You might also like

- AFM Notes by - Taha Popatia - Volume 1Document68 pagesAFM Notes by - Taha Popatia - Volume 1Ashfaq Ul Haq OniNo ratings yet

- Financial Management June 2011 Exam Paper ICAEWDocument6 pagesFinancial Management June 2011 Exam Paper ICAEWMuhammad Ziaul HaqueNo ratings yet

- Jim Sinclair On Gold and The World Financial SystemDocument8 pagesJim Sinclair On Gold and The World Financial SystemRon HeraNo ratings yet

- Aug Booking - Com ConfirmationDocument2 pagesAug Booking - Com ConfirmationViswanathNo ratings yet

- ISAS Brief: Capital Account Convertibility For India - Current ConcernsDocument5 pagesISAS Brief: Capital Account Convertibility For India - Current Concernsapi-26494462No ratings yet

- Fema PDFDocument10 pagesFema PDFshivam_dubey4004No ratings yet

- Global LinkagesDocument36 pagesGlobal Linkagesraashid91No ratings yet

- Fdi and Exchange Rate RelationsDocument17 pagesFdi and Exchange Rate Relationsuk4950430No ratings yet

- Dre Been: What Are Type of Facili. Es Offered by Housing Finance Companies. What Are Some ofDocument10 pagesDre Been: What Are Type of Facili. Es Offered by Housing Finance Companies. What Are Some oframdayal kumawatNo ratings yet

- INR InternationalisationDocument3 pagesINR InternationalisationBarsha ToppoNo ratings yet

- RBI Intervention in Foreign Exchange MarketDocument26 pagesRBI Intervention in Foreign Exchange Marketshamchandak03100% (1)

- Exchange Rate System in IndiaDocument8 pagesExchange Rate System in IndiaVandana SharmaNo ratings yet

- Forex Exchange Reserves WordDocument14 pagesForex Exchange Reserves WordHamid RehmanNo ratings yet

- Fera To FemaDocument53 pagesFera To FemaJay BarchhaNo ratings yet

- Current and Capital Account Convertibility-The Balance of PaymentsDocument5 pagesCurrent and Capital Account Convertibility-The Balance of Paymentssudhasagar0055No ratings yet

- Financial Management A Report Submitted For External Assessment On Project Topic: Forex Risk ManagementDocument32 pagesFinancial Management A Report Submitted For External Assessment On Project Topic: Forex Risk Managementishmeetkohli100% (1)

- India'S Policy Stance On Reserves and The Currency: Working Paper No. 108Document33 pagesIndia'S Policy Stance On Reserves and The Currency: Working Paper No. 108Rishi AmritNo ratings yet

- PatnaikPauly2001 IndianforexDocument28 pagesPatnaikPauly2001 IndianforexSubham ChoudhuryNo ratings yet

- PatnaikPauly2001 IndianforexDocument28 pagesPatnaikPauly2001 IndianforexJustin ThomasNo ratings yet

- SR24329232545Document12 pagesSR24329232545pradeep kumarNo ratings yet

- Bibliometric Survey of Foreign Exchange ReservesDocument17 pagesBibliometric Survey of Foreign Exchange Reservesshubham aroraNo ratings yet

- Development Research Group Studies 2013 - 14: Securities and Exchange Board of IndiaDocument100 pagesDevelopment Research Group Studies 2013 - 14: Securities and Exchange Board of IndiaVaibhav SalaskarNo ratings yet

- Forex Reserves IndiaDocument27 pagesForex Reserves IndiaDhaval Lagwankar100% (2)

- What Is Currency ConvertibilityDocument8 pagesWhat Is Currency Convertibilitybrahmesh_raoNo ratings yet

- Captal Acc ConvertibilityDocument42 pagesCaptal Acc ConvertibilityAbhijeet BhattacharyaNo ratings yet

- Saim 1Document29 pagesSaim 1Sammy PatelNo ratings yet

- Current and Capital Account Convert Ability - FMKTDocument3 pagesCurrent and Capital Account Convert Ability - FMKTDdev ThaparrNo ratings yet

