92% found this document useful (36 votes)

60K views31 pagesBanking Instruments

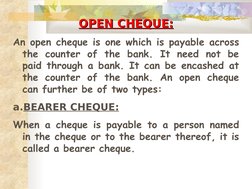

This document discusses various types of banking instruments including deposits, cheques, demand drafts, debit and credit notes, and vouchers. It provides details on what each instrument is, how it works, and how it differs from other similar instruments. For example, it explains that a cheque can be an open cheque or crossed cheque, and describes the difference between a demand draft and a regular cheque. The document also covers topics like deposits slips, types of cheque crossings including general and special crossings, and debit and credit notes.

Uploaded by

sunny_live09Copyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPT, PDF, TXT or read online on Scribd

92% found this document useful (36 votes)

60K views31 pagesBanking Instruments

This document discusses various types of banking instruments including deposits, cheques, demand drafts, debit and credit notes, and vouchers. It provides details on what each instrument is, how it works, and how it differs from other similar instruments. For example, it explains that a cheque can be an open cheque or crossed cheque, and describes the difference between a demand draft and a regular cheque. The document also covers topics like deposits slips, types of cheque crossings including general and special crossings, and debit and credit notes.

Uploaded by

sunny_live09Copyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPT, PDF, TXT or read online on Scribd

- Kinds of Banking Instruments

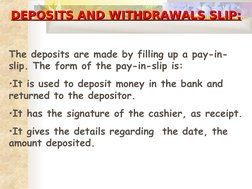

- Deposit or Pay-in-Slip

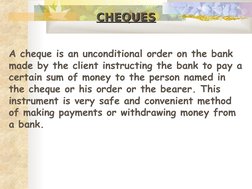

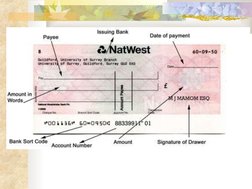

- Cheques

- Types of Cheques

- Crossed Cheque

- Demand Draft

- Debit Note & Credit Note

- Voucher

- Cheque Crossing