You might also like

- Page 1 of 3 36833 SAP Note Jan 25, 2021 9: DescriptionDocument3 pagesPage 1 of 3 36833 SAP Note Jan 25, 2021 9: Descriptiondgr77No ratings yet

- For Office Only: Co CoDocument1 pageFor Office Only: Co CoPrabath Nilan GunasekaraNo ratings yet

- Output Ratings: Diesel Generator Set Exclusively From Your Cat ® DealerDocument7 pagesOutput Ratings: Diesel Generator Set Exclusively From Your Cat ® Dealerعلوي الهاشميNo ratings yet

- Materi Uas - Final - Suham C Aks18Document45 pagesMateri Uas - Final - Suham C Aks18suhamcahyonoNo ratings yet

- Chain DrivesDocument20 pagesChain Drivesharshdeep2638No ratings yet

- Content FormatDocument1 pageContent FormatSanjay SathiasekharanNo ratings yet

- UnnamedDocument1 pageUnnamederic1388No ratings yet

- Test Unit 9 HW 31 O5 23Document2 pagesTest Unit 9 HW 31 O5 23Nikita PoroshinNo ratings yet

- CID 0100 FMI 03 Engine Oil Pressure Open/short To +batt: TroubleshootingDocument1 pageCID 0100 FMI 03 Engine Oil Pressure Open/short To +batt: TroubleshootingRobel KebedeNo ratings yet

- LAG ConfigurationDocument6 pagesLAG ConfigurationArmand PicheleNo ratings yet

- PDF Pioneer b2 Tests CompressDocument65 pagesPDF Pioneer b2 Tests Compressalejandra.cuasquerNo ratings yet

- Esutbusinessjournal 14Document19 pagesEsutbusinessjournal 14Lê Viết Bi BoNo ratings yet

- Vengthlang North YMADocument2 pagesVengthlang North YMAsangteack1067No ratings yet

- PTW - Level 1 Training New Proposal SimonDocument39 pagesPTW - Level 1 Training New Proposal SimonKORAMA KIEN100% (1)

- Low Engine Oil Pressure: Shutdown SIS Previous ScreenDocument2 pagesLow Engine Oil Pressure: Shutdown SIS Previous ScreenRobel KebedeNo ratings yet

- Accounting ratios analysisDocument9 pagesAccounting ratios analysisAmbily SaliNo ratings yet

- Net DesignDocument26 pagesNet DesignMohammad HegazyNo ratings yet

- TESCO Financial AnalysisDocument21 pagesTESCO Financial AnalysisIdrees Sheikh100% (1)

- Engine Oil Cooler Bypass 3500Document3 pagesEngine Oil Cooler Bypass 3500Anonymous V9fdC6No ratings yet

- Rope Drive DesignDocument24 pagesRope Drive Designharshdeep2638No ratings yet

- 100KVA Trafo SpecDocument15 pages100KVA Trafo SpecAnfal BarbhuiyaNo ratings yet

- Section-2 Hvac System Design For Clean Facility: Co CoDocument1 pageSection-2 Hvac System Design For Clean Facility: Co CopremNo ratings yet

- Word Formation 02 02 23Document1 pageWord Formation 02 02 23NykytaNo ratings yet

- RPT QRCodesDocument2 pagesRPT QRCodesAsset BPKDNo ratings yet

- Grafik Penerimaan Obat Terbanyak Tahun 2019Document5 pagesGrafik Penerimaan Obat Terbanyak Tahun 2019ghaida salsabilaNo ratings yet

- This Is A Sample Empty Letter Template.: Ar ArDocument1 pageThis Is A Sample Empty Letter Template.: Ar Arpatagonia3No ratings yet

- Questions AnsweredDocument30 pagesQuestions AnsweredLancasterFirstNo ratings yet

- Effects of Consumerism - Global IssuesDocument17 pagesEffects of Consumerism - Global IssuesJose PepeNo ratings yet

- BitLocker Drive Encryption Recovery KeyDocument1 pageBitLocker Drive Encryption Recovery KeyAnonymous SNEL2bNo ratings yet

- Progress Report: Ghana Institute of MGNT and Public AdminDocument2 pagesProgress Report: Ghana Institute of MGNT and Public AdminGeorge GhanemNo ratings yet

- Simple overunity method may produce more energy than inputDocument2 pagesSimple overunity method may produce more energy than inputamanNo ratings yet

- FOS On Materials Strength Factors in HKDocument1 pageFOS On Materials Strength Factors in HKStephen KungNo ratings yet

- Sliding Contact BearingsDocument49 pagesSliding Contact Bearingsharshdeep2638No ratings yet

- Plate CalcsDocument1 pagePlate CalcsKrish AãrkãyNo ratings yet

- 10 Hydraulic System Oil Level - CheckDocument6 pages10 Hydraulic System Oil Level - Checkmuftah76No ratings yet

- Helical GearDocument21 pagesHelical Gearharshdeep2638No ratings yet

- Ar Ar: Er-Softw Er-SoftwDocument1 pageAr Ar: Er-Softw Er-SoftwCikgu BerbagiNo ratings yet

- Engine Oil PressureDocument7 pagesEngine Oil PressureRobel KebedeNo ratings yet

- Vampire Savior 2 - Moves - StrategyWiki, The Free Strategy Guide and Walkthrough WikiDocument14 pagesVampire Savior 2 - Moves - StrategyWiki, The Free Strategy Guide and Walkthrough WikiMac Will Fengyep NgassamNo ratings yet

- 01c.cloning Towards APZ17.0 AGM318Document17 pages01c.cloning Towards APZ17.0 AGM318Loi Huynh TanNo ratings yet

- 1.modele I Elemente Ale Structurii XMLDocument13 pages1.modele I Elemente Ale Structurii XMLMaria SevciucNo ratings yet

- Incidence Map 10182021Document1 pageIncidence Map 10182021Debbie HarbsmeierNo ratings yet

- Presentation On Operational AuditDocument29 pagesPresentation On Operational AuditRNo ratings yet

- Reading 17 10 23buhDocument1 pageReading 17 10 23buhОлімпіада На УрокNo ratings yet

- The History and Future of The WTODocument36 pagesThe History and Future of The WTOHamad KalafNo ratings yet

- Incidence Map 08162021Document1 pageIncidence Map 08162021Debbie HarbsmeierNo ratings yet

- Pusat Pendidikan Dan Pelatihan Industri Sekolah Menengah Kejuruan - Smak Bogor Laboratorium Tempat Uji Kompetensi (Tuk) SmakboDocument1 pagePusat Pendidikan Dan Pelatihan Industri Sekolah Menengah Kejuruan - Smak Bogor Laboratorium Tempat Uji Kompetensi (Tuk) SmakboRahmah WulanNo ratings yet

- October 2019 Math PaperDocument34 pagesOctober 2019 Math Papervanessa.livaniaNo ratings yet

- Zarah Notes Insurance LawDocument32 pagesZarah Notes Insurance LawTinn ApNo ratings yet

- Population of Towns As of July 2021Document50 pagesPopulation of Towns As of July 2021Real BrightNo ratings yet

- Highway & Traffic Eng Classification Highway LocationDocument16 pagesHighway & Traffic Eng Classification Highway Locationhiran peirisNo ratings yet

- CV for Structural EngineerDocument2 pagesCV for Structural EngineerPardonné KiamessoNo ratings yet

- CFA 2 RegistrationDocument1 pageCFA 2 Registrationtien8618No ratings yet

- Indian Railways Classifies Broad Gauge Lines by SpeedDocument5 pagesIndian Railways Classifies Broad Gauge Lines by SpeedBrijesh SinghNo ratings yet

- Piping and Instrumentation Diagram for Gas Plant - I (Unit No: 30Document9 pagesPiping and Instrumentation Diagram for Gas Plant - I (Unit No: 30Wă ÎłNo ratings yet

- Incidence Map 07082021Document1 pageIncidence Map 07082021Debbie HarbsmeierNo ratings yet

- CalibrationDocument6 pagesCalibrationRobel Kebede100% (1)

- Helical SpringDocument34 pagesHelical Springharshdeep2638No ratings yet

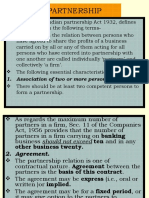

- Partnership: 1. Association of Two or More PersonsDocument4 pagesPartnership: 1. Association of Two or More PersonsshekharmvmNo ratings yet

- Delivery." Which A Right Is Created in Favour of Some Person."Document5 pagesDelivery." Which A Right Is Created in Favour of Some Person."shekharmvmNo ratings yet

- Doctrine of Caveat EmptorDocument3 pagesDoctrine of Caveat Emptorshekharmvm80% (5)

- Dissolution of Partnership FirmDocument5 pagesDissolution of Partnership Firmshekharmvm100% (2)

- Incoming and Outgoing PartnersDocument4 pagesIncoming and Outgoing PartnersshekharmvmNo ratings yet

- Bill of ExchangeDocument2 pagesBill of ExchangeshekharmvmNo ratings yet

- DirectorsDocument17 pagesDirectorsshekharmvmNo ratings yet

- Conditions and WarrantiesDocument13 pagesConditions and WarrantiesshekharmvmNo ratings yet

