You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Introduction To Sustainability - Lecture 6Document18 pagesIntroduction To Sustainability - Lecture 6Wasana MuthumaliNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Exercise 5.1: A Werribee Office Cleaners: Cash Receipts JournalDocument9 pagesExercise 5.1: A Werribee Office Cleaners: Cash Receipts JournalDoan Chan PhongNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- BHR 407, BPM 424, Bse424 Notes 2023Document63 pagesBHR 407, BPM 424, Bse424 Notes 2023Eric KiverengeNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Kenya Warehousing Market Outlook To 2023Document13 pagesKenya Warehousing Market Outlook To 2023Janno van der LaanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Kindler Volume XV July-December 2015 Conference SpecialDocument453 pagesKindler Volume XV July-December 2015 Conference SpecialArmy Institute of Management, KolkataNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- CPA Review School of The Philippines: Obligations DO Dela CruzDocument23 pagesCPA Review School of The Philippines: Obligations DO Dela CruzLegara RobelynNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Chapter 3 - Introduction To Optimization Modeling: Answer: CDocument6 pagesChapter 3 - Introduction To Optimization Modeling: Answer: CRashaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Chapter 06 - Cost-Volume-Profit RelationshipsDocument15 pagesChapter 06 - Cost-Volume-Profit RelationshipsHardly Dare GonzalesNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Sales and Marketing Information SystemDocument13 pagesSales and Marketing Information SystemAnindita Nandy75% (4)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Renewables Atlas FinalDocument128 pagesRenewables Atlas FinalOrtegaYONo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- ARIIX Compensation Plan Bible (Hong Kong & China) - 中国和香港奖励汁划资料册Document5 pagesARIIX Compensation Plan Bible (Hong Kong & China) - 中国和香港奖励汁划资料册ARIIX GlobalNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Enterprise Risk Management FrameworkDocument2 pagesEnterprise Risk Management FrameworkalkalkiaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Anti-Money Laundering ManualDocument15 pagesAnti-Money Laundering ManualMarilyn OhoylanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Assignment 6 RORDocument7 pagesAssignment 6 RORKHANSA DIVA NUR APRILIANo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Week 2 Overview of Tourism and Hospitality Industry 3Document28 pagesWeek 2 Overview of Tourism and Hospitality Industry 3kimberly dueroNo ratings yet

- SAP WMS User Requirements Gathering Questionnaire 3Document3 pagesSAP WMS User Requirements Gathering Questionnaire 3Anil Kumar100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 7077 - Cash and Accruals BasisDocument2 pages7077 - Cash and Accruals BasisKlare JimenoNo ratings yet

- AccorDocument11 pagesAccorPooja Kumari Deo50% (2)

- Car Brand Automobile Industry in The Porte's MatrixDocument5 pagesCar Brand Automobile Industry in The Porte's MatrixAli IsmailNo ratings yet

- Chapter 3: Internet Consumers and Market ResearchDocument69 pagesChapter 3: Internet Consumers and Market ResearchKamran Shabbir0% (1)

- Privatization and Nationalization TopicDocument9 pagesPrivatization and Nationalization TopicNELSONNo ratings yet

- Module Handbook Tourism Marketing PrinciplesDocument13 pagesModule Handbook Tourism Marketing PrinciplesJay MenonNo ratings yet

- Pardot User Sync Implementation GuideDocument12 pagesPardot User Sync Implementation GuidenethriNo ratings yet

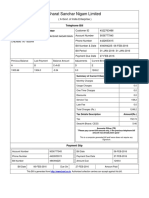

- BSNL Bill - Jan2016Document1 pageBSNL Bill - Jan2016ritbhaiNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Conviser Company: Joint Cost Product C Product L Product T TotalDocument6 pagesConviser Company: Joint Cost Product C Product L Product T TotalKiyo KoNo ratings yet

- Rural Media: Conventional Mass Media Non-Conventional Mass Media Personalized Mass MediaDocument10 pagesRural Media: Conventional Mass Media Non-Conventional Mass Media Personalized Mass Mediadnrt09No ratings yet

- North South University: Department of Management Management Information Systems MIS207 - SUMMER 2020 Midterm - 02Document5 pagesNorth South University: Department of Management Management Information Systems MIS207 - SUMMER 2020 Midterm - 02Zahid Hridoy100% (2)

- Essay - Cirebon-Semarang Transmission Pipeline - Faris HabiburrahmanDocument3 pagesEssay - Cirebon-Semarang Transmission Pipeline - Faris HabiburrahmanFaris HabiburrahmanNo ratings yet

- Corporate Governance Refers in General To The Rules, Procedures, or Laws WherebyDocument7 pagesCorporate Governance Refers in General To The Rules, Procedures, or Laws WherebyLigayaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Literature Review Organisational CultureDocument9 pagesLiterature Review Organisational Cultureafmacaewfefwug100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)