A325 discussion – March 19, 2012

Budgeting – planning

We use budgets as a target that we hope or expect to achieve. These are

financial and non-financial in nature, but typically offer some quantitative

measure

We will begin by talking about the building of a STATIC BUDGET. A static

budget is the basic PLAN that you are expecting. For a manufacturing firm,

you typically start with SALES and work your way back to PRODUCTION

and then to PURCHASING of raw materials.

Breakers, Inc. is preparing budgets for the quarter ending June 30.

Budgeted sales for the next five months are:

April 20,000 units

May 50,000 units

June 30,000 units

July 25,000 units

August 15,000 units.

The selling price is $10 per unit.

The management of Breakers, Inc. wants ending inventory to be equal to

20% of the following month’s budgeted sales in units.

On March 31, 4,000 units were on hand.

• At Breakers, five kilograms of material are required per unit of product.

• Management wants materials on hand at the end of each month equal to

10% of the following month’s production.

• On March 31, 13,000 kilograms of material are on hand. Material cost

$.40 per kilogram.

1

�A325 discussion – March 19, 2012

• At Breakers, each unit of product requires 0.1 hours of direct labor.

• The Company has a “no layoff” policy so all employees will be paid for 40

hours of work each week.

• In exchange for the “no layoff” policy, workers agreed to a wage rate of

$8 per hour regardless of the hours worked (No overtime pay).

• For the next three months, the direct-labor workforce will be paid for a

minimum of 3,000 hours per month.

• At Breakers, variable selling and administrative expenses are $0.50 per

unit sold.

• Fixed selling and administrative expenses are $70,000 per month.

• The $70,000 fixed expenses include $10,000 in depreciation expense

that does not require a cash outflow for the month.

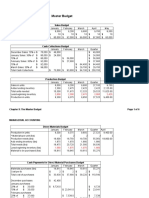

Overhead Budget (taken as given)

April May June Quarter

Indirect labor $ 25,700 $ 35,900 $ 26,100 $ 61,900

Indirect material 7,000 12,600 8,600 28,200

Utilities 4,200 8,400 5,200 17,800

Rent 13,300 13,300 13,300 39,900

Insurance 5,800 5,800 5,800 17,400

Depreciation 8,200 9,400 8,200 25,800

$ 64,200 $ 85,400 $ 67,200 $ 191,000

2

�A325 discussion – March 19, 2012

At Breakers, all sales are on account.

The company’s collection pattern is:

• 70% collected in the month of sale,

• 25% collected in the month following sale,

• 5% is uncollected.

The March 31 accounts receivable balance of $30,000 will be collected in

full.

• Breakers pays $0.40 per kilogram for its materials.

• One-half of a month’s purchases are paid for in the month of purchase;

the other half is paid in the following month.

• No discounts are available.

• The March 31 accounts payable balance is $12,000.

• Maintains a 12% open line of credit for $75,000.

• Maintains a minimum cash balance of $30,000.

• Borrows on the first day of the month and repays loans on the last day of

the month.

• Pays a cash dividend of $25,000 in April.

• Purchases $143,700 of equipment in May and $48,300 in June paid in

cash.

• Has an April 1 cash balance of $40,000.

3

�A325 discussion – March 19, 2012

Here is the solution to that problem.

First, we prepare a REVENUE BUDGET (or SALES BUDGET)

Sales

April May June Quarter

Sales 20,000 50,000 30,000 100,000

Price 10.00 10.00 10.00 10.00

Revenue 200,000 500,000 300,000 1,000,000

We must also know our Sales for July and August, since June’s ending

inventories will depend on July production and July’s production will depend

on August Sales.

July August

Sales 25,000 15,000

Price 10.00 10.00

Revenue 250,000 150,000

Next, we prepare a production budget using the fact that we have 4,000

units on hand as of March 31 and the fact that we require 20% of the next

month’s sales on hand in Ending FGI (20% of 20,000 units of April sales is

4,000 units – our March 31 ending inventory):

4

�A325 discussion – March 19, 2012

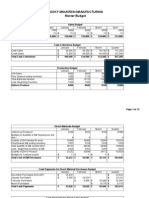

Production

April May June Quarter July August

Sales 20,000 50,000 30,000 100,000 25,000 15,000

Less Beginning Inventory 4,000 10,000 6,000 4,000 5,000

16,000 40,000 24,000 96,000 20,000

Add Ending Inventory 10,000 6,000 5,000 5,000 3,000

Produced 26,000 46,000 29,000 101,000 23,000

Now, we use the production budget to compute our purchases of Raw

Materials. We have 13,000 Kg of materials on hand and require 10% of the

following month’s production on hand in ending inventory. Each unit produced

requires 5 Kg of materials. Materials cost $.40 per Kg. The beginning

inventory of 13,000 Kg is: 26,000 units produced in April X 5 Kg = 130,000

(our total needs for April production) X 10%.

