You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The "Exorbitant Privilege" - A Theoretical ExpositionDocument25 pagesThe "Exorbitant Privilege" - A Theoretical ExpositionANIBAL LOPEZNo ratings yet

- CF Chapter Two QuestionsDocument2 pagesCF Chapter Two Questionszaraazahid_950888410No ratings yet

- Legal Notice (Prem Chand Jai Chand) Sec - 138Document3 pagesLegal Notice (Prem Chand Jai Chand) Sec - 138GADDi AhNo ratings yet

- Managerial Accounting ch10 QuizDocument7 pagesManagerial Accounting ch10 Quizariel4869No ratings yet

- 27 Fil EstateDocument1 page27 Fil EstateDonvidachiye Liwag CenaNo ratings yet

- Eml S4hana2020 Op Starters Guide v1.1Document34 pagesEml S4hana2020 Op Starters Guide v1.1herbertNo ratings yet

- Product Sheet FOR CALCULATING PROFIRDocument14 pagesProduct Sheet FOR CALCULATING PROFIRZain KhalidNo ratings yet

- Financial Literacy (Done)Document5 pagesFinancial Literacy (Done)Joseph Paul VERDANNo ratings yet

- Current Trends in Compensation & BenefitsDocument10 pagesCurrent Trends in Compensation & BenefitsGarcesto ConsultancyNo ratings yet

- KKR: Bertelsmann Acquires Full Ownership of Music Company BMGDocument6 pagesKKR: Bertelsmann Acquires Full Ownership of Music Company BMGAlyson DavisNo ratings yet

- Exam Review - Chapters 4, 5, 6: Key Terms and Concepts To KnowDocument21 pagesExam Review - Chapters 4, 5, 6: Key Terms and Concepts To KnowDanica De VeraNo ratings yet

- Business Plan: Maria Antonio Corn MillersDocument27 pagesBusiness Plan: Maria Antonio Corn MillersPelekani Sakala100% (1)

- JournalDocument6 pagesJournalAlyssa AlejandroNo ratings yet

- HPD - 0502 - Mills EscrowDocument16 pagesHPD - 0502 - Mills EscrowUlisesNo ratings yet

- Specimen & Key Points of The Chapter: Errors Causing Disagreement of Trial BalanceDocument10 pagesSpecimen & Key Points of The Chapter: Errors Causing Disagreement of Trial BalanceArham RajpootNo ratings yet

- Chapter 10 - Profitability AnalysisDocument46 pagesChapter 10 - Profitability AnalysisMega Nurjannah Ahmad100% (1)

- 23-Fwd: 1950's Paparazzi - Performer Contract & W-9Document2 pages23-Fwd: 1950's Paparazzi - Performer Contract & W-9Julio BarriereNo ratings yet

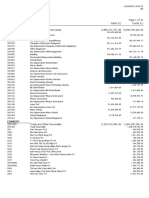

- Indofood Sukses Makmur TBK - Billingual - 30 - Sep - 2018 PDFDocument180 pagesIndofood Sukses Makmur TBK - Billingual - 30 - Sep - 2018 PDFSsela selviaNo ratings yet

- GL Opening BalanceDocument10 pagesGL Opening BalanceAye Mya ThidaNo ratings yet

- Macro Chap - 2Document15 pagesMacro Chap - 2NamaamNo ratings yet

- PitchBooks Guide To VC Funding For StartupsDocument25 pagesPitchBooks Guide To VC Funding For StartupsNazarii VykhrivskyiNo ratings yet

- RFP Supply of Hardware Maintenance of CBS PDFDocument142 pagesRFP Supply of Hardware Maintenance of CBS PDFAndy_sumanNo ratings yet

- Net Present Value (NPV)Document12 pagesNet Present Value (NPV)Rustam AliyevNo ratings yet

- How To Make A Business PlanDocument17 pagesHow To Make A Business PlanlibaboyNo ratings yet

- Instant Loans For Bad Credit-Instant Money For The Bad CreditorsDocument4 pagesInstant Loans For Bad Credit-Instant Money For The Bad CreditorsMcculloughNixon2No ratings yet

- Bollinger Band MagicDocument13 pagesBollinger Band MagicMike Ugo80% (5)

- Topic-Best Mutual Funds 2024Document5 pagesTopic-Best Mutual Funds 2024iamrdas02No ratings yet

- 5 Randomness and Probability PDFDocument33 pages5 Randomness and Probability PDFirisNo ratings yet

- KSD and Their Finances ArticleDocument2 pagesKSD and Their Finances ArticleKING 5 NewsNo ratings yet

- India Banks: EquitiesDocument42 pagesIndia Banks: EquitiesDebjit AdakNo ratings yet