- Investing in IndiaDocument5 pagesInvesting in IndiaAlok VermaNo ratings yet

- Research Paper - Financial Sector ReformsDocument10 pagesResearch Paper - Financial Sector ReformsTarun KehairNo ratings yet

- Capital Account Convertibilty: By: Preeti N (766) Sumit H (803) Vinay NDocument13 pagesCapital Account Convertibilty: By: Preeti N (766) Sumit H (803) Vinay NVinay NaikNo ratings yet

- Indian Stock MarketDocument23 pagesIndian Stock MarketPawan GajbhiyeNo ratings yet

- Role of Reserve Bank of IndiaDocument16 pagesRole of Reserve Bank of Indianiyati_parthNo ratings yet

- MAEC - Project Report - Group PDocument21 pagesMAEC - Project Report - Group PSudip KarNo ratings yet

- Benchmark Rate IndiaDocument10 pagesBenchmark Rate IndiasaudebNo ratings yet

- Libralization Its Impact On Indian Banking SectorDocument7 pagesLibralization Its Impact On Indian Banking SectorSimran GopalNo ratings yet

- Rohith U J - AssignmentDocument3 pagesRohith U J - AssignmentRohithNo ratings yet

- A Thesis On A Study To Guide Investors in Online & Offline Trading in Equity MarketDocument36 pagesA Thesis On A Study To Guide Investors in Online & Offline Trading in Equity Marketsantosh kumar mauryaNo ratings yet

- Convertibility of Rupee.: Rohan Jivan Ghalsasi Mohima Sethi Rajeev RanjanDocument12 pagesConvertibility of Rupee.: Rohan Jivan Ghalsasi Mohima Sethi Rajeev RanjanRajeev Ranjan KumarNo ratings yet

- Development of Securities Market - The Indian Experience: Narendra JadhavDocument22 pagesDevelopment of Securities Market - The Indian Experience: Narendra JadhavAlishaNo ratings yet

- Financial Markets Integration in India: Asia-Pacific Development Journal Vol. 12, No. 2, December 2005Document18 pagesFinancial Markets Integration in India: Asia-Pacific Development Journal Vol. 12, No. 2, December 2005anon-392261No ratings yet

- Current Status of Derivative Products in India: An OverviewDocument17 pagesCurrent Status of Derivative Products in India: An OverviewSarojKumarSinghNo ratings yet

- Capital Account Convertibility - A Way Ahead For India: Project Report OnDocument12 pagesCapital Account Convertibility - A Way Ahead For India: Project Report OnKeta KurkuteNo ratings yet

- Impact of Sinking Rupee On Indias Foreign Trade (Threats To Exchange Rate Fluctuations)Document8 pagesImpact of Sinking Rupee On Indias Foreign Trade (Threats To Exchange Rate Fluctuations)IJAR JOURNALNo ratings yet

- International Reserves Determinants andDocument6 pagesInternational Reserves Determinants andJuan Nicolas SalgadoNo ratings yet

- Financial Stability Asurveyof Indian ExperienceDocument36 pagesFinancial Stability Asurveyof Indian ExperienceRakesh BetiwarNo ratings yet

- Indian Mutual FundDocument28 pagesIndian Mutual Fundap36r7961No ratings yet

- 6th Week Lecture Notes .B A Hon Economics VIth Semeter Money and Financial MarketsDocument10 pages6th Week Lecture Notes .B A Hon Economics VIth Semeter Money and Financial MarketsBen WelshelyNo ratings yet

- Reserve Bank of IndiaDocument29 pagesReserve Bank of IndiarachanarajeNo ratings yet

- N.L.S I.U: Rbi As The Custodian of Foreign ExchangeDocument13 pagesN.L.S I.U: Rbi As The Custodian of Foreign Exchangevishnu TiwariNo ratings yet

- BFA 243 NotesDocument54 pagesBFA 243 Notesshivtejkumbhar2121No ratings yet

- Organisational Structure and Role of RBI in Foreign Exchange MarketsDocument110 pagesOrganisational Structure and Role of RBI in Foreign Exchange Marketsmanoj_pker0% (1)

