0% found this document useful (0 votes)

30 views8 pagesModule No 12 - Regular Allowable Itemized Deductions

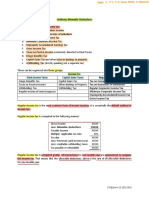

Module No. 12 covers the conditions, rules, and computational procedures for regular allowable itemized deductions from gross income, including interest expense, taxes, losses, bad debts, depreciation, depletion, charitable contributions, and pension contributions. It outlines the requisites for deductibility, examples of deductible and non-deductible items, and provides illustrations for clarity. The module emphasizes the importance of adhering to legal stipulations and proper documentation for each type of deduction.

Uploaded by

castillorussel363Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

30 views8 pagesModule No 12 - Regular Allowable Itemized Deductions

Module No. 12 covers the conditions, rules, and computational procedures for regular allowable itemized deductions from gross income, including interest expense, taxes, losses, bad debts, depreciation, depletion, charitable contributions, and pension contributions. It outlines the requisites for deductibility, examples of deductible and non-deductible items, and provides illustrations for clarity. The module emphasizes the importance of adhering to legal stipulations and proper documentation for each type of deduction.

Uploaded by

castillorussel363Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd