You might also like

- Tablel 9: Years 1990 and 2000)Document8 pagesTablel 9: Years 1990 and 2000)porkstarNo ratings yet

- High Taxes HurtDocument7 pagesHigh Taxes HurtZachary JanowskiNo ratings yet

- Property Tax Cap - 745pm PDFDocument16 pagesProperty Tax Cap - 745pm PDFjspectorNo ratings yet

- By The Numbers: What Government Costs in North Carolina Cities and Counties FY 2006Document45 pagesBy The Numbers: What Government Costs in North Carolina Cities and Counties FY 2006John Locke FoundationNo ratings yet

- BenchmarkingFY2015 TaxSpendDebt FINALDocument4 pagesBenchmarkingFY2015 TaxSpendDebt FINALjspectorNo ratings yet

- Millionaire Migration and State Taxation of Top Incomes: Evidence From A Natural ExperimentDocument30 pagesMillionaire Migration and State Taxation of Top Incomes: Evidence From A Natural ExperimentnextSTL.comNo ratings yet

- Taxation of An IndividualDocument15 pagesTaxation of An IndividualsahilNo ratings yet

- MN Income Migration 2016Document24 pagesMN Income Migration 2016John HinderakerNo ratings yet

- Top Ten States With The Highest Tax BurdenDocument3 pagesTop Ten States With The Highest Tax BurdenAndreea Anamaria WNo ratings yet

- Faux Populism: Rutland HeraldDocument2 pagesFaux Populism: Rutland HeraldvernalNo ratings yet

- Sales Tax: Main ArticleDocument1 pageSales Tax: Main ArticleMaika J. PudaderaNo ratings yet

- Tax BriefDocument3 pagesTax BriefHelen BennettNo ratings yet

- Taxes Really Do Matter: Look at The States: by Arthur B. Laffer, Ph.D. & Stephen MooreDocument20 pagesTaxes Really Do Matter: Look at The States: by Arthur B. Laffer, Ph.D. & Stephen Mooreuzibg2012No ratings yet

- Difference Between Indian and United State tXATION SystemDocument8 pagesDifference Between Indian and United State tXATION SystemamitNo ratings yet

- Property Tax and Income - Brief - FINALDocument9 pagesProperty Tax and Income - Brief - FINALThe GazetteNo ratings yet

- Local Property Tax ReformDocument2 pagesLocal Property Tax ReformTPPFNo ratings yet

- A Roadmap To BetterDocument16 pagesA Roadmap To BetterTexas Comptroller of Public AccountsNo ratings yet

- Affordability Crisis: New YorkDocument14 pagesAffordability Crisis: New YorkrkarlinNo ratings yet

- "High Rate" Income Tax States Are Outperforming No-Tax StatesDocument7 pages"High Rate" Income Tax States Are Outperforming No-Tax StatesfryingpannewsNo ratings yet

- 2014 Roadmap To RenewalDocument22 pages2014 Roadmap To RenewalsuzanneyankeeNo ratings yet

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxFrom EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNo ratings yet

- Taken, Is Greater Than $0Document2 pagesTaken, Is Greater Than $0bdlimmNo ratings yet

- Who Pays Report PDFDocument139 pagesWho Pays Report PDFChris JosephNo ratings yet

- Lanier 2010Document94 pagesLanier 2010AIG at ECUNo ratings yet

- Reexamining The Border Tax Effect: A Case Study of Washington StateDocument30 pagesReexamining The Border Tax Effect: A Case Study of Washington Statepetermc89No ratings yet

- US Government Economics - Local, State and Federal | How Taxes and Government Spending Work | 4th Grade Children's Government BooksFrom EverandUS Government Economics - Local, State and Federal | How Taxes and Government Spending Work | 4th Grade Children's Government BooksNo ratings yet

- Reforming The New York Tax Code: A Fiscal Policy Institute Report December 5, 2011Document25 pagesReforming The New York Tax Code: A Fiscal Policy Institute Report December 5, 2011fmauro7531No ratings yet

- How Does The Deduction For State and Local Taxes Work?Document3 pagesHow Does The Deduction For State and Local Taxes Work?hritik guptaNo ratings yet

- The 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingDocument23 pagesThe 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingA.J. MacDonald, Jr.No ratings yet

- What Are TaxesDocument7 pagesWhat Are TaxesNasir AliNo ratings yet

- Fundamental State Tax ReformDocument40 pagesFundamental State Tax ReformPaul BedardNo ratings yet

- Undocumented Immigrants in Texas Cost and BenefitsDocument24 pagesUndocumented Immigrants in Texas Cost and BenefitsLatinos Ready To VoteNo ratings yet

- Unpacking The State and Local Tax Toolkit Sources of State and Local Tax Collections FY 2020Document16 pagesUnpacking The State and Local Tax Toolkit Sources of State and Local Tax Collections FY 2020gjehle57No ratings yet

- Empire State Freedom Plan - 9-28-18Document23 pagesEmpire State Freedom Plan - 9-28-18MolinaroNo ratings yet

- Gr9 12lesson9 PDFDocument10 pagesGr9 12lesson9 PDFbekbek12No ratings yet

- Economics 100 Class 20Document15 pagesEconomics 100 Class 20idealparrotNo ratings yet

- University of Central Punjab: Assignment No 1 SubjectDocument8 pagesUniversity of Central Punjab: Assignment No 1 SubjectXh MuneebNo ratings yet

- Top Ten States With The Lowest Tax BurdenDocument3 pagesTop Ten States With The Lowest Tax BurdenAndreea Anamaria WNo ratings yet

- Big Bank Tax DrainDocument25 pagesBig Bank Tax DrainpublicaccountabilityNo ratings yet

- Crowley Tax Reform Case Studies v1Document37 pagesCrowley Tax Reform Case Studies v1MahnoorNo ratings yet

- 2009 State Tax TrendsDocument16 pages2009 State Tax TrendsArgyll Lorenzo BongosiaNo ratings yet

- A Tale of Three TaxpayersDocument16 pagesA Tale of Three TaxpayersMercatus Center at George Mason UniversityNo ratings yet

- Illinois IllustratedDocument64 pagesIllinois IllustratedReboot IllinoisNo ratings yet

- Immigration Council - Adding Up The BillionsDocument6 pagesImmigration Council - Adding Up The BillionsRoberto RamosNo ratings yet

- Projected Tax Growth 2013Document10 pagesProjected Tax Growth 2013Nick ReismanNo ratings yet

- Tax Resource 2011Document4 pagesTax Resource 2011Mark SnyderNo ratings yet

- Tri-Counties Libertarian Party Email To Representatives Bourne, Scherer and Halbrook: April 7, 2017Document5 pagesTri-Counties Libertarian Party Email To Representatives Bourne, Scherer and Halbrook: April 7, 2017Jake LeonardNo ratings yet

- Pa Nov 2016Document6 pagesPa Nov 2016Vikram rajputNo ratings yet

- Federal Estate Tax Disadvantages For Same-Sex Couples: July 2009Document27 pagesFederal Estate Tax Disadvantages For Same-Sex Couples: July 2009legalmattersNo ratings yet

- HF2480 Article 1 Section 8-9 Incidence Analysis 1 PDFDocument5 pagesHF2480 Article 1 Section 8-9 Incidence Analysis 1 PDFminnesoda238No ratings yet

- Homeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransFrom EverandHomeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransNo ratings yet

- Top20-New York PDFDocument2 pagesTop20-New York PDFrkarlinNo ratings yet

- Chapter 1-Solutions-Spring 2020Document18 pagesChapter 1-Solutions-Spring 2020Rashaf RazakNo ratings yet

- Summary: Flat Tax Revolution: Review and Analysis of Steve Forbes's BookFrom EverandSummary: Flat Tax Revolution: Review and Analysis of Steve Forbes's BookNo ratings yet

- The Benefit and The Burden: Tax Reform-Why We Need It and What It Will TakeFrom EverandThe Benefit and The Burden: Tax Reform-Why We Need It and What It Will TakeRating: 3.5 out of 5 stars3.5/5 (2)

- Summary: The Fair Tax Book: Review and Analysis of Neal Boortz and John Linder's BookFrom EverandSummary: The Fair Tax Book: Review and Analysis of Neal Boortz and John Linder's BookNo ratings yet

- Global Tax Revolution: The Rise of Tax Competition and the Battle to Defend ItFrom EverandGlobal Tax Revolution: The Rise of Tax Competition and the Battle to Defend ItNo ratings yet

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

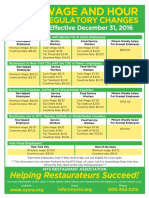

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- PD10011 LF9050 Venturi Combo Lube Filter Performance DatasheetDocument2 pagesPD10011 LF9050 Venturi Combo Lube Filter Performance DatasheetCristian Navarro AriasNo ratings yet

- Assessment Guidelines For Processing Operations Hydrocarbons VQDocument47 pagesAssessment Guidelines For Processing Operations Hydrocarbons VQMatthewNo ratings yet

- Corporation True or FalseDocument2 pagesCorporation True or FalseAllyza Magtibay50% (2)

- Bikini Body: Eating GuideDocument12 pagesBikini Body: Eating GuideAdela M BudNo ratings yet

- Security Information and Event Management (SIEM) - 2021Document4 pagesSecurity Information and Event Management (SIEM) - 2021HarumNo ratings yet

- Portales Etapas 2022 - MonicaDocument141 pagesPortales Etapas 2022 - Monicadenis_c341No ratings yet

- The Dallas Post 07-24-2011Document16 pagesThe Dallas Post 07-24-2011The Times LeaderNo ratings yet

- The Cornerstones of TestingDocument7 pagesThe Cornerstones of TestingOmar Khalid Shohag100% (3)

- Feminist Standpoint As Postmodern StrategyDocument21 pagesFeminist Standpoint As Postmodern StrategySumit AcharyaNo ratings yet

- Auditing The Purchasing Process: Mcgraw-Hill/IrwinDocument18 pagesAuditing The Purchasing Process: Mcgraw-Hill/IrwinFaruk H. IrmakNo ratings yet

- 100 Demon WeaponsDocument31 pages100 Demon WeaponsSpencer KrigbaumNo ratings yet

- SSoA Resilience Proceedings 27mbDocument704 pagesSSoA Resilience Proceedings 27mbdon_h_manzano100% (1)

- Literature Is An Important Component of A Total Language Arts Program at All Grade Levels Because of The Many Benefits It OffersDocument1 pageLiterature Is An Important Component of A Total Language Arts Program at All Grade Levels Because of The Many Benefits It Offersbersam05No ratings yet

- WHO SOPs Terms DefinitionsDocument3 pagesWHO SOPs Terms DefinitionsNaseem AkhtarNo ratings yet

- AWS PowerPoint PresentationDocument129 pagesAWS PowerPoint PresentationZack Abrahms56% (9)

- Specifications: Back2MaintableofcontentsDocument31 pagesSpecifications: Back2MaintableofcontentsRonal MoraNo ratings yet

- Condo Contract of SaleDocument7 pagesCondo Contract of SaleAngelo MadridNo ratings yet

- Math Grade 7 Q2 PDFDocument158 pagesMath Grade 7 Q2 PDFIloise Lou Valdez Barbado100% (2)

- Hse Check List For Portable Grinding MachineDocument1 pageHse Check List For Portable Grinding MachineMD AbdullahNo ratings yet

- Cat Enclosure IngDocument40 pagesCat Enclosure IngJuan Pablo GonzálezNo ratings yet

- Food Security: Its Components and ChallengesDocument9 pagesFood Security: Its Components and ChallengesSimlindile NgobelaNo ratings yet

- Serenity Dormitory PresentationDocument16 pagesSerenity Dormitory PresentationGojo SatoruNo ratings yet

- Burger 2005Document7 pagesBurger 2005Stefania PDNo ratings yet

- Timeline of Jewish HistoryDocument33 pagesTimeline of Jewish Historyfabrignani@yahoo.com100% (1)

- Cone Penetration Test (CPT) Interpretation: InputDocument5 pagesCone Penetration Test (CPT) Interpretation: Inputstephanie andriamanalinaNo ratings yet

- Part 1: Hôm nay bạn mặc gì?Document5 pagesPart 1: Hôm nay bạn mặc gì?NamNo ratings yet

- Peralta v. Philpost (GR 223395, December 4, 2018Document20 pagesPeralta v. Philpost (GR 223395, December 4, 2018Conacon ESNo ratings yet

- Chapter 4Document20 pagesChapter 4Alyssa Grace CamposNo ratings yet

- TWC AnswersDocument169 pagesTWC AnswersAmanda StraderNo ratings yet

- Project Presentation (142311004) FinalDocument60 pagesProject Presentation (142311004) FinalSaad AhammadNo ratings yet