You might also like

- And Then One Day A Memoir by Naseeruddin ShahDocument255 pagesAnd Then One Day A Memoir by Naseeruddin ShahSuhail AhmedNo ratings yet

- BIG BAZAR BareillyDocument59 pagesBIG BAZAR Bareillyrachit sharmaNo ratings yet

- A Research On Customer Awareness &: Branding in FMCG IndustryDocument13 pagesA Research On Customer Awareness &: Branding in FMCG Industryshakti shankerNo ratings yet

- 04.monster Pet Evolution Chapter 151 - Chapter 200Document300 pages04.monster Pet Evolution Chapter 151 - Chapter 200Abdul Muqeet RehanNo ratings yet

- Role of IT in Strategic HRMDocument7 pagesRole of IT in Strategic HRMChandan SrivastavaNo ratings yet

- Sample Synopsis For MBA DissertationDocument15 pagesSample Synopsis For MBA DissertationReshma Cp0% (1)

- Fast Moving Consumer Goods (FMCG)Document78 pagesFast Moving Consumer Goods (FMCG)Akanksha JindalNo ratings yet

- Fundamental Analysis of FMCG Sector (Ashish Chanchlani)Document61 pagesFundamental Analysis of FMCG Sector (Ashish Chanchlani)Ashish chanchlani79% (47)

- Women Growth in Corporate SectorDocument66 pagesWomen Growth in Corporate SectorShruti JainNo ratings yet

- Dissertation On Globalization and Its Effect On Marketing StratregiesDocument57 pagesDissertation On Globalization and Its Effect On Marketing Stratregiesvikas k86% (14)

- A Study Based On Comparative Financial Performance Analysis of Two Private Sector BanksDocument59 pagesA Study Based On Comparative Financial Performance Analysis of Two Private Sector BankshariniNo ratings yet

- Merged DocumentDocument93 pagesMerged DocumentsurekhaNo ratings yet

- Pratap Sip Report Oct 2015Document72 pagesPratap Sip Report Oct 2015Aniket DuhanNo ratings yet

- Strategy of Marketing Adopted by PaytmDocument81 pagesStrategy of Marketing Adopted by PaytmSONALINo ratings yet

- Green Marketing and Environmental Regulations: AnalysisDocument7 pagesGreen Marketing and Environmental Regulations: AnalysisInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Mba ProjectDocument25 pagesMba ProjectPraveen HJNo ratings yet

- Study of Consumer Buying Behaviour in Reliance Fresh New DelhiDocument78 pagesStudy of Consumer Buying Behaviour in Reliance Fresh New DelhiSid MishraNo ratings yet

- Akash Market Survey ReportDocument79 pagesAkash Market Survey ReportHemant JoshhiNo ratings yet

- A Study On Performance Appraisal System at BYJU's in Lucknow CityDocument44 pagesA Study On Performance Appraisal System at BYJU's in Lucknow CityChandan SrivastavaNo ratings yet

- Study of Indian Soap MarketDocument54 pagesStudy of Indian Soap MarketAnkit Bhardwaj90% (10)

- FMCG Case StudyDocument5 pagesFMCG Case StudyDini PutriNo ratings yet

- The Impact of Green Marketing Practices On Consumer Buying DecisionDocument130 pagesThe Impact of Green Marketing Practices On Consumer Buying DecisionpsychonomyNo ratings yet

- Mba Iii ProjectDocument70 pagesMba Iii ProjectmanojNo ratings yet

- Dissertation Report Flipkart Marketing StategiesDocument46 pagesDissertation Report Flipkart Marketing StategiesAvneesh KumarNo ratings yet

- A Report ON: Understand The Ecosystem in Digital Media MarketingDocument64 pagesA Report ON: Understand The Ecosystem in Digital Media MarketingRaghu RangapurNo ratings yet

- A PROJECT REPORT ON MBA ON ItDocument62 pagesA PROJECT REPORT ON MBA ON ItlalsinghNo ratings yet

- A Study On Customer Satisfaction Towards HCL Telecom Products in LucknowDocument33 pagesA Study On Customer Satisfaction Towards HCL Telecom Products in LucknowChandan SrivastavaNo ratings yet

- Dissertation Amit FinalDocument50 pagesDissertation Amit FinalHarish Chandra Jaiswal100% (1)

- Project On Axis BankDocument64 pagesProject On Axis BankSandeep GuneshwarNo ratings yet

- 2nd Sem Project Report NGOs Joshi JiiDocument44 pages2nd Sem Project Report NGOs Joshi JiiVirat SilswalNo ratings yet

- Study of Consumer Buying Behaviour in Reliance Fresh New DelhiDocument80 pagesStudy of Consumer Buying Behaviour in Reliance Fresh New DelhiAnkitSinghNo ratings yet

- Dissertation Report SumandeepDocument82 pagesDissertation Report SumandeepSumandeep Kaur Chambial0% (1)

- Project Report On "FACTORS AFFECTING BRAND CHOICE OF MOBILE PHONE HANDSETS"Document66 pagesProject Report On "FACTORS AFFECTING BRAND CHOICE OF MOBILE PHONE HANDSETS"Amit DhankharNo ratings yet

- A Comparative Study On Reliance Jio Vs AirtelDocument77 pagesA Comparative Study On Reliance Jio Vs AirtelRishabh RkNo ratings yet

- Marketing Strategy of LG ProjectDocument114 pagesMarketing Strategy of LG ProjectMohd ShahidNo ratings yet

- FMCG SectorDocument41 pagesFMCG SectorGurusaran SinghNo ratings yet

- Project Report On Study of Consumer Behaviour and Attitude Towards The Cellular Services With Refrence To AircelDocument108 pagesProject Report On Study of Consumer Behaviour and Attitude Towards The Cellular Services With Refrence To AircelSANDEEP SINGH100% (8)

- Winter ProjectDocument73 pagesWinter Projectranjitkumar828No ratings yet

- Final ThesisDocument225 pagesFinal ThesisAnonymous VdwBhb4frFNo ratings yet

- MPR Project Report Sample FormatDocument24 pagesMPR Project Report Sample FormatArya khattarNo ratings yet

- Naveen ProjectDocument47 pagesNaveen ProjectNaveenNo ratings yet

- Ok A Study On Consumer Buying Behavior of Retail Industry With Special References To Big Bazaar in Ranchi"Document83 pagesOk A Study On Consumer Buying Behavior of Retail Industry With Special References To Big Bazaar in Ranchi"Parshant GargNo ratings yet

- Deepak Dissertation Report Smartphones1Document55 pagesDeepak Dissertation Report Smartphones1Mohit JoshiNo ratings yet

- A Project Report Study About The Consumer Behaviour On Online ShoppingDocument68 pagesA Project Report Study About The Consumer Behaviour On Online ShoppingKapil Sambhnani100% (1)

- Internet Marketing Full Project ReportDocument77 pagesInternet Marketing Full Project Reportaurorashiva1No ratings yet

- Project On Brand Awareness of ICICI Prudential by SajadDocument99 pagesProject On Brand Awareness of ICICI Prudential by SajadSajadul Ashraf71% (7)

- Mini Project 2 (Sajal Gupta) (Roll No - 2001240700119)Document47 pagesMini Project 2 (Sajal Gupta) (Roll No - 2001240700119)Shivam PathakNo ratings yet

- Sybba ProjectsDocument72 pagesSybba Projectsproject guide100% (1)

- A Study On Green Marketing Initiative by Leading Corporation Takin Nokia As CaseDocument79 pagesA Study On Green Marketing Initiative by Leading Corporation Takin Nokia As CaseSami ZamaNo ratings yet

- COMPARATIVE STUDY OF CUSTOMER SATISFACTION TOWARD PERFORMANCE OF HERO HONDA, TVS AND BAJAJ BIKES by Deshraj SinghDocument67 pagesCOMPARATIVE STUDY OF CUSTOMER SATISFACTION TOWARD PERFORMANCE OF HERO HONDA, TVS AND BAJAJ BIKES by Deshraj Singharunkitty100% (1)

- Project Report On Rural MarketingDocument117 pagesProject Report On Rural MarketingAdeel KhanNo ratings yet

- BRM Mini ProjectDocument55 pagesBRM Mini ProjectAshish Ranjan100% (3)

- FMCG Dissertation ReportDocument70 pagesFMCG Dissertation ReportNaman RastogiNo ratings yet

- Fundamental Analysis of FMCG Sector Ashish Chanchlani PDFDocument61 pagesFundamental Analysis of FMCG Sector Ashish Chanchlani PDFSAKSHI KHAITAN0% (1)

- Strategic Impact of Electronic Media For FMCG Products in Rural MarketDocument116 pagesStrategic Impact of Electronic Media For FMCG Products in Rural MarketManjeet SinghNo ratings yet

- Cargill India Private Limited: Market Mapping of Fragmented Food ServiceDocument39 pagesCargill India Private Limited: Market Mapping of Fragmented Food ServiceMohammad SabaNo ratings yet

- FCMG ProjectDocument72 pagesFCMG ProjectsbraajaNo ratings yet

- Shubhbham Singh 50080801Document65 pagesShubhbham Singh 50080801ssrana26No ratings yet

- Subhi ReportDocument89 pagesSubhi ReportSubhash PrajapatNo ratings yet

- ECO531Document15 pagesECO531Naureen ShabnamNo ratings yet

- A1Document121 pagesA1Sanjay NgarNo ratings yet

- A STUDY ON MARKETING STRATEGIES IN FMCG IN RELATION WITH HIDUSTAN UNILEVER LIMITED. Research ReportDocument84 pagesA STUDY ON MARKETING STRATEGIES IN FMCG IN RELATION WITH HIDUSTAN UNILEVER LIMITED. Research ReportMaaz AbdullahNo ratings yet

- Assignment GuidelinesDocument3 pagesAssignment Guidelinesvandana chandraNo ratings yet

- A Presentation On Effect of Recession On AgricultureDocument17 pagesA Presentation On Effect of Recession On Agriculturevandana chandra100% (3)

- Dissertation ReportDocument79 pagesDissertation Reportvandana chandra100% (14)

- Dissertation ReportDocument79 pagesDissertation Reportvandana chandra100% (14)

- NEW MESS MENU 2023 To 2024Document5 pagesNEW MESS MENU 2023 To 2024Vijaya LakshmiNo ratings yet

- Preguntas LógicaDocument15 pagesPreguntas LógicaBorja López NavarroNo ratings yet

- The Siouan Indians by McGee, W. J. (William John), 1853-1912Document48 pagesThe Siouan Indians by McGee, W. J. (William John), 1853-1912Gutenberg.orgNo ratings yet

- Mercy Corps Cash Transfer Programming Toolkit Part 1Document93 pagesMercy Corps Cash Transfer Programming Toolkit Part 1Jacopo SegniniNo ratings yet

- Active Listings ReportDocument19 pagesActive Listings ReportvishalNo ratings yet

- Chettinad Chicken Sanjeev KapoorDocument3 pagesChettinad Chicken Sanjeev Kapoorgsekar74No ratings yet

- I. Dạng điền khuyêt câu: Word form hsg 8Document11 pagesI. Dạng điền khuyêt câu: Word form hsg 8Ken Bi100% (2)

- François Rabelais - Gargantua and PantagruelDocument2 pagesFrançois Rabelais - Gargantua and PantagruelАлина СладкаедкаNo ratings yet

- Halal List enDocument2 pagesHalal List ensilver lauNo ratings yet

- Lesson 6 On Galantine Ballotine Roulade N ParfaitDocument5 pagesLesson 6 On Galantine Ballotine Roulade N ParfaitBonophool BanerjeeNo ratings yet

- Diwali Gifts PANKAJDocument3 pagesDiwali Gifts PANKAJharshitaNo ratings yet

- Case Study On Akshaya Patra Group-1Document9 pagesCase Study On Akshaya Patra Group-1swaroopNo ratings yet

- Leadership Journey: Region 4 (Group A) August 17, 2022Document19 pagesLeadership Journey: Region 4 (Group A) August 17, 2022Archu ArchuNo ratings yet

- 20 Traditional Salvadoran Foods To Try TodayDocument5 pages20 Traditional Salvadoran Foods To Try TodayMagaly RivasNo ratings yet

- Cookbook FrittataDocument2 pagesCookbook FrittataJilly CookeNo ratings yet

- Market Comparison of Cadbury, Nestle & GSKDocument89 pagesMarket Comparison of Cadbury, Nestle & GSKRajat Gupta100% (1)

- Kim Il Sung - Memórias No Transcurso Do Século Vol. 3 (INGLÊS) PDFDocument623 pagesKim Il Sung - Memórias No Transcurso Do Século Vol. 3 (INGLÊS) PDFLuigi AroneNo ratings yet

- WBCS 2020 (Preliminary) MOCK TEST No.: 5 (Answer Paper) Full Marks-200 Time-2 Hr. 30 MinDocument46 pagesWBCS 2020 (Preliminary) MOCK TEST No.: 5 (Answer Paper) Full Marks-200 Time-2 Hr. 30 Minsouparna duttaNo ratings yet

- Bart Anthologies Ug9 Final PDFDocument134 pagesBart Anthologies Ug9 Final PDFdinaNo ratings yet

- 1975 Hedges Notes On The Kumeyaay 1975Document15 pages1975 Hedges Notes On The Kumeyaay 1975Josep Romans FontacabaNo ratings yet

- Vegeterian Banquet MenuDocument4 pagesVegeterian Banquet Menuajay goelNo ratings yet

- Lib-Ushistory-Clash-Between-Spanish-Aztec-27786-Article OnlyDocument3 pagesLib-Ushistory-Clash-Between-Spanish-Aztec-27786-Article Onlyapi-260397974No ratings yet

- Current Affairs Pocket PDF - June 2020 by AffairsCloud PDFDocument84 pagesCurrent Affairs Pocket PDF - June 2020 by AffairsCloud PDFShivam AnandNo ratings yet

- The Human Right To Food in India: January 2002Document12 pagesThe Human Right To Food in India: January 2002Gayathri SNo ratings yet

- Samut Songkhram - Amazing Thailand EbookDocument44 pagesSamut Songkhram - Amazing Thailand EbookBlue LangurNo ratings yet

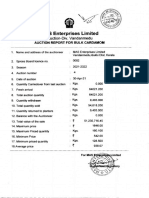

- Enterprises Limited: Auction-Div, VandanmeduDocument16 pagesEnterprises Limited: Auction-Div, VandanmeduRoshniNo ratings yet

- Conditionals VIIDocument8 pagesConditionals VIICamila Veilchen OliveiraNo ratings yet

- Menu Plan For Postnatal MothersDocument1 pageMenu Plan For Postnatal MothersNandhini ShreeNo ratings yet