0% found this document useful (0 votes)

1K views10 pagesFeatures of Process Costing

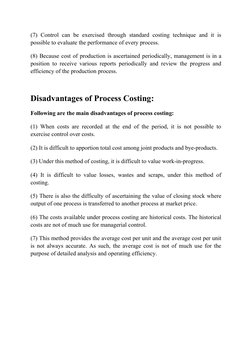

Process costing is a method used to calculate the cost of producing goods through sequential processes. It involves tracking the costs incurred at each stage of production and averaging them over total units produced. Costs like materials, labor, expenses are allocated to individual process accounts. The total cost of each process is divided by units produced to determine average cost per unit. Industries like chemicals, oil refining, cement use this method due to their continuous production processes.

Uploaded by

bcomh01097 UJJWAL SINGHCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

1K views10 pagesFeatures of Process Costing

Process costing is a method used to calculate the cost of producing goods through sequential processes. It involves tracking the costs incurred at each stage of production and averaging them over total units produced. Costs like materials, labor, expenses are allocated to individual process accounts. The total cost of each process is divided by units produced to determine average cost per unit. Industries like chemicals, oil refining, cement use this method due to their continuous production processes.

Uploaded by

bcomh01097 UJJWAL SINGHCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

- Process Costing Introduction

- Objectives and Elements of Process Costing

- Principles and Accumulation of Costs

- Advantages and Disadvantages of Process Costing

- Difference between Job Costing and Process Costing