You might also like

- Exponential and Logarithmic FunctionsDocument19 pagesExponential and Logarithmic FunctionsRamon GasgasNo ratings yet

- Online BankingDocument46 pagesOnline BankingNazmulHasanNo ratings yet

- Answer Key For Week 1 To 3 ULO 8 To 10Document7 pagesAnswer Key For Week 1 To 3 ULO 8 To 10Margaux Phoenix KimilatNo ratings yet

- Stop HuntingDocument3 pagesStop HuntingManuel Mora100% (2)

- Fundamentals of Corporate Finance 8th Edition Brealey Solutions Manual PDFDocument5 pagesFundamentals of Corporate Finance 8th Edition Brealey Solutions Manual PDFa819334331No ratings yet

- Project On Process CostingDocument11 pagesProject On Process CostingMukesh ManwaniNo ratings yet

- Employee DataDocument1 pageEmployee DataomkassNo ratings yet

- IvoryDocument20 pagesIvorycubadesignstudNo ratings yet

- Opportunity Assessment PlanDocument18 pagesOpportunity Assessment PlanSteffie67% (6)

- Horngren Ima16 Tif 07 GEDocument59 pagesHorngren Ima16 Tif 07 GEasem shaban100% (3)

- Mfglobaldaily 2 22 11Document4 pagesMfglobaldaily 2 22 11marketpanicNo ratings yet

- Mfglobaldaily 2 21 11Document6 pagesMfglobaldaily 2 21 11marketpanicNo ratings yet

- Mfglobaldaily 2 25 11Document3 pagesMfglobaldaily 2 25 11marketpanicNo ratings yet

- Metals Insight: A Daily Report On Base MetalsDocument8 pagesMetals Insight: A Daily Report On Base MetalsManish ChandakNo ratings yet

- Market Technical Reading: More Corrections Expected Going Forward... - 26/05/2010Document6 pagesMarket Technical Reading: More Corrections Expected Going Forward... - 26/05/2010Rhb InvestNo ratings yet

- Commodities: I Vayda BazaarDocument7 pagesCommodities: I Vayda Bazaarhitesh315No ratings yet

- Market Technical Reading - Losing 1,350 Will Confirm A Bearish Breakdown - 11/08/2010Document6 pagesMarket Technical Reading - Losing 1,350 Will Confirm A Bearish Breakdown - 11/08/2010Rhb InvestNo ratings yet

- SL No From To Scope Completed Section Date Balance WorkDocument3 pagesSL No From To Scope Completed Section Date Balance WorkDipankarHaloiNo ratings yet

- Derivative Report 6march2017Document6 pagesDerivative Report 6march2017ram sahuNo ratings yet

- MKT RPT 30 October 2020Document8 pagesMKT RPT 30 October 2020antonyNo ratings yet

- Stock Market Outlook by Mansukh Investment & Trading Solutions 29/07/2010Document5 pagesStock Market Outlook by Mansukh Investment & Trading Solutions 29/07/2010MansukhNo ratings yet

- Daily Trade Journal - 26.12.2013Document6 pagesDaily Trade Journal - 26.12.2013Randora LkNo ratings yet

- Daily Report 20141006Document3 pagesDaily Report 20141006Joseph DavidsonNo ratings yet

- Lima Tahun Kinerja Perekonomian IndonesiaDocument77 pagesLima Tahun Kinerja Perekonomian IndonesiaIand Novian NurtanioNo ratings yet

- Market Technical Reading: Avoid Catching A "Falling Knife"... - 25/05/2010Document6 pagesMarket Technical Reading: Avoid Catching A "Falling Knife"... - 25/05/2010Rhb InvestNo ratings yet

- MelanieDwl - 183 - Praktikum Pengelolaan Keuangan D - Pertemuan 3Document15 pagesMelanieDwl - 183 - Praktikum Pengelolaan Keuangan D - Pertemuan 3almaira oktaviaNo ratings yet

- Daily Commodity Report 10 Feb 2014 by EPIC RESEARCHDocument13 pagesDaily Commodity Report 10 Feb 2014 by EPIC RESEARCHNidhi JainNo ratings yet

- 14jan2013 Section02A Summary Volume and Open Interest Int Rates Futures and Options 2013009Document2 pages14jan2013 Section02A Summary Volume and Open Interest Int Rates Futures and Options 2013009avadcsNo ratings yet

- Market Overview (Economy) : Commodity Last CHG % CHGDocument3 pagesMarket Overview (Economy) : Commodity Last CHG % CHGAk ChowdaryNo ratings yet

- Daily Trade Journal - 25.07.2013Document6 pagesDaily Trade Journal - 25.07.2013Randora LkNo ratings yet

- Daily Report 20141201Document3 pagesDaily Report 20141201Joseph DavidsonNo ratings yet

- Daily Commodity Report 30 JANUARY 2013: WWW - Epicresearch.CoDocument6 pagesDaily Commodity Report 30 JANUARY 2013: WWW - Epicresearch.Coapi-196234891No ratings yet

- Daily Trade Journal - 20.02.2014Document6 pagesDaily Trade Journal - 20.02.2014Randora LkNo ratings yet

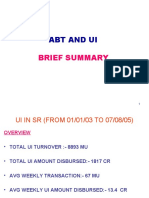

- Abt and Ui: Brief SummaryDocument8 pagesAbt and Ui: Brief Summarygaurang1111No ratings yet

- Markets and Commodity Figures: MetalsDocument1 pageMarkets and Commodity Figures: MetalsTiso Blackstar GroupNo ratings yet

- Daily Report 20141014Document3 pagesDaily Report 20141014Joseph DavidsonNo ratings yet

- China'S Mixed Slowdown: KWH (BN) 230.5 250.5 BN MT KMDocument7 pagesChina'S Mixed Slowdown: KWH (BN) 230.5 250.5 BN MT KMfakepocNo ratings yet

- Daily Report: News & UpdatesDocument3 pagesDaily Report: News & UpdatesМөнхбат ДоржпүрэвNo ratings yet

- Pulau PinangDocument14 pagesPulau PinangNoelle LeeNo ratings yet

- Employee CornerDocument4 pagesEmployee CornerNithya Prabhu RajagopalNo ratings yet

- Morning Notes 31.03.10Document5 pagesMorning Notes 31.03.10Mansukh Investment & Trading SolutionsNo ratings yet

- Index Flat Deals in JKH Boost Turnover : Tuesday, July 30, 2013Document6 pagesIndex Flat Deals in JKH Boost Turnover : Tuesday, July 30, 2013Randora LkNo ratings yet

- Line 191Document1 pageLine 191hyg7d5ry45No ratings yet

- Daily Trade Journal - 21.02.2014Document6 pagesDaily Trade Journal - 21.02.2014Randora LkNo ratings yet

- ANZ Commodity Daily 749 231112Document5 pagesANZ Commodity Daily 749 231112Luke Campbell-SmithNo ratings yet

- Nammaaaa 000007Document98 pagesNammaaaa 000007mohammad qaruishNo ratings yet

- US Gov 'T Debt To Stabilize at A High Level: Morning ReportDocument3 pagesUS Gov 'T Debt To Stabilize at A High Level: Morning Reportnaudaslietas_lvNo ratings yet

- Chapter 8Document52 pagesChapter 8raomahinNo ratings yet

- Weekly Report - 02 July 2021Document4 pagesWeekly Report - 02 July 2021Dan HathurusingheNo ratings yet

- Daily Trade Journal - 05.03.2014Document6 pagesDaily Trade Journal - 05.03.2014Randora LkNo ratings yet

- GDM 20190925Document4 pagesGDM 20190925Jorge A. Flores CruzNo ratings yet

- Indian Stock Market Outlook by Mansukh Investment & Trading Solutions 26/8/2010Document5 pagesIndian Stock Market Outlook by Mansukh Investment & Trading Solutions 26/8/2010MansukhNo ratings yet

- Morning Report 15oct2014Document2 pagesMorning Report 15oct2014Joseph DavidsonNo ratings yet

- Daily Commodity Report 1 February 2013: WWW - Epicresearch.CoDocument6 pagesDaily Commodity Report 1 February 2013: WWW - Epicresearch.Coapi-196234891No ratings yet

- No Scrips Under Ban For Trade Date 02-02-2011.: FEB-01-11 10:57 PM Page 1 of 38Document38 pagesNo Scrips Under Ban For Trade Date 02-02-2011.: FEB-01-11 10:57 PM Page 1 of 38vjain333No ratings yet

- Oib Daily Bulletin 29 Januari 2024Document14 pagesOib Daily Bulletin 29 Januari 2024damar wulanNo ratings yet

- Table 155: Foreign Investment Inflows: Year A. Direct Investment B. Portfolio Investment Total (A+B)Document5 pagesTable 155: Foreign Investment Inflows: Year A. Direct Investment B. Portfolio Investment Total (A+B)Saumya SinghNo ratings yet

- Silver's Demand and Supply in India at Micro LevelDocument9 pagesSilver's Demand and Supply in India at Micro Levelhimanshushah871006No ratings yet

