0% found this document useful (0 votes)

13 views17 pagesFinancial System and Internal Control Overview

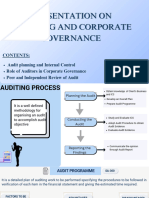

The document outlines the objectives and procedures of various financial systems including purchasing, sales invoicing, payroll, credit control, and cash management, emphasizing the importance of internal controls to prevent fraud and errors. It discusses the roles of internal and external auditors, the limitations of internal controls, and the responsibilities of management and the board of directors in maintaining effective systems. Additionally, it highlights the advantages and disadvantages of external audits, including their impact on management disputes and operational disruptions.

Uploaded by

bjj44567Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

13 views17 pagesFinancial System and Internal Control Overview

The document outlines the objectives and procedures of various financial systems including purchasing, sales invoicing, payroll, credit control, and cash management, emphasizing the importance of internal controls to prevent fraud and errors. It discusses the roles of internal and external auditors, the limitations of internal controls, and the responsibilities of management and the board of directors in maintaining effective systems. Additionally, it highlights the advantages and disadvantages of external audits, including their impact on management disputes and operational disruptions.

Uploaded by

bjj44567Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd