You might also like

- Superstore Sales InsightsDocument3 pagesSuperstore Sales InsightsSachin RathodNo ratings yet

- Cootamundra House PricesDocument4 pagesCootamundra House PricesDaisy HuntlyNo ratings yet

- 2020 Recap Global Manda by The NumbersDocument4 pages2020 Recap Global Manda by The NumbersIman Ridhwan SyahNo ratings yet

- Denge Kimya - First Quarter ReportDocument16 pagesDenge Kimya - First Quarter ReportAli SarwarNo ratings yet

- Listings Sold by Calendar QuarterDocument9 pagesListings Sold by Calendar Quarterapi-27643796No ratings yet

- Real EstateDocument8 pagesReal EstatenguyentrantoquynhtqNo ratings yet

- 2013 Tax Bracket CalculatorDocument1 page2013 Tax Bracket Calculatorsalauddin1979No ratings yet

- Cost Breakdown Oct. 09 PDFDocument1 pageCost Breakdown Oct. 09 PDFBreckenridge Grand Real EstateNo ratings yet

- Trimble Investor Overview-February 2023Document24 pagesTrimble Investor Overview-February 2023RA ThriftshopNo ratings yet

- 2 FunctionsDocument17 pages2 FunctionsSalman AhmadNo ratings yet

- Montgomery County Empower Montgomery ReportDocument7 pagesMontgomery County Empower Montgomery ReportAJ MetcalfNo ratings yet

- Staggers PropertyDocument8 pagesStaggers PropertyBen KellerNo ratings yet

- Fairclough PropertyDocument7 pagesFairclough PropertyBen KellerNo ratings yet

- Tax Year 2020 StatisticsDocument127 pagesTax Year 2020 StatisticsAdam HarringtonNo ratings yet

- Jermolowicz Sabrina Excel02 ExpendituresDocument6 pagesJermolowicz Sabrina Excel02 Expendituresapi-535055317No ratings yet

- Q1 2011 Quarterly EarningsDocument15 pagesQ1 2011 Quarterly EarningsRip Empson100% (1)

- Cma-27-1 Douro Place-West Perth-Wa 6005Document16 pagesCma-27-1 Douro Place-West Perth-Wa 6005sapphireNo ratings yet

- Ultimate Spreadsheet Charts: SynopsisDocument38 pagesUltimate Spreadsheet Charts: SynopsisRizki RidwanNo ratings yet

- Spartan Inc - German MotorsDocument4 pagesSpartan Inc - German MotorsFavian Maraville YadisaputraNo ratings yet

- Chapter 9 Case Question Finance SolvedDocument1 pageChapter 9 Case Question Finance SolvedOwais Khan KhattakNo ratings yet

- Dashboard Template 2 - Complete: Strictly ConfidentialDocument2 pagesDashboard Template 2 - Complete: Strictly ConfidentialKnightspageNo ratings yet

- Dashboard Template 2 CompleteDocument2 pagesDashboard Template 2 CompleteKshitize GuptaNo ratings yet

- Education Technology QuarterlyDocument14 pagesEducation Technology QuarterlyAmit GalaNo ratings yet

- Tugas Accounting IntermediateDocument1 pageTugas Accounting IntermediateYohanes PitherNo ratings yet

- NAR 2018 Proposed Budget SummaryDocument6 pagesNAR 2018 Proposed Budget SummaryRobert HahnNo ratings yet

- 3Q20 Earnings PresentationDocument15 pages3Q20 Earnings PresentationjazzNo ratings yet

- Chapter07 XlssolDocument49 pagesChapter07 XlssolEkhlas AmmariNo ratings yet

- Market Analysis by Area Oct. 09Document1 pageMarket Analysis by Area Oct. 09Breckenridge Grand Real EstateNo ratings yet

- Ultimate Spreadsheet Charts: SynopsisDocument38 pagesUltimate Spreadsheet Charts: SynopsisjpereztmpNo ratings yet

- GDP OverallDocument832 pagesGDP OverallEleanorXuNo ratings yet

- Google PresentationDocument22 pagesGoogle Presentationcia100% (10)

- Fahmi Gilang Madani - 120110170024 - Tugas AKLDocument6 pagesFahmi Gilang Madani - 120110170024 - Tugas AKLFahmi GilangNo ratings yet

- Iab Internet Advertising Revenue Report: PWC PWCDocument21 pagesIab Internet Advertising Revenue Report: PWC PWCebelaniNo ratings yet

- Indonesia Digitization EraDocument8 pagesIndonesia Digitization Eraasri suryaNo ratings yet

- January 2010 Summit County Real Estate StatsDocument7 pagesJanuary 2010 Summit County Real Estate StatsBreckenridge Grand Real EstateNo ratings yet

- ZULUAGA, 2020 - Cash Flow Cycle Analysis TemplateDocument8 pagesZULUAGA, 2020 - Cash Flow Cycle Analysis TemplateandreaNo ratings yet

- Capital Budgeting Techniques WorkshopDocument3 pagesCapital Budgeting Techniques WorkshopValentina Barreto Puerta0% (1)

- Resort Real Estate Index First Quarter 2010Document4 pagesResort Real Estate Index First Quarter 2010Breckenridge Grand Real EstateNo ratings yet

- Trial BalanceDocument9 pagesTrial BalanceJasmine ActaNo ratings yet

- SP Immigration Services Financial PlanDocument24 pagesSP Immigration Services Financial Planmalik_saleem_akbarNo ratings yet

- Agent 360: Public RecordsDocument3 pagesAgent 360: Public RecordsCarlos CruzNo ratings yet

- Q4 2010 Quarterly EarningsDocument15 pagesQ4 2010 Quarterly EarningsAlexia BonatsosNo ratings yet

- NP EX19 9b JinruiDong 2Document10 pagesNP EX19 9b JinruiDong 2Ike DongNo ratings yet

- 1Q MA Emerging Market Financial Advisory ReviewDocument16 pages1Q MA Emerging Market Financial Advisory ReviewRahul MahajanNo ratings yet

- TAP Molson Coors Ny Investor Deck Final 2018Document81 pagesTAP Molson Coors Ny Investor Deck Final 2018Ala BasterNo ratings yet

- PepperTea P&LDocument2 pagesPepperTea P&Lstock marketNo ratings yet

- Analisis MRB - 17 - 18 - 19 - 20Document4,260 pagesAnalisis MRB - 17 - 18 - 19 - 20Yulisa CastroNo ratings yet

- Dashboard Template: Business Unit Revenue ($000) Profit Margin ($000)Document1 pageDashboard Template: Business Unit Revenue ($000) Profit Margin ($000)GolamMostafaNo ratings yet

- F Wall Street 4-JNJ-Analysis (2009)Document1 pageF Wall Street 4-JNJ-Analysis (2009)smith_raNo ratings yet

- Guri-BABMGT517 - Operational Performance Report Template-Task 4Document2 pagesGuri-BABMGT517 - Operational Performance Report Template-Task 4Kumar Creative ContentsNo ratings yet

- The Office Furniture Store Data FileDocument16 pagesThe Office Furniture Store Data FileVy Nguyễn Trần TườngNo ratings yet

- Market Snapshot Full Years 08-09Document1 pageMarket Snapshot Full Years 08-09Breckenridge Grand Real EstateNo ratings yet

- Zoned To Shrink PresentationDocument33 pagesZoned To Shrink PresentationWVXU NewsNo ratings yet

- Wholesale Banking PresentationDocument22 pagesWholesale Banking PresentationAlezNgNo ratings yet

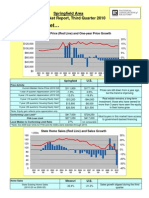

- Today's Market : Springfield Area Local Market Report, Third Quarter 2010Document7 pagesToday's Market : Springfield Area Local Market Report, Third Quarter 2010phatty34No ratings yet

- Blue Ridge Spain ExcelDocument5 pagesBlue Ridge Spain Excelsanchi virmaniNo ratings yet

- HRM Kpi-DashboardDocument10 pagesHRM Kpi-DashboardMahmud MorshedNo ratings yet

- Selling Canadian Books in Colombia: A Guide for Canadian PublishersFrom EverandSelling Canadian Books in Colombia: A Guide for Canadian PublishersNo ratings yet

- My First Gujarati Money, Finance & Shopping Picture Book with English Translations: Teach & Learn Basic Gujarati words for Children, #17From EverandMy First Gujarati Money, Finance & Shopping Picture Book with English Translations: Teach & Learn Basic Gujarati words for Children, #17Rating: 5 out of 5 stars5/5 (1)

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Edmonton Mayor Amarjeet Sohi letter to Alberta Premier Danielle Smith, April 2, 2024Document6 pagesEdmonton Mayor Amarjeet Sohi letter to Alberta Premier Danielle Smith, April 2, 2024edmontonjournalNo ratings yet