Direct Materials

April May June Quarter July August

Produced 26,000 46,000 29,000 101,000 23,000 15,000

Materials required 130,000 230,000 145,000 505,000 115,000

Less Beginning Inventory 13,000 23,000 14,500 13,000 -

117,000 207,000 130,500 492,000 23,000

Add Ending Inventory 23,000 14,500 11,500 11,500 -

Units purchased 140,000 221,500 142,000 503,500 23,000

Price per pound 0.40 0.40 0.40 0.40

Purchases (cost) 56,000 88,600 56,800 201,400

Next, we budget for Direct Labor. An hour of direct labor costs $8. Direct

Labor is a minimum of 3,000 hours and is otherwise based upon .1 hour per

unit produced. We work off of the production budget above.

5

�A325 discussion – March 19, 2012

Direct Labor

April May June Quarter

Produced 26,000 46,000 29,000 101,000

Labor required 2,600 4,600 2,900

Minimum labor 3,000 3,000 3,000

3,000 4,600 3,000 10,600

Price per hour 8.00 8.00 8.00 8.00

Direct Labor Cost 24,000 36,800 24,000 84,800

The overhead budget was given:

Overhead

April May June Quarter

Indirect labor 25,700 35,900 26,100 87,700

Indirect material 7,000 12,600 8,600 28,200

Utilities 4,200 8,400 5,200 17,800

Rent 13,300 13,300 13,300 39,900

Insurance 5,800 5,800 5,800 17,400

Depreciation 8,200 9,400 8,200 25,800

64,200 85,400 67,200 216,800

That completes the components of production (Direct Materials, Direct

Labor, and Overhead). Now we will base our selling and administrative

expense budget on sales for the period. It is pretty straight-forward.

6

�A325 discussion – March 19, 2012

Selling and Administrative

April May June Quarter

Sales 20,000 50,000 30,000 100,000

Variable S and A rate 0.50 0.50 0.50 0.50

Variable Selling and Admin 10,000 25,000 15,000 50,000

Fixed S and A 60,000 60,000 60,000 180,000

Total Selling and Admin 70,000 85,000 75,000 230,000

Now, we start putting together our CASH BUDGET. First, based upon the

sales budget, our beginning Accounts Receivable of $30,000, and our

collection expectations, we budget for Cash Receipts.

Cash Receipts

April May June Quarter

Sales 20,000 50,000 30,000 100,000

Price 10.00 10.00 10.00 10.00

Revenue 200,000 500,000 300,000 1,000,000

Collections from previous month 30,000 50,000 125,000 205,000

Collections from this month 140,000 350,000 210,000 700,000

Total Collections 170,000 400,000 335,000 905,000

Our cash disbursements (outflows of cash) are based upon payments for

direct materials, payments for direct labor, and our CASH payments for

overhead, as well as our payments for selling and administrative expenses

and any DIVIDENDS or CASH PURCHASES that we may make in a period.

7

�A325 discussion – March 19, 2012

Our cash payments for materials purchases is given below:

Cash Disbursements - Materials

April May June Quarter

Purchases (cost) 56,000 88,600 56,800 201,400

Paid from this month 28,000 44,300 28,400

Paid from last month 12,000 28,000 44,300

Total materials payments 40,000 72,300 72,700 185,000

This gives us the following CASH BUDGET

Cash Budget

April May June Quarter

Beginning Balance 40,000 30,000 30,000 40,000

Cash from Revenues 170,000 400,000 335,000 905,000

Cash Available 210,000 430,000 365,000 945,000

Cash Disbursements

Purchases 40,000 72,300 72,700 185,000

Labor 24,000 36,800 24,000 84,800

Overhead 56,000 76,000 59,000 191,000

Selling and Admin 70,000 85,000 75,000 230,000

Equipment Purchase 143,700 48,300 192,000

Dividends 25,000 - - 25,000

Total 215,000 413,800 279,000 907,800

Excess Cash (5,000) 16,200 86,000 37,200

Borrowing 35,000 13,800 48,800

Repayment (48,800) (48,800)

Interest - - (1,326) (1,326)

Ending Balance 30,000 30,000 35,874 35,874