- Daily Report 20150109Document3 pagesDaily Report 20150109Joseph DavidsonNo ratings yet

- Metals - March 22 2017Document1 pageMetals - March 22 2017Tiso Blackstar GroupNo ratings yet

- Towing and TaxiingDocument82 pagesTowing and TaxiingKeilaeFrancisco ArceNo ratings yet

- Daily Commodity Report 4 JANUARY 2013: WWW - Epicresearch.CoDocument6 pagesDaily Commodity Report 4 JANUARY 2013: WWW - Epicresearch.Coapi-196234891No ratings yet

- Daily Report 20141017Document3 pagesDaily Report 20141017Joseph DavidsonNo ratings yet

- 3rd Revised Rates 07 11 16.Document4 pages3rd Revised Rates 07 11 16.Mwansa MachaloNo ratings yet

- HistoryDocument16 pagesHistoryPratap SahooNo ratings yet

- ASPI Ends Flat S&P SL20 Falls With Liquid Big Caps : Thursday, February 13, 2014Document6 pagesASPI Ends Flat S&P SL20 Falls With Liquid Big Caps : Thursday, February 13, 2014Randora LkNo ratings yet

- Daily Trade Journal - 13.09.2013Document6 pagesDaily Trade Journal - 13.09.2013Randora LkNo ratings yet

- Statement of Account / نايب نم باسحلا: ليومتلاو تارامثتسلإل نامع ةكرش ش - م - ع - ع Oman Investment & Finance Co.SaogDocument8 pagesStatement of Account / نايب نم باسحلا: ليومتلاو تارامثتسلإل نامع ةكرش ش - م - ع - ع Oman Investment & Finance Co.SaograzibackerNo ratings yet

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaFrom EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaNo ratings yet

- Seya-Industries-Result-Presentation - Q1FY201 Seya IndustriesDocument24 pagesSeya-Industries-Result-Presentation - Q1FY201 Seya Industriesabhishek kalbaliaNo ratings yet

- Bank Alfalah Clearance DepartmentDocument7 pagesBank Alfalah Clearance Departmenthassan_shazaib100% (1)

- Probablity QuestionsDocument14 pagesProbablity QuestionsSetu Ahuja100% (1)

- Case Study Period 2Document4 pagesCase Study Period 2thomas gagnantNo ratings yet

- A Study On Financial Performance of Public Sector Banks in IndiaDocument38 pagesA Study On Financial Performance of Public Sector Banks in IndiaMehul ParmarNo ratings yet

- Eco Assignment 3Document2 pagesEco Assignment 3bushraNo ratings yet

- Grievance SGDocument41 pagesGrievance SGsandipgargNo ratings yet

- Pre and Post Shipment Unit IVDocument15 pagesPre and Post Shipment Unit IVvishesh_2211_1257207100% (1)

- Course DetailDocument3 pagesCourse DetailNajlaNo ratings yet

- August 19, 2016Document16 pagesAugust 19, 2016Anonymous KMKk9Msn5No ratings yet

- 39f6a5fb 23Document52 pages39f6a5fb 23moblogNo ratings yet

- Benjamin Yu vs. National Labor Relations Commission (NLRC) : Tri-Level Existence & Attributes 1Document1 pageBenjamin Yu vs. National Labor Relations Commission (NLRC) : Tri-Level Existence & Attributes 1Trisha Ace Betita ElisesNo ratings yet

- 09 Mapa V ArroyoDocument5 pages09 Mapa V ArroyoAirelle AvilaNo ratings yet

- File 261Document16 pagesFile 261Bharat Kumar PatelNo ratings yet

- Feasibility ReportDocument21 pagesFeasibility Reportzee abadillaNo ratings yet

- Major Types of Orders Available To Investors and Market Maker WEEK2 &3 LECT 2023Document57 pagesMajor Types of Orders Available To Investors and Market Maker WEEK2 &3 LECT 2023Manar AmrNo ratings yet

- Revitalization of Shahjahanabad (Walled City of Delhi) : - Project Concept ProposalDocument98 pagesRevitalization of Shahjahanabad (Walled City of Delhi) : - Project Concept ProposalVismay WadiwalaNo ratings yet

- The Financial Management Practices of Small and Medium EnterprisesDocument15 pagesThe Financial Management Practices of Small and Medium EnterprisesJa MieNo ratings yet

- v62 Form Honda CivicDocument2 pagesv62 Form Honda Civicdawudaaa9No ratings yet

- BP&EM External ImpsDocument19 pagesBP&EM External ImpsKiran ansurkarNo ratings yet

- CH 04Document4 pagesCH 04Nusirwan Mz50% (2)