100% found this document useful (1 vote)

4K views23 pagesFinal Project of Accounting

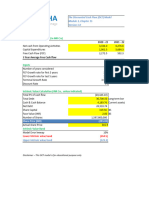

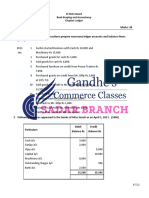

The document is a final project report submitted by a group of students for their Bachelor's degree in Business Administration. It analyzes and compares the financial statements of two shoe companies, Bata Shoes and Servis Shoes, over two years (2007-2008) using various financial ratios. The ratios calculated include liquidity, leverage, profitability, activity, and market ratios. Data is presented in tables and interpretations are provided for analysis of the financial health and performance of each company.

Uploaded by

pirzada Arslan sabriCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

100% found this document useful (1 vote)

4K views23 pagesFinal Project of Accounting

The document is a final project report submitted by a group of students for their Bachelor's degree in Business Administration. It analyzes and compares the financial statements of two shoe companies, Bata Shoes and Servis Shoes, over two years (2007-2008) using various financial ratios. The ratios calculated include liquidity, leverage, profitability, activity, and market ratios. Data is presented in tables and interpretations are provided for analysis of the financial health and performance of each company.

Uploaded by

pirzada Arslan sabriCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd