0% found this document useful (0 votes)

2K views11 pagesProject On Process Costing

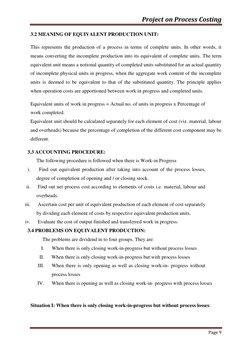

Process costing is an accounting methodology that traces and accumulates direct costs, and allocates indirect costs of a manufacturing process. It assigns average costs to each unit produced. Process costing is suitable for industries producing homogeneous products through continuous production processes. Key aspects of process costing include averaging unit costs across total production, accounting for normal and abnormal losses at each stage of production, and transferring costs between production stages until a finished product is completed. Process costing provides managers with cost information to monitor budgets and control manufacturing costs.

Uploaded by

Mukesh ManwaniCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

2K views11 pagesProject On Process Costing

Process costing is an accounting methodology that traces and accumulates direct costs, and allocates indirect costs of a manufacturing process. It assigns average costs to each unit produced. Process costing is suitable for industries producing homogeneous products through continuous production processes. Key aspects of process costing include averaging unit costs across total production, accounting for normal and abnormal losses at each stage of production, and transferring costs between production stages until a finished product is completed. Process costing provides managers with cost information to monitor budgets and control manufacturing costs.

Uploaded by

Mukesh ManwaniCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd