You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Case Study Final RoundDocument2 pagesCase Study Final RoundPawan NkNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Project TopicsDocument13 pagesProject TopicsPawan NkNo ratings yet

- Admission CircularDocument2 pagesAdmission CircularPawan NkNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Project TopicsDocument13 pagesProject TopicsPawan NkNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- BROM (Sim)Document2 pagesBROM (Sim)Pawan NkNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Tata Steel LTDDocument15 pagesTata Steel LTDPawan NkNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Syllabus Copy of 2nd SemesterDocument21 pagesSyllabus Copy of 2nd SemesterPawan NkNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Who Moved My JobDocument19 pagesWho Moved My JobPawan NkNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Case Study Final RoundDocument2 pagesCase Study Final RoundPawan NkNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Paint IndustryDocument6 pagesPaint IndustryPawan NkNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Business, Government & Society: Pawan Kumar N K 12301005Document8 pagesBusiness, Government & Society: Pawan Kumar N K 12301005Pawan NkNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Nokia PC Suite UG EngDocument28 pagesNokia PC Suite UG Engshelly_nataliaNo ratings yet

- Talent ManagementDocument26 pagesTalent ManagementPawan NkNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Case Study Final RoundDocument2 pagesCase Study Final RoundPawan NkNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Vapour Compression Refrigeration Test RigDocument1 pageVapour Compression Refrigeration Test RigPawan NkNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Alpha College of EngineeringDocument1 pageAlpha College of EngineeringPawan NkNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- 1.1 Underwater Welding OverviewDocument1 page1.1 Underwater Welding OverviewPawan NkNo ratings yet

- Adaptive Cruise ControlDocument1 pageAdaptive Cruise ControlPawan NkNo ratings yet

- R Reessuum Mee F Foorrm Maatt && C Coonntteenntt: Carol TecherDocument9 pagesR Reessuum Mee F Foorrm Maatt && C Coonntteenntt: Carol Techerhiteshtanwer13No ratings yet

- 371 - Umoja Bank Reconciliation - User Guide - v1.0 PDFDocument86 pages371 - Umoja Bank Reconciliation - User Guide - v1.0 PDFsreekumarNo ratings yet

- Create Accounting 290816Document9 pagesCreate Accounting 290816SAlah MOhammedNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Visa Rules PublicDocument1,031 pagesVisa Rules PublicGabriel Alexandru LipanNo ratings yet

- BFSI Business Analysis ProfessionalDocument6 pagesBFSI Business Analysis ProfessionalaNo ratings yet

- Aunpp BrochureDocument4 pagesAunpp BrochureUser ShareNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Bank of BarodaDocument81 pagesBank of BarodalovelydineshNo ratings yet

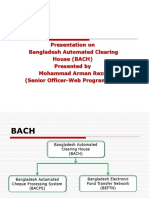

- BACH Complete PresentationDocument57 pagesBACH Complete Presentationsdfdsf0% (1)

- CASH MANAGEMENT ANALYSIS RPP FINAL As of Dec 7 2021Document30 pagesCASH MANAGEMENT ANALYSIS RPP FINAL As of Dec 7 2021Amnie AliNo ratings yet

- CHEQUE TRUNCATION - Business OpportunitiesDocument28 pagesCHEQUE TRUNCATION - Business OpportunitiesMangesh KolwadkarNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- An Internship Report On Risk Management of Exim Bank BangladeshDocument64 pagesAn Internship Report On Risk Management of Exim Bank BangladeshSumantra Barai25% (4)

- 9 Analytics FramworksDocument5 pages9 Analytics FramworksmittleNo ratings yet

- Capital MarketDocument10 pagesCapital Marketसम्राट सुबेदीNo ratings yet

- Krishna HSBC 20-21 StatementDocument175 pagesKrishna HSBC 20-21 StatementSumit VermaNo ratings yet

- Black BookDocument104 pagesBlack BookSoni PalNo ratings yet

- A Study On Technical Analysis S&P NIFTY StocksDocument87 pagesA Study On Technical Analysis S&P NIFTY StocksManikanta Satish0% (1)

- Clearing Bank ChequesDocument4 pagesClearing Bank ChequesLaila HammadNo ratings yet

- Account StatementDocument10 pagesAccount StatementShiv JoshiNo ratings yet

- BIS QTRT 202003Document151 pagesBIS QTRT 202003sh_chandraNo ratings yet

- Clearing House Lectureupdated - June11 2013Document35 pagesClearing House Lectureupdated - June11 2013dushakilNo ratings yet

- Payment, Clearing and Settlement Systems in Korea: CPSS - Red Book - 2011Document40 pagesPayment, Clearing and Settlement Systems in Korea: CPSS - Red Book - 2011Xinjie ChuNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Fia Fa1 Banking Monies ReceivedDocument22 pagesFia Fa1 Banking Monies ReceivedKj NayeeNo ratings yet

- Settlement Manual: 21 July 2020Document293 pagesSettlement Manual: 21 July 2020Ahmed Alobaede0% (1)

- Commerce 1 PDFDocument14 pagesCommerce 1 PDFAnonymous AOS81PvLeiNo ratings yet

- Ns 01 2013 PDFDocument136 pagesNs 01 2013 PDFchunochunoNo ratings yet

- 2023 03 21 14 30 06apr 22 - 400070Document7 pages2023 03 21 14 30 06apr 22 - 400070Sakila SNo ratings yet

- FTDocument337 pagesFTMadjid MansouriNo ratings yet

- Clearing House Interbank Payment SystemDocument4 pagesClearing House Interbank Payment SystemEjaru SagarNo ratings yet

- Philippine Depository and Trust CorpDocument59 pagesPhilippine Depository and Trust CorpMonica Medina100% (1)

- Franklin Transaction FormDocument4 pagesFranklin Transaction FormGurvinder SinghNo ratings yet

- Cashpro® Online: Technical Resources: Bank Administration Institute CodesDocument7 pagesCashpro® Online