You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

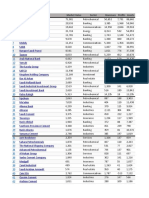

- Top 100 Saudi CompaniesDocument12 pagesTop 100 Saudi CompaniesMurad Al AliatNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- IOE516 - Stochastic Processes II Homework Set 2 - Suggested SolutionsDocument6 pagesIOE516 - Stochastic Processes II Homework Set 2 - Suggested SolutionsAloke ChatterjeeNo ratings yet

- Complex EigenvaluesDocument7 pagesComplex EigenvaluesAloke ChatterjeeNo ratings yet

- FubiniDocument5 pagesFubiniAloke ChatterjeeNo ratings yet

- Stochastic Optimization: Anton J. Kleywegt and Alexander ShapiroDocument43 pagesStochastic Optimization: Anton J. Kleywegt and Alexander ShapiroAloke ChatterjeeNo ratings yet

- Syllabus INE1050 Microeconomics 2023Document5 pagesSyllabus INE1050 Microeconomics 2023Phuonganh NgoNo ratings yet

- Pakistan's Relations With North African Countries: Challenges and Way ForwardDocument10 pagesPakistan's Relations With North African Countries: Challenges and Way ForwardInstitute of Policy StudiesNo ratings yet

- Agreement Between Japan and The Republic of IndonesiaDocument36 pagesAgreement Between Japan and The Republic of IndonesiaerfikaNo ratings yet

- OTIS - Case - EditedDocument10 pagesOTIS - Case - EditedAshley WoodNo ratings yet

- Diageo Phils. Inc. vs. CIR GR No. 183553Document3 pagesDiageo Phils. Inc. vs. CIR GR No. 183553ZeusKimNo ratings yet

- Virtonomics q4 ReportDocument22 pagesVirtonomics q4 Reportapi-504872356No ratings yet

- Securities and Exchange Commission (SEC) - Formx-17a-5 2fDocument9 pagesSecurities and Exchange Commission (SEC) - Formx-17a-5 2fhighfinanceNo ratings yet

- Knupp For Mayor: For Instructions, See Back of Form LDocument1 pageKnupp For Mayor: For Instructions, See Back of Form LZach EdwardsNo ratings yet

- A1D - Rework Production Order WIP in Process - BBPDocument17 pagesA1D - Rework Production Order WIP in Process - BBPGRMUDIMELA REDDYNo ratings yet

- How To Load Amore Prepaid Card - Google SearchDocument1 pageHow To Load Amore Prepaid Card - Google SearchDanny MontanaNo ratings yet

- PR - Interim Order Cum Show Cause Notice Against Shri Priyansh Patodi, Proprietor - MMF SolutionsDocument1 pagePR - Interim Order Cum Show Cause Notice Against Shri Priyansh Patodi, Proprietor - MMF SolutionsShyam SunderNo ratings yet

- Ail Setup AdxDocument5 pagesAil Setup Adxharish20050% (1)

- Forward Rate AgreementsDocument2 pagesForward Rate Agreementsajain22No ratings yet

- Sample Marketing ResearchDocument11 pagesSample Marketing ResearchChristina Amor GarciaNo ratings yet

- Psicologia - Mario Ferreira Dos SantosDocument144 pagesPsicologia - Mario Ferreira Dos Santosmusic the in vein contentetv jogagêmosNo ratings yet

- Dr. Harisingh Gour Vishwavidyalaya, Sagar (M.P.) : Fee Breakup AmountDocument1 pageDr. Harisingh Gour Vishwavidyalaya, Sagar (M.P.) : Fee Breakup AmountAditi sainiNo ratings yet

- PCMC Receipt 1Document1 pagePCMC Receipt 1Manoj SinghNo ratings yet

- Money and Monetary StandardsDocument40 pagesMoney and Monetary StandardsZenedel De JesusNo ratings yet

- Held Captive: Child Poverty in AmericaDocument56 pagesHeld Captive: Child Poverty in AmericaProgressTXNo ratings yet

- Book Ii Property, Ownership and Its ModificationsDocument7 pagesBook Ii Property, Ownership and Its Modificationslilieth shayNo ratings yet

- Group 7 SecB MahindraDocument8 pagesGroup 7 SecB MahindrasaranshmaniNo ratings yet

- FX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HigherDocument25 pagesFX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HighertekesburNo ratings yet

- The World Is Flat: "The Great Sorting Out" Through "The Virgin of Guadalupe"Document34 pagesThe World Is Flat: "The Great Sorting Out" Through "The Virgin of Guadalupe"Edward Nicklaus MalekNo ratings yet

- MarchDocument70 pagesMarchdexter1850No ratings yet

- Jack Kelly Presentation On Jersey City's BudgetDocument12 pagesJack Kelly Presentation On Jersey City's BudgetThe Jersey City IndependentNo ratings yet

- Economic Building Blocks For VictoriaDocument16 pagesEconomic Building Blocks For VictoriaDaniel AndrewsNo ratings yet

- Pariksha Pe Charcha Nidhi PDFDocument3 pagesPariksha Pe Charcha Nidhi PDFPiyusha MhaiskeyNo ratings yet

- Annex 37-Annual Statement of Receipts and PaymentsDocument4 pagesAnnex 37-Annual Statement of Receipts and Paymentsvermon salidoNo ratings yet

- Immigration NA HandbookDocument18 pagesImmigration NA Handbookdeepanbaalan5112No ratings yet