- Alberta Pension Plan - Analysis of Costs, Benefits, Risks and ConsiderationsDocument95 pagesAlberta Pension Plan - Analysis of Costs, Benefits, Risks and Considerationsedmontonjournal100% (3)

- Mandatory Reviews Into Child Deaths: October 2021 - March 2022Document100 pagesMandatory Reviews Into Child Deaths: October 2021 - March 2022edmontonjournalNo ratings yet

- Who Can Stay - GoDocument9 pagesWho Can Stay - GoedmontonjournalNo ratings yet

- Caucus LetterDocument2 pagesCaucus LetteredmontonjournalNo ratings yet

- 2022-02-11 Hangar 14 Investment Study - FINAL (Lo Res)Document188 pages2022-02-11 Hangar 14 Investment Study - FINAL (Lo Res)edmontonjournalNo ratings yet

- Premier Designate Danielle Smith Holds First Caucus MeetingDocument1 pagePremier Designate Danielle Smith Holds First Caucus MeetingedmontonjournalNo ratings yet

- Allegations Involving Premier Danielle Smith May 17 2023Document17 pagesAllegations Involving Premier Danielle Smith May 17 2023edmontonjournalNo ratings yet

- UCP AGM Plenary Agenda 2022Document36 pagesUCP AGM Plenary Agenda 2022edmontonjournalNo ratings yet

- Mandatory Reviews Into Child Deaths: October 2021 - March 2022Document100 pagesMandatory Reviews Into Child Deaths: October 2021 - March 2022edmontonjournalNo ratings yet

- 2021-22 Oilers' You Be The Boss PollDocument16 pages2021-22 Oilers' You Be The Boss Polledmontonjournal0% (1)

- Edmonton Red Alerts FOIPDocument1 pageEdmonton Red Alerts FOIPKaren BartkoNo ratings yet

- Chinatown AccordDocument1 pageChinatown AccordedmontonjournalNo ratings yet

- 2021-22 Oilers' You Be The Boss PollDocument4 pages2021-22 Oilers' You Be The Boss PolledmontonjournalNo ratings yet

- Office of The Integrity Commissioner ReportDocument43 pagesOffice of The Integrity Commissioner ReportCTV News EdmontonNo ratings yet

- ECSD SRO EvaluationDocument69 pagesECSD SRO EvaluationKaren BartkoNo ratings yet

- Calgary Herald and Edmonton Journal - Provincial Issues Poll - Dec 9 2021Document53 pagesCalgary Herald and Edmonton Journal - Provincial Issues Poll - Dec 9 2021edmontonjournalNo ratings yet

- Justice and Solicitor General Letter To Edmonton Mayor Public Safety 2022-05-26Document3 pagesJustice and Solicitor General Letter To Edmonton Mayor Public Safety 2022-05-26edmontonjournalNo ratings yet

- Health Cmoh Order 39 2021 Exemption Designated Family Support Person Obstetrical PatientsDocument2 pagesHealth Cmoh Order 39 2021 Exemption Designated Family Support Person Obstetrical PatientsCTV CalgaryNo ratings yet

- Health Cmoh Order 39 2021 Exemption Designated Family Support Person Obstetrical PatientsDocument2 pagesHealth Cmoh Order 39 2021 Exemption Designated Family Support Person Obstetrical PatientsCTV CalgaryNo ratings yet

- COVID - Open Letter To PremierDocument4 pagesCOVID - Open Letter To PremieredmontonjournalNo ratings yet

- Dear AlbertansDocument3 pagesDear AlbertansedmontonjournalNo ratings yet

- VOCF Partners Letter To Premier 20200525Document3 pagesVOCF Partners Letter To Premier 20200525edmontonjournalNo ratings yet

- You're Not AloneDocument4 pagesYou're Not Aloneedmontonjournal100% (3)

- 2020 21 First Quarter Fiscal Update and Economic StatementDocument20 pages2020 21 First Quarter Fiscal Update and Economic StatementedmontonjournalNo ratings yet

- Physicians For Alberta HealthcareDocument11 pagesPhysicians For Alberta HealthcareAnonymous NbMQ9YmqNo ratings yet

- The Honourable Jason CoppingDocument3 pagesThe Honourable Jason Coppingedmontonjournal100% (1)

- COVID-19 Singing Risk Transmission Rapid ReviewDocument17 pagesCOVID-19 Singing Risk Transmission Rapid ReviewedmontonjournalNo ratings yet

- Dr. Mukarram Zaidi Letter To AlbertansDocument1 pageDr. Mukarram Zaidi Letter To AlbertansedmontonjournalNo ratings yet

- Open Letter From Doctors On MasksDocument4 pagesOpen Letter From Doctors On MasksedmontonjournalNo ratings yet

- BusinessDocument6 pagesBusinessn3xtnetworkNo ratings yet

- INE N: Franchisee Financial Controls Investment TemplateDocument2 pagesINE N: Franchisee Financial Controls Investment TemplatePatrick D'souzaNo ratings yet

- Exchange of Money Under of Transfer Property Act-1882Document7 pagesExchange of Money Under of Transfer Property Act-1882mayank kumarNo ratings yet

- Managing Finances Mock TestDocument8 pagesManaging Finances Mock TestThuy TranNo ratings yet

- Lums Leveragingthestyloshoesexperience 130119101835 Phpapp01Document20 pagesLums Leveragingthestyloshoesexperience 130119101835 Phpapp01Bushra UmarNo ratings yet

- Invoice PDFDocument1 pageInvoice PDFJesse ChenNo ratings yet

- Introduction Letter of Snapon ToolsDocument2 pagesIntroduction Letter of Snapon ToolsRajinder singhNo ratings yet

- Cold CallingDocument3 pagesCold Callingabhishekmohanty2No ratings yet

- Hetzner Invoice for Server HostingDocument1 pageHetzner Invoice for Server HostingArminNo ratings yet

- Activity Based Costing (ABC) .Document70 pagesActivity Based Costing (ABC) .irwansyah1617100% (4)

- Impact of Salesperson Behavior on Customer Perceived Service QualityDocument98 pagesImpact of Salesperson Behavior on Customer Perceived Service QualityJehan Marie GiananNo ratings yet

- ITC's Strategy to Diversify Beyond TobaccoDocument27 pagesITC's Strategy to Diversify Beyond Tobaccorohan48No ratings yet

- Sap Retail Two Step PricingDocument4 pagesSap Retail Two Step PricingShams TabrezNo ratings yet

- Measuring The Performance of Investment Centers Using RoiDocument9 pagesMeasuring The Performance of Investment Centers Using RoiIndah SetyoriniNo ratings yet

- Atul Industries Limited-IC PDFDocument23 pagesAtul Industries Limited-IC PDFSanjayNo ratings yet

- Contracts 2 - OutlineDocument60 pagesContracts 2 - Outlinembirdwell03No ratings yet

- Job Order Costing SystemsDocument38 pagesJob Order Costing SystemsNived Lrac Pdll Sgn50% (2)

- Project Manager Retail Supply Chain in Toronto Canada Resume Dwight WestacottDocument2 pagesProject Manager Retail Supply Chain in Toronto Canada Resume Dwight WestacottDwightWestacottNo ratings yet

- Describe Briefly The Rights As A Hirer UnderDocument9 pagesDescribe Briefly The Rights As A Hirer UnderMika MellonNo ratings yet

- Mercantile Bar Review Material 1Document209 pagesMercantile Bar Review Material 1shintaronikoNo ratings yet

- EBC - Understand The Business TemplateDocument6 pagesEBC - Understand The Business TemplateBenjie AquinoNo ratings yet

- Joshua Kennon What Is A FranchiseDocument6 pagesJoshua Kennon What Is A FranchiseNico A. Cotzias Jr.No ratings yet

- Analysis of Brand Quality & Customer Satisfaction Regarding With R.S.W.M.Document84 pagesAnalysis of Brand Quality & Customer Satisfaction Regarding With R.S.W.M.Jitendra VirahyasNo ratings yet

- Interbrand Design Forum Newsletter: How Design Drives Retail Brand ValueDocument4 pagesInterbrand Design Forum Newsletter: How Design Drives Retail Brand ValueBeth LingNo ratings yet

- CREDIT POLICY AND DIRECT BILLING AUTHORIZATIONDocument3 pagesCREDIT POLICY AND DIRECT BILLING AUTHORIZATIONshakeelzs78100% (3)

- Detailed Analysis of BigbasketDocument18 pagesDetailed Analysis of BigbasketRathan Devatha100% (3)

- WestmountDocument5 pagesWestmountsai chandra100% (1)

- Philip KotlerDocument3 pagesPhilip Kotlernantha74No ratings yet

- International MarketingDocument28 pagesInternational Marketingarnab_bhaskar100% (2)