionDocument23 pagesSolutions Manual: 1st EditionJunior Waqairasari67% (3)

- 1.4 Classification of ProductDocument11 pages1.4 Classification of Productbabunaidu2006No ratings yet

- SG 2Document43 pagesSG 2SWETCHCHA MISKANo ratings yet

- SE ContractDocument21 pagesSE Contractaugusta.mironNo ratings yet