- BailmentDocument8 pagesBailmentshekharmvmNo ratings yet

- Principles of Macroeconomics 6th Edition Frank Test Bank 1Document36 pagesPrinciples of Macroeconomics 6th Edition Frank Test Bank 1cynthiasheltondegsypokmj100% (24)

- IC SWOT and PEST Analysis 11598 - WORDDocument2 pagesIC SWOT and PEST Analysis 11598 - WORDGianna Glov100% (1)

- Questions COSTDocument5 pagesQuestions COSTDonita BinayNo ratings yet

- Caso Toy World IncDocument18 pagesCaso Toy World IncLuis Fernando MoraNo ratings yet

- BofA Merrill - QuestionsDocument2 pagesBofA Merrill - QuestionsShubham KumarNo ratings yet

- 52608500Document68 pages52608500Anjo Vasquez100% (1)

- 05.12.2023 PB Cause ListDocument14 pages05.12.2023 PB Cause ListSREEMANTINI MUKHERJEENo ratings yet

- Profitability Analysis of Nepal Electricity Authority - RashiDocument9 pagesProfitability Analysis of Nepal Electricity Authority - RashiRashi GoyalNo ratings yet

- Psychology of Trading: Controlling Emotions is KeyDocument4 pagesPsychology of Trading: Controlling Emotions is KeyjoseluisvazquezNo ratings yet

- Fintech PresentationDocument6 pagesFintech PresentationStudent Placement CoordinatorNo ratings yet

- Advanced Financial Management Test 1 May 2024 Solution 1701932012Document15 pagesAdvanced Financial Management Test 1 May 2024 Solution 1701932012shauryagupta20013007No ratings yet

- Understanding Market EquilibriumDocument22 pagesUnderstanding Market EquilibriumTw YulianiNo ratings yet

- Corrección Del Quiz de Vocabulario: Economy and BusinessDocument2 pagesCorrección Del Quiz de Vocabulario: Economy and BusinessAngelica Duarte BecerraNo ratings yet

- "Trial Balance ": by Srinivas Methuku Asst. Professor, SLS HyderabadDocument17 pages"Trial Balance ": by Srinivas Methuku Asst. Professor, SLS HyderabadMuthu KonarNo ratings yet

- MRF Tyres Brand Expansion StrategyDocument87 pagesMRF Tyres Brand Expansion StrategyMohit BansalNo ratings yet

- Corporation: Title XVDocument9 pagesCorporation: Title XVDarrel SapinosoNo ratings yet

- JAIME Company budgeting questionsDocument2 pagesJAIME Company budgeting questionsLopez, Azzia M.No ratings yet

- Ilocos Kidney Plus Dialysis Center Supply and Medicine Flow ChartDocument1 pageIlocos Kidney Plus Dialysis Center Supply and Medicine Flow ChartWyn AgustinNo ratings yet

- Mylan Write-Up Historicals and Sell RecommendationDocument1 pageMylan Write-Up Historicals and Sell RecommendationAdam SchlossNo ratings yet

- MA4850 Supply Chain & Logistics ManagementDocument25 pagesMA4850 Supply Chain & Logistics ManagementQy LeeNo ratings yet

- Fy 2018 FinancialsDocument68 pagesFy 2018 FinancialsAnonymous UH3nIimNo ratings yet

- International Trade Assignment 2Document22 pagesInternational Trade Assignment 2Gayatri PanjwaniNo ratings yet

- Solutions Brief Accounting ExercisesDocument4 pagesSolutions Brief Accounting ExercisesHa Dang Huynh NhuNo ratings yet

- Frsa Theory Notes Unit IDocument7 pagesFrsa Theory Notes Unit ISuganesh NetflixNo ratings yet

- Letter of Guarantee For Permanent Vat DefermentDocument1 pageLetter of Guarantee For Permanent Vat DefermentSheruni Amanthi Therese AllesNo ratings yet

- HEL Case Study on Supply Chain ManagementDocument27 pagesHEL Case Study on Supply Chain ManagementMayank KothariNo ratings yet

- Full Download Essentials of Life Span Development 2nd Edition Santrock Test BankDocument35 pagesFull Download Essentials of Life Span Development 2nd Edition Santrock Test Banksultryjuliformykka100% (23)

- Hotel NewsDocument88 pagesHotel NewsnickiminajNo ratings yet

- Automatic extension letter of creditDocument1 pageAutomatic extension letter of creditЛаниер Ср Брајант ХенриNo ratings yet

- BAJAJ HEALTHCARE LTD. - PurveeshaDocument44 pagesBAJAJ HEALTHCARE LTD. - PurveeshaShree KhandelwalNo ratings yet