0% found this document useful (0 votes)

353 views19 pagesSFA Solved Question Bank As Per July 2022

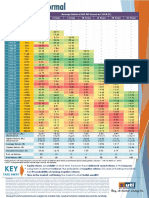

The document is a sample question paper for a valuation examination that covers various topics related to securities valuation, financial assets, accounting, taxation, and insolvency. It contains 37 multiple choice questions testing knowledge of concepts like national income measurement, fiscal and primary deficits, quantitative easing, net present value, debt to equity ratios, cash flow statements, valuation methods, and regulations governing securities, taxation, and insolvency.

Uploaded by

Abhijat MittalCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

353 views19 pagesSFA Solved Question Bank As Per July 2022

The document is a sample question paper for a valuation examination that covers various topics related to securities valuation, financial assets, accounting, taxation, and insolvency. It contains 37 multiple choice questions testing knowledge of concepts like national income measurement, fiscal and primary deficits, quantitative easing, net present value, debt to equity ratios, cash flow statements, valuation methods, and regulations governing securities, taxation, and insolvency.

Uploaded by

Abhijat MittalCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd