0% found this document useful (0 votes)

1K views3 pagesBasic Accounting Journal Entries

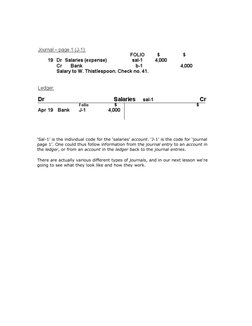

The journal is the initial record of business transactions and is used to record debits and credits in chronological order. Each transaction includes a brief explanation and reference number to link it to supporting documents. Reference numbers also connect journal entries to specific accounts in the ledger to allow tracing transactions through the accounting cycle. Various types of journals exist to record different types of transactions.

Uploaded by

Dominicque HartCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOC, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

1K views3 pagesBasic Accounting Journal Entries

The journal is the initial record of business transactions and is used to record debits and credits in chronological order. Each transaction includes a brief explanation and reference number to link it to supporting documents. Reference numbers also connect journal entries to specific accounts in the ledger to allow tracing transactions through the accounting cycle. Various types of journals exist to record different types of transactions.

Uploaded by

Dominicque HartCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOC, PDF, TXT or read online on Scribd

- Basic Accounting Journal Entries: Introduces journal entries, explaining their relevance and displaying format examples for accounting students.