- Assignment OF Financial Institution and Services ON Mutual FundsDocument7 pagesAssignment OF Financial Institution and Services ON Mutual Fundssham_singhNo ratings yet

- Regulatory Bodies in India - RBI - 2Document38 pagesRegulatory Bodies in India - RBI - 2omesh gehlotNo ratings yet

- RBI Bulletin - Mar 2022Document160 pagesRBI Bulletin - Mar 2022Sowmya NarayananNo ratings yet

- Monetary Policy ImplementationDocument12 pagesMonetary Policy ImplementationYuseer AmanNo ratings yet

- Impact of FiisDocument3 pagesImpact of Fiisfinance24No ratings yet

- Reliance Money Project ReportDocument107 pagesReliance Money Project ReportSahil100% (3)

- Exchange Rate RegimesDocument17 pagesExchange Rate Regimesnimmy celin mariyaNo ratings yet

- Introduction To Indian Economy FinalDocument51 pagesIntroduction To Indian Economy FinalSabah MemonNo ratings yet

- FIIs in India.........Document12 pagesFIIs in India.........JogenderNo ratings yet

- IKUFP ComparisonDocument26 pagesIKUFP ComparisonAyush GuptaNo ratings yet

- Asian Development Review: Volume 29, Number 2, 2012From EverandAsian Development Review: Volume 29, Number 2, 2012No ratings yet

- Next Steps for ASEAN+3 Central Securities Depository and Real-Time Gross Settlement Linkages: A Progress Report of the Cross-Border Settlement Infrastructure ForumFrom EverandNext Steps for ASEAN+3 Central Securities Depository and Real-Time Gross Settlement Linkages: A Progress Report of the Cross-Border Settlement Infrastructure ForumNo ratings yet

- WEight Training ScheduleDocument2 pagesWEight Training Scheduleapi-3712367100% (1)

- Anti-Inflationary Policy in IndiaDocument14 pagesAnti-Inflationary Policy in Indiaapi-3712367No ratings yet

- Policybrief Nov05Document6 pagesPolicybrief Nov05api-3712367No ratings yet

- Report OnDocument9 pagesReport Onapi-3712367No ratings yet

- Macroeconomics AssignmentsDocument15 pagesMacroeconomics Assignmentsapi-3712367No ratings yet

- Fema CDocument5 pagesFema Capi-3712367No ratings yet

- SubPrime Mortgage MarketDocument6 pagesSubPrime Mortgage Marketapi-3712367No ratings yet

- FFRChange HistoryDocument1 pageFFRChange Historyapi-3712367No ratings yet

- Subprime Toxic Debt - Bloomberg July07Document10 pagesSubprime Toxic Debt - Bloomberg July07api-3712367No ratings yet

- Global Economics - IndiaDocument2 pagesGlobal Economics - Indiaapi-3712367No ratings yet

- Sebi TocDocument33 pagesSebi Tocapi-3712367No ratings yet

- BSC & Knowledge ManagementDocument3 pagesBSC & Knowledge Managementapi-3712367100% (1)

- Subprime FinalDocument34 pagesSubprime Finalapi-3712367No ratings yet

- SubprimeDocument31 pagesSubprimeapi-3712367No ratings yet

- MacroEconomics - Lecture 4 SKM MultiplierDocument7 pagesMacroEconomics - Lecture 4 SKM Multiplierapi-3712367No ratings yet

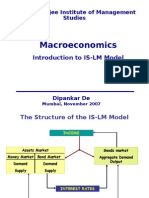

- MacroEconomics - Lecture 4 - IsLM ModelDocument24 pagesMacroEconomics - Lecture 4 - IsLM Modelapi-3712367No ratings yet

- Balanced ScorecardDocument13 pagesBalanced Scorecardapi-3712367No ratings yet

- Amortization Calculator - Wikipedia, The Free EncyclopediaDocument3 pagesAmortization Calculator - Wikipedia, The Free Encyclopediaapi-3712367No ratings yet

