0% found this document useful (0 votes)

63 views16 pagesTopic 3 Chargeable Income

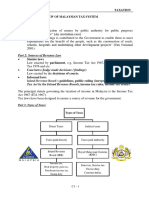

The document outlines the computation of chargeable income for individuals and companies in Malaysia, detailing the steps from ascertaining the source of income to arriving at the chargeable income. It explains the components of gross income, adjusted income, statutory income, and aggregate income, along with examples and tax treatments for business losses and donations. Additionally, it covers personal tax relief and tax rates applicable to individual taxpayers and companies.

Uploaded by

AdamCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

63 views16 pagesTopic 3 Chargeable Income

The document outlines the computation of chargeable income for individuals and companies in Malaysia, detailing the steps from ascertaining the source of income to arriving at the chargeable income. It explains the components of gross income, adjusted income, statutory income, and aggregate income, along with examples and tax treatments for business losses and donations. Additionally, it covers personal tax relief and tax rates applicable to individual taxpayers and companies.

Uploaded by

AdamCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd