You might also like

- Acoute Guide to McConnell Brue and Flynn's Microeconomics: Problems, Principles, and Policies (20th edition)From EverandAcoute Guide to McConnell Brue and Flynn's Microeconomics: Problems, Principles, and Policies (20th edition)Rating: 3.5 out of 5 stars3.5/5 (2)

- Fake Marketing Dilemmas: The Folly of Making Complex Marketing Issues SimpleFrom EverandFake Marketing Dilemmas: The Folly of Making Complex Marketing Issues SimpleNo ratings yet

- The Seventh Commandment: Walk Before You RunDocument11 pagesThe Seventh Commandment: Walk Before You RunDavid 'Valiant' OnyangoNo ratings yet

- SubtitleDocument2 pagesSubtitleBlack LotusNo ratings yet

- Ge Matrix NotesDocument13 pagesGe Matrix Notes51095BRizwana KhojaNo ratings yet

- Facebook'S Mark Zuckerberg Is Having A Great Year: Net Worth Up From $24.7B To $31.6B Betweejn Jan 3 and Mar 12, 2014Document10 pagesFacebook'S Mark Zuckerberg Is Having A Great Year: Net Worth Up From $24.7B To $31.6B Betweejn Jan 3 and Mar 12, 2014Vj LaxmananNo ratings yet

- Managerial Accounting Homework AnswersDocument7 pagesManagerial Accounting Homework AnswersafodbokhsblprdNo ratings yet

- Microeconomics Assignment S1G3Document14 pagesMicroeconomics Assignment S1G3Ankur Rana100% (1)

- James Montier WhatGoesUpDocument8 pagesJames Montier WhatGoesUpdtpalfiniNo ratings yet

- M&A: Concepts and Theories: New York Institute of FinanceDocument6 pagesM&A: Concepts and Theories: New York Institute of FinanceBhuwanNo ratings yet

- Name - Eco200: Practice Test 3A Covering Chapters 16, 18-21Document6 pagesName - Eco200: Practice Test 3A Covering Chapters 16, 18-21Thiện ThảoNo ratings yet

- Unit7 Feb2015 PDFDocument32 pagesUnit7 Feb2015 PDFJared OlivarezNo ratings yet

- Macro Economy Today 14th Edition Schiller Solutions Manual 1Document36 pagesMacro Economy Today 14th Edition Schiller Solutions Manual 1kimberlywillistockexfgbq100% (20)

- Valuing Dot ComsDocument11 pagesValuing Dot ComsEchuOkan1No ratings yet

- The FaceBook FutureDocument24 pagesThe FaceBook FutureVJLaxmananNo ratings yet

- What Is Economics About? Part OneDocument14 pagesWhat Is Economics About? Part Onesaqib razaNo ratings yet

- How To Read and Analyze An Income StatementDocument5 pagesHow To Read and Analyze An Income StatementsaketNo ratings yet

- Foundations of Economics 7th Edition Bade Solutions Manual DownloadDocument12 pagesFoundations of Economics 7th Edition Bade Solutions Manual DownloadFaith Pritchett100% (19)

- Whitepaper Risk Analysis Using The DuPont ModelDocument8 pagesWhitepaper Risk Analysis Using The DuPont ModelMartin HislopNo ratings yet

- Decision Trees QuestionsDocument2 pagesDecision Trees QuestionsSaeed Rahaman0% (1)

- Econ 112: Review For Final ExamDocument9 pagesEcon 112: Review For Final ExamOmar RaoufNo ratings yet

- Ec103 Week 01 s14Document32 pagesEc103 Week 01 s14юрий локтионовNo ratings yet

- Contemporary Management Cases and Assigments (1) v.2Document22 pagesContemporary Management Cases and Assigments (1) v.2osama sallamNo ratings yet

- Best Buy Business AnalysisDocument11 pagesBest Buy Business Analysisraheem34No ratings yet

- Aritmetica de MarketingDocument2 pagesAritmetica de MarketingJohn VelásquezNo ratings yet

- New Microsoft Word DocumentDocument85 pagesNew Microsoft Word DocumentniveditasharmaNo ratings yet

- David Einhorn MSFT Speech-2006Document5 pagesDavid Einhorn MSFT Speech-2006mikesfbayNo ratings yet

- ECMT2130: Semester 2, 2020 Assignment: Geoff Shuetrim Geoffrey - Shuetrim@sydney - Edu.au University of SydneyDocument7 pagesECMT2130: Semester 2, 2020 Assignment: Geoff Shuetrim Geoffrey - Shuetrim@sydney - Edu.au University of SydneyDaniyal AsifNo ratings yet

- Michael Baye AnswerDocument6 pagesMichael Baye AnswerHarsya FitrioNo ratings yet

- BUSAD 101 - Disussion 9Document5 pagesBUSAD 101 - Disussion 9maryNo ratings yet

- Entrep Q2 W2Document16 pagesEntrep Q2 W2Jaw Use EmpuestoNo ratings yet

- 03 Bill French - Accountant - StudentsDocument23 pages03 Bill French - Accountant - StudentsFiroz AhmadNo ratings yet

- Exercises Tutoring 20230526 SolDocument9 pagesExercises Tutoring 20230526 SolomerogolddNo ratings yet

- Contemporary Management Cases and Assigments (1) v.2Document22 pagesContemporary Management Cases and Assigments (1) v.2osama sallamNo ratings yet

- Eco685notes Intro ProdDocument28 pagesEco685notes Intro ProdAnjali Dharam Dutt VyasNo ratings yet

- Sales Forecasting ExampleDocument2 pagesSales Forecasting ExampleArash MazandaraniNo ratings yet

- Mix Matters: by Frank WarthenDocument13 pagesMix Matters: by Frank WarthenKaranveerGrewalNo ratings yet

- Seminar Assignments Roche CaseDocument7 pagesSeminar Assignments Roche CaseChristophe SieberNo ratings yet

- Seminar 3 - SolutionsDocument7 pagesSeminar 3 - SolutionsphuongfeoNo ratings yet

- Zeke Ashton Apples To ApplesDocument30 pagesZeke Ashton Apples To ApplesValueWalk100% (1)

- Monopoly Game Research PaperDocument7 pagesMonopoly Game Research Paperxactrjwgf100% (1)

- Macroeconomics Understanding The Global Economy 3rd Edition Miles Solutions ManualDocument36 pagesMacroeconomics Understanding The Global Economy 3rd Edition Miles Solutions ManualprunellamarsingillusNo ratings yet

- Riphah International University: ConclusionDocument11 pagesRiphah International University: ConclusionSid MalikNo ratings yet

- AdvertisingDocument2 pagesAdvertisingIsabel FontesNo ratings yet

- Case StudyDocument11 pagesCase StudyKester NdabaiNo ratings yet

- Production Possibility Frontier ("PPF")Document6 pagesProduction Possibility Frontier ("PPF")New1122No ratings yet

- Pareto Efficiency: 10.f. Pareto Efficiency Productive, Consumptive, and Trade EfficiencyDocument6 pagesPareto Efficiency: 10.f. Pareto Efficiency Productive, Consumptive, and Trade EfficiencysamNo ratings yet

- Completed Chapter 2 Mini Case Excel Working Papers FA14Document4 pagesCompleted Chapter 2 Mini Case Excel Working Papers FA14ZachLovingNo ratings yet

- Building Your CSR Business StrategyDocument12 pagesBuilding Your CSR Business StrategyDhiraj SarmahNo ratings yet

- The Bottom LineDocument2 pagesThe Bottom LineFunCity NigeriaNo ratings yet

- Tugas Game Theory 18-23Document5 pagesTugas Game Theory 18-23Hardian EkaputraNo ratings yet

- Final Report On InnovationDocument36 pagesFinal Report On InnovationSudhir ChoudharyNo ratings yet

- ECO402-FinalTerm MegafileDocument110 pagesECO402-FinalTerm MegafileAb DulNo ratings yet

- Yahoo Inc Maximum Point On The Profits-Revenues GraphDocument38 pagesYahoo Inc Maximum Point On The Profits-Revenues GraphVJLaxmananNo ratings yet

- Marketing ProblemsDocument10 pagesMarketing Problemsdgomez_512133No ratings yet

- Accounting Textbook Solutions - 30Document19 pagesAccounting Textbook Solutions - 30acc-expertNo ratings yet

- Concept Questions w6Document31 pagesConcept Questions w6Sadia AdamNo ratings yet

- Seizing the White Space (Review and Analysis of Johnson's Book)From EverandSeizing the White Space (Review and Analysis of Johnson's Book)No ratings yet

- Prince George Alexander Louis of Cambridge and The Precession of EquinoxesDocument33 pagesPrince George Alexander Louis of Cambridge and The Precession of EquinoxesVJLaxmananNo ratings yet

- Mayor Bloomberg's Comparison of NYC Homicide Rates and Wall Street's Ratio AnalysisDocument15 pagesMayor Bloomberg's Comparison of NYC Homicide Rates and Wall Street's Ratio AnalysisVJLaxmananNo ratings yet

- Trust Me, The Financial World Will Change Forever If Wall Street Starts Analyzing Financial Data Like We Do Baseball Stats: Miguel CabreraDocument38 pagesTrust Me, The Financial World Will Change Forever If Wall Street Starts Analyzing Financial Data Like We Do Baseball Stats: Miguel CabreraVj LaxmananNo ratings yet

- The Correlation Between Highway Deaths and The US EconomyDocument21 pagesThe Correlation Between Highway Deaths and The US EconomyVJLaxmananNo ratings yet

- Gun Violence in America: Americans Are Killing Themselves NOT Each Other Across StatesDocument22 pagesGun Violence in America: Americans Are Killing Themselves NOT Each Other Across StatesVJLaxmananNo ratings yet

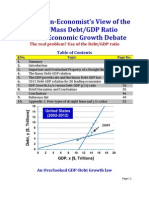

- An MIT Non-Economist's View of The Harvard-UMass Debt/GDP Ratio and The Economic Growth DebateDocument74 pagesAn MIT Non-Economist's View of The Harvard-UMass Debt/GDP Ratio and The Economic Growth DebateVJLaxmananNo ratings yet

- The Average Net Worth by Country Part 1: Introducing The X-Y DiagramDocument14 pagesThe Average Net Worth by Country Part 1: Introducing The X-Y DiagramVJLaxmananNo ratings yet

- Growth in The Combined Net Worth of Billionaires From 2000-2013: An Interesting Limit To Growth Is RevealedDocument11 pagesGrowth in The Combined Net Worth of Billionaires From 2000-2013: An Interesting Limit To Growth Is RevealedVJLaxmananNo ratings yet

- Derivation of Plancks Formula Radiation Chapter10Document14 pagesDerivation of Plancks Formula Radiation Chapter10TewodrosNo ratings yet

- Nda 2020 Gat Sol 37Document52 pagesNda 2020 Gat Sol 37Keshab Chandra BihariNo ratings yet

- Gamma Attenuation and ShieldingDocument11 pagesGamma Attenuation and ShieldingAhmedAmer1No ratings yet

- Class Worksheet Atomic Structure - Problems 2021-22: H N 4 Mze/4 1 H N 4 Mze/4Document4 pagesClass Worksheet Atomic Structure - Problems 2021-22: H N 4 Mze/4 1 H N 4 Mze/4RAVI ANANTHAKRISHNANNo ratings yet

- AewStructure of Atom (Narayana)Document39 pagesAewStructure of Atom (Narayana)majji satish33% (3)

- Photoelectron SpectrosDocument24 pagesPhotoelectron SpectrosUmesh ChandraNo ratings yet

- 16 Atomic Structure SolutionDocument34 pages16 Atomic Structure SolutionVINOD JINo ratings yet

- Questions 1 - 4 Are Worth Two Points Each. Questions 5 - 28 Are Worth Four Points EachDocument5 pagesQuestions 1 - 4 Are Worth Two Points Each. Questions 5 - 28 Are Worth Four Points EachLouis ParrNo ratings yet

- Atomic StructureDocument32 pagesAtomic StructureHarshNo ratings yet

- 26.electron & PhotonDocument27 pages26.electron & Photonrakeshece0701No ratings yet

- Exploring Gamma RayDocument9 pagesExploring Gamma RayChloe SoleNo ratings yet

- Chapter 4 Scintillation Detectors: 4.1. Basic Principle of The ScintillatorDocument10 pagesChapter 4 Scintillation Detectors: 4.1. Basic Principle of The ScintillatorbbkanilNo ratings yet

- Mt1 (Physics)Document4 pagesMt1 (Physics)Amaranath GovindollaNo ratings yet

- Aakash 10 - Dual Nature of Matter and RadiationDocument4 pagesAakash 10 - Dual Nature of Matter and RadiationTanishqNo ratings yet

- Handbook On The Physics and Chemistry of Rare Earths Vol. 10 PDFDocument611 pagesHandbook On The Physics and Chemistry of Rare Earths Vol. 10 PDFNilmar CamiloNo ratings yet

- As CT2 - Mechanics, Waves and QuantumDocument9 pagesAs CT2 - Mechanics, Waves and QuantumShabbir H. KhanNo ratings yet

- Chapter 2 Structure of AtomDocument48 pagesChapter 2 Structure of AtomRehan AhmadNo ratings yet

- Physics HSCDocument2 pagesPhysics HSCmothermonkNo ratings yet

- OpticsI 01 Light P (E)Document41 pagesOpticsI 01 Light P (E)Ma'ruf FarizalNo ratings yet

- 2022 Jee Advanced 7 Paper 2Document13 pages2022 Jee Advanced 7 Paper 2Rajat Verma X D 39No ratings yet

- Physical Chemistry IIDocument70 pagesPhysical Chemistry IIAyobami Akindele50% (2)

- Standard-Standard - Science Science 12 12: Sankalya Sankalya Paperset PapersetDocument31 pagesStandard-Standard - Science Science 12 12: Sankalya Sankalya Paperset PapersetGaming CoreNo ratings yet

- Structure of AtomDocument35 pagesStructure of Atommayashankarjha100% (1)

- Physical Sciences P1 Feb March 2018 EngDocument20 pagesPhysical Sciences P1 Feb March 2018 EngKoketso LetswaloNo ratings yet

- PHY098Document9 pagesPHY098Syarifah Anis AqilaNo ratings yet

- 10+2 Question Bank Final PDFDocument38 pages10+2 Question Bank Final PDFS RajNo ratings yet

- Project On Photoelectric Effect Class 12Document24 pagesProject On Photoelectric Effect Class 12fizakouser1216100% (4)

- Class 11 Chemistry Chapter 2 Structure of AtomDocument15 pagesClass 11 Chemistry Chapter 2 Structure of AtomgokulNo ratings yet

- Einstein's Equation and Wave-Particle DualityDocument12 pagesEinstein's Equation and Wave-Particle Duality8hhznfvp2sNo ratings yet

- Xi Chemistry Patna RegionDocument202 pagesXi Chemistry Patna RegionBhupenderYadavNo ratings yet