- Balanced ScorecardDocument67 pagesBalanced Scorecardapi-3712367100% (4)

- MacroEconomics - Lecture 5 Introduction To ISLMDocument21 pagesMacroEconomics - Lecture 5 Introduction To ISLMapi-3712367100% (1)

- Micro Economics PresentationDocument18 pagesMicro Economics Presentationapi-3712367No ratings yet

- Multinational Business Finance 12th Edition Slides Chapter 13Document31 pagesMultinational Business Finance 12th Edition Slides Chapter 13Alli Tobba100% (1)

- Akuntansi Keuangan Lanjutan - Chap 011Document38 pagesAkuntansi Keuangan Lanjutan - Chap 011Gugat jelang romadhonNo ratings yet

- Exchange Rate ManagementDocument19 pagesExchange Rate ManagementRohit JangidNo ratings yet

- International Financial Management Eun 7th Edition Test BankDocument17 pagesInternational Financial Management Eun 7th Edition Test BankCynthiaWalkerfeqb100% (34)

- Unit-Ii: Foreign Exchange Regulations and FormalitiesDocument27 pagesUnit-Ii: Foreign Exchange Regulations and FormalitiesLAKSHMIKANTH.B MEC-AP/MCNo ratings yet

- Indian Economy 3 LPGDocument68 pagesIndian Economy 3 LPGAlans TechnicalNo ratings yet

- 7.Ch 11 - International Finance New SyllabusDocument85 pages7.Ch 11 - International Finance New SyllabusSullivan LyaNo ratings yet

- ImfDocument30 pagesImfvigneshkarthik23No ratings yet

- Ch01 VersCDocument47 pagesCh01 VersCBren FlakesNo ratings yet

- Asian Regionalism-Group 2Document20 pagesAsian Regionalism-Group 2Fia bianca ColibaoNo ratings yet

- FINM009 - Assignment 1Document22 pagesFINM009 - Assignment 1Meena Das100% (1)

- SFM Super 30 TheoryDocument37 pagesSFM Super 30 TheorySahil SharmaNo ratings yet

- Chap 3Document29 pagesChap 3kimngan.nguyen8803No ratings yet

- IA Portfoliob enDocument18 pagesIA Portfoliob enOscar E. SánchezNo ratings yet

- Journal of International Money and Finance: Juan Carlos Berganza, Carmen BrotoDocument17 pagesJournal of International Money and Finance: Juan Carlos Berganza, Carmen BrotoKhairulNo ratings yet

- Corporate Finance QuizDocument6 pagesCorporate Finance QuizHerdanto UtamaNo ratings yet

- Yearly Plan Economics GR 11Document4 pagesYearly Plan Economics GR 11NancyNabaAbouFarajNo ratings yet

- Problemens On Foreign Exchange MarketDocument3 pagesProblemens On Foreign Exchange MarketTeffi Boyer MontoyaNo ratings yet

- Forecasting Daily and Monthly Exchange Rates With Machine Learning TechniquesDocument32 pagesForecasting Daily and Monthly Exchange Rates With Machine Learning TechniquesOsiayaNo ratings yet

- McKinsey 2012Document10 pagesMcKinsey 2012LuxembourgAtaGlanceNo ratings yet

- Monetary Policy RefernceDocument17 pagesMonetary Policy RefernceMaria Cristina ImportanteNo ratings yet

- AgreementDocument28 pagesAgreementEugénio AmaralNo ratings yet

- The Monetary Approach To The BoP 1Document30 pagesThe Monetary Approach To The BoP 1Velichka DimitrovaNo ratings yet

- Fundamentals of Multinational FinanceDocument40 pagesFundamentals of Multinational FinanceMaría RamosNo ratings yet

- Eco P2-9708 Guess For May 2023Document4 pagesEco P2-9708 Guess For May 2023Mishal ZainabNo ratings yet

- bài tập tổng hợp ônDocument16 pagesbài tập tổng hợp ônHà NguyễnNo ratings yet