You might also like

- Equity Valuation Report - LVMHDocument3 pagesEquity Valuation Report - LVMHFEPFinanceClubNo ratings yet

- Cfroi HoltDocument7 pagesCfroi Holtamro_baryNo ratings yet

- Mercury Athletic Historical Income StatementsDocument18 pagesMercury Athletic Historical Income StatementskarthikawarrierNo ratings yet

- Homework #3 TemplateDocument18 pagesHomework #3 TemplateAnthony ButlerNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- NYSF Practice TemplateDocument22 pagesNYSF Practice TemplaterapsjadeNo ratings yet

- SBICAPS - Model Test 2Document34 pagesSBICAPS - Model Test 2rishav digga0% (1)

- McDonald's (MCD) - Earnings Quality ReportDocument1 pageMcDonald's (MCD) - Earnings Quality ReportInstant AnalystNo ratings yet

- IFS - Simple Three Statement ModelDocument1 pageIFS - Simple Three Statement ModelThanh NguyenNo ratings yet

- Ch02 P14 Build A Model AnswerDocument4 pagesCh02 P14 Build A Model Answersiefbadawy1No ratings yet

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Document178 pagesIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- Degree Polynomial:: Generic Yield Interpolation ChartDocument9 pagesDegree Polynomial:: Generic Yield Interpolation Chartapi-3763138No ratings yet

- Bond Duration - Dynamic ChartDocument3 pagesBond Duration - Dynamic Chartapi-3763138No ratings yet

- Bond Valuation ProblemsDocument4 pagesBond Valuation ProblemsMary Justine Paquibot100% (1)

- This Study Resource Was: Answer of Bond ValuationDocument9 pagesThis Study Resource Was: Answer of Bond Valuationmuhammad hasan100% (2)

- Relative Value Models (Feb04)Document18 pagesRelative Value Models (Feb04)api-3763138No ratings yet

- RV YTM Model PDFDocument47 pagesRV YTM Model PDFAllen LiNo ratings yet

- Lbo DCF ModelDocument38 pagesLbo DCF ModelBobbyNicholsNo ratings yet

- Case 1 SwanDavisDocument4 pagesCase 1 SwanDavissilly_rabbit0% (1)

- 06 06 Football Field Walmart Model Valuation BeforeDocument47 pages06 06 Football Field Walmart Model Valuation BeforeIndrama Purba0% (1)

- ProjectDocument24 pagesProjectAayat R. AL KhlafNo ratings yet

- DCF ModellDocument7 pagesDCF ModellziuziNo ratings yet

- 72Ho-Singer Model V3Document28 pages72Ho-Singer Model V3aqwaNo ratings yet

- Merger Model PP Allocation BeforeDocument100 pagesMerger Model PP Allocation BeforePaulo NascimentoNo ratings yet

- Valuation Cash Flow A Teaching NoteDocument5 pagesValuation Cash Flow A Teaching NotesarahmohanNo ratings yet

- Blank Financial ModelDocument109 pagesBlank Financial Modelrising_aboveNo ratings yet

- Qatar National Bank April 2011Document6 pagesQatar National Bank April 2011Michael KiddNo ratings yet

- Valuation - CocacolaDocument14 pagesValuation - CocacolaLegends MomentsNo ratings yet

- FM TemplateDocument3 pagesFM TemplateWynn WizzNo ratings yet

- 1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678Document18 pages1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678X.r. GeNo ratings yet

- Valuation of A FirmDocument13 pagesValuation of A FirmAshish RanjanNo ratings yet

- CAT ValuationDocument231 pagesCAT ValuationMichael CheungNo ratings yet

- FCFE CalculationDocument23 pagesFCFE CalculationIqbal YusufNo ratings yet

- WACC AnalysisDocument9 pagesWACC AnalysisFadhilNo ratings yet

- How To Calculate Terminal ValueDocument4 pagesHow To Calculate Terminal ValueSODDEYNo ratings yet

- Quantamental Research - ITC LTDDocument1 pageQuantamental Research - ITC LTDsadaf hashmiNo ratings yet

- 1 2 3 4 5 6 7 8 9 File Name: C:/Courses/Course Materials/3 Templates and Exercises M&A Models/LBO Shell - Xls Colour CodesDocument46 pages1 2 3 4 5 6 7 8 9 File Name: C:/Courses/Course Materials/3 Templates and Exercises M&A Models/LBO Shell - Xls Colour CodesfdallacasaNo ratings yet

- Fitch C Do RatingDocument29 pagesFitch C Do RatingMakarand LonkarNo ratings yet

- Eclerx Services (Eclser) : Chugging Along..Document6 pagesEclerx Services (Eclser) : Chugging Along..shahavNo ratings yet

- LBO Completed ModelDocument210 pagesLBO Completed ModelBrian DongNo ratings yet

- Worldwide Paper DCFDocument16 pagesWorldwide Paper DCFLaila SchaferNo ratings yet

- 20.06.26 Nano II Model - SentDocument309 pages20.06.26 Nano II Model - SentAdrian KurniaNo ratings yet

- CRS Monte Carlo Simulation WorkpapersDocument388 pagesCRS Monte Carlo Simulation WorkpapersShaunak ChitnisNo ratings yet

- q2 Valuation Insights Second 2020 PDFDocument20 pagesq2 Valuation Insights Second 2020 PDFKojiro FuumaNo ratings yet

- Variance Analysis: Assignment Line ItemDocument18 pagesVariance Analysis: Assignment Line Itemfatima khurramNo ratings yet

- European World-Class Results Are Close To Overall Results, But Fewer Top Performers On CostDocument35 pagesEuropean World-Class Results Are Close To Overall Results, But Fewer Top Performers On Costkapnau007No ratings yet

- Hynix Semiconductor: Initiate With A 1-OW: Re-Armed and ReadyDocument45 pagesHynix Semiconductor: Initiate With A 1-OW: Re-Armed and Readymanastir_2000No ratings yet

- Toys R Us LBO Model BlankDocument34 pagesToys R Us LBO Model BlankCatarina AlmeidaNo ratings yet

- Task 3 - Model Answer EmailDocument1 pageTask 3 - Model Answer EmailPruthvi Shetty ShettyNo ratings yet

- L&T 4Q Fy 2013Document15 pagesL&T 4Q Fy 2013Angel BrokingNo ratings yet

- Indonesia Loss Reserving (Example)Document6 pagesIndonesia Loss Reserving (Example)Setyo Tyas JarwantoNo ratings yet

- APV Method FrameworkDocument17 pagesAPV Method FrameworkssinhNo ratings yet

- One Page M&A Simple Model Improved BlankDocument21 pagesOne Page M&A Simple Model Improved BlankAllen FengNo ratings yet

- Fitch Special Report US Private Equity Overview October 2010Document19 pagesFitch Special Report US Private Equity Overview October 2010izi25No ratings yet

- DCF ModelDocument6 pagesDCF ModelKatherine ChouNo ratings yet

- Free Cash Flow To Firm DCF Valuation Model Base DataDocument3 pagesFree Cash Flow To Firm DCF Valuation Model Base DataTran Anh VanNo ratings yet

- 1) Template Detailed ModelDocument20 pages1) Template Detailed Modelabdul5721No ratings yet

- Cole Park CLO LimitedDocument22 pagesCole Park CLO Limitedeimg20041333No ratings yet

- ABC Company, Inc. Recapitalization AnalysisDocument10 pagesABC Company, Inc. Recapitalization AnalysisMarcNo ratings yet

- Analytical Calibration Using A Reversed Cubic Curve FitDocument12 pagesAnalytical Calibration Using A Reversed Cubic Curve FitNoah ZlinNo ratings yet

- Binomial Probability Distribution: Sample Size Probability of Success Mean Standard DeviationDocument2 pagesBinomial Probability Distribution: Sample Size Probability of Success Mean Standard DeviationShawnNo ratings yet

- READ ME: Spreadsheet Guide: Only WhiteDocument17 pagesREAD ME: Spreadsheet Guide: Only WhiteNicholas LutfiNo ratings yet

- Tarea 5 - Curva Caracteristica de OperaciónDocument4 pagesTarea 5 - Curva Caracteristica de OperaciónCarolina MontoyaNo ratings yet

- Confidence Interval Lower Limit Confidence Interval Upper LimitDocument165 pagesConfidence Interval Lower Limit Confidence Interval Upper LimitJoe BoustanyNo ratings yet

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Estimating Growth Rates (Teaching Model)Document4 pagesEstimating Growth Rates (Teaching Model)api-3763138No ratings yet

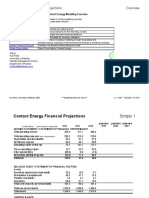

- Contact - Main 2006Document89 pagesContact - Main 2006api-3763138No ratings yet

- SchwartzMoon (2000) Rational Pricing Internet CpyDocument14 pagesSchwartzMoon (2000) Rational Pricing Internet Cpyapi-3763138No ratings yet

- Stiglitz Weiss 1981 Implementation by Kurt HessDocument20 pagesStiglitz Weiss 1981 Implementation by Kurt Hessapi-3763138No ratings yet

- Endowment - Warrant - Valuer (McVerry) DDocument244 pagesEndowment - Warrant - Valuer (McVerry) Dapi-3763138No ratings yet

- Δr=α b−r Δt+σε Δt: Simulation of short-term interest ratesDocument19 pagesΔr=α b−r Δt+σε Δt: Simulation of short-term interest ratesapi-3763138No ratings yet

- Refresh Worksheet ListDocument14 pagesRefresh Worksheet Listapi-3763138No ratings yet

- Spline Basis Function Approximating Discount Function Fitting Bond UniverseDocument5 pagesSpline Basis Function Approximating Discount Function Fitting Bond Universeapi-3763138No ratings yet

- Longstaff Schwartz (95) Risky Debt (P)Document18 pagesLongstaff Schwartz (95) Risky Debt (P)api-3763138No ratings yet

- Bond Price With Excel FunctionsDocument6 pagesBond Price With Excel Functionsapi-3763138No ratings yet

