0% found this document useful (0 votes)

1K views33 pagesIndia's Multimodal Logistics Future

The document discusses multimodal logistics hubs and their future potential in India. It begins by providing context on the significance of logistics and the transition from unimodal to multimodal transport. It then discusses the history and global perspective of multimodal logistics before focusing on the Indian perspective. Key points about the Indian logistics sector include its growth rate but also inefficiencies compared to other countries. The document outlines various global trends supporting the growth of multimodal logistics hubs and discusses developments in India's transport infrastructure like the dedicated freight corridor and growth of multimodal logistics parks.

Uploaded by

singhranjanCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

1K views33 pagesIndia's Multimodal Logistics Future

The document discusses multimodal logistics hubs and their future potential in India. It begins by providing context on the significance of logistics and the transition from unimodal to multimodal transport. It then discusses the history and global perspective of multimodal logistics before focusing on the Indian perspective. Key points about the Indian logistics sector include its growth rate but also inefficiencies compared to other countries. The document outlines various global trends supporting the growth of multimodal logistics hubs and discusses developments in India's transport infrastructure like the dedicated freight corridor and growth of multimodal logistics parks.

Uploaded by

singhranjanCopyright

© Attribution Non-Commercial (BY-NC)

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

- Agenda

- Era of Globalization

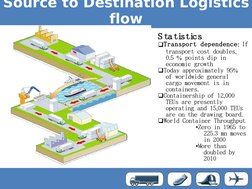

- Source to Destination Logistics Flow

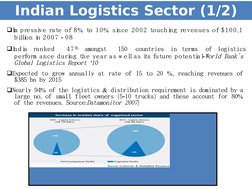

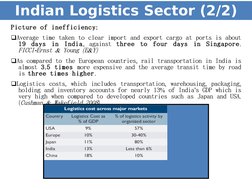

- Indian Logistics Sector

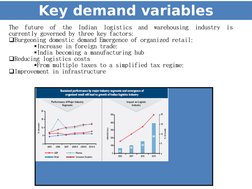

- Key Demand Variables

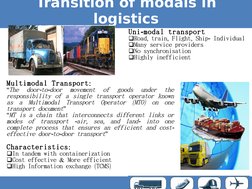

- Transition of Modals in Logistics

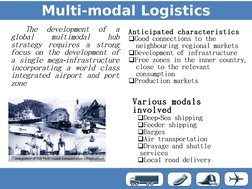

- Multi-modal Logistics

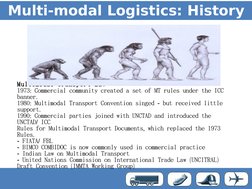

- Multi-modal Logistics: History

- Global Perspective

- Global Trends Favoring Growth

- Opportunities & Competition

- Multi-modal Logistics: Update

- Comparison of Different Modes of Transport

- Key Developments - India's Transport Infrastructure

- Dedicated Freight Corridor

- Multi-modal Logistics Hubs/Parks (MMLP)

- Elaborating on Major Entities

- Containerization

- Revenue Sources of MMH

- Value Added Services

- Development Stages of MMH

- Government Policies

- VAPI - MultiModal Logistics Hub

- Roadblocks to Growth

- Way Ahead