- Bond Pricing - System of Five Bond VariablesDocument2 pagesBond Pricing - System of Five Bond Variablesapi-3763138No ratings yet

- Converts PrimerDocument6 pagesConverts Primerjunjun07_01No ratings yet

- Bond Pricing - BasicsDocument2 pagesBond Pricing - Basicsapi-3763138No ratings yet

- Bond Duration - BasicsDocument2 pagesBond Duration - Basicsapi-3763138No ratings yet

- Bond Pricing - Dynamic ChartDocument4 pagesBond Pricing - Dynamic Chartapi-3763138No ratings yet

- Input All Yellow Shaded AreasDocument6 pagesInput All Yellow Shaded Areasapi-3763138No ratings yet

- Put - Call Parity Model: Synthetic SecuritiesDocument3 pagesPut - Call Parity Model: Synthetic Securitiesapi-3763138No ratings yet

- Bond Convexity - Dynamic ChartDocument3 pagesBond Convexity - Dynamic Chartapi-3763138No ratings yet

- Bond Duration - Price Sensitivity Using DurationDocument3 pagesBond Duration - Price Sensitivity Using Durationapi-3763138No ratings yet

- PvtdiscrateDocument4 pagesPvtdiscrateapi-3763138No ratings yet

- Inputs: Before Restructuring After RestructuringDocument4 pagesInputs: Before Restructuring After Restructuringapi-3763138No ratings yet

- OptltDocument3 pagesOptltapi-3763138No ratings yet

- Bond Convexity - BasicsDocument2 pagesBond Convexity - Basicsapi-3763138No ratings yet

- Bond and Stock ValutionsDocument23 pagesBond and Stock ValutionsNikhil TurkarNo ratings yet

- Bond ValuationDocument49 pagesBond Valuationmehnaz kNo ratings yet

- Bonds PayableDocument5 pagesBonds PayableJoseph AsisNo ratings yet

- CH 09Document45 pagesCH 09Monir AheenNo ratings yet

- Sinking Fund PresentationDocument12 pagesSinking Fund Presentationyoshan tharushaNo ratings yet

- Bond Valuation - Practice QuestionsDocument3 pagesBond Valuation - Practice QuestionsMuhammad Mansoor100% (3)

- Chapter 3 - Valuing BondsDocument37 pagesChapter 3 - Valuing BondsDeok NguyenNo ratings yet

- Midterm Fixed IncomeDocument6 pagesMidterm Fixed IncomeBasel ObaidNo ratings yet

- Convertable Bond: (Option Adjusted Spread)Document6 pagesConvertable Bond: (Option Adjusted Spread)Taychang WangNo ratings yet

- Convertible Bonds CH 24Document2 pagesConvertible Bonds CH 24Debarnob SarkarNo ratings yet

- Ch05 P24 Build A ModelDocument5 pagesCh05 P24 Build A ModelKatarína HúlekováNo ratings yet

- QF2104 Tutorial - Assignment 4Document3 pagesQF2104 Tutorial - Assignment 4igndunnoNo ratings yet

- FBL4Document15 pagesFBL4FaleeNo ratings yet

- Investing in Bonds WorksheetDocument6 pagesInvesting in Bonds Worksheetapi-311692437No ratings yet

- Seminar Set 5Document3 pagesSeminar Set 5fanuel kijojiNo ratings yet

- HihiDocument20 pagesHihiCath OquialdaNo ratings yet

- Session 2 EMBA Interest Rate RiskDocument24 pagesSession 2 EMBA Interest Rate Risksatu tanvirNo ratings yet

- Sinking Fund BondsDocument8 pagesSinking Fund BondsKunal MaheshwariNo ratings yet

- Bonds and Their Valuation (Comprehensive Spreadsheet Problem Answers)Document15 pagesBonds and Their Valuation (Comprehensive Spreadsheet Problem Answers)Kaira Go100% (1)

- BT Chap 6Document4 pagesBT Chap 6Hang NguyenNo ratings yet

- CH 06Document34 pagesCH 06Puput AjaNo ratings yet

- Debt C-EDocument1,236 pagesDebt C-EFirdaus AliNo ratings yet

- Values For U.S. Savings Bonds: $50 Series I/EE/E Bonds and $50 Savings NotesDocument17 pagesValues For U.S. Savings Bonds: $50 Series I/EE/E Bonds and $50 Savings NotesMichaelNo ratings yet

- Floating Rate Notes: Concepts and BuzzwordsDocument6 pagesFloating Rate Notes: Concepts and BuzzwordsMyagmarsuren SanaakhorolNo ratings yet

- Bonds and Their Valuaton - Practice QuestionsDocument3 pagesBonds and Their Valuaton - Practice Questionsluliga.loulouNo ratings yet

- FI AssignmentDocument7 pagesFI AssignmentsuggestionboxNo ratings yet

- FMDFINA Valuation Online HandoutsDocument12 pagesFMDFINA Valuation Online HandoutsasiacrisostomoNo ratings yet

- Financial Markets & Institutions Feb.23Document2 pagesFinancial Markets & Institutions Feb.23pratik9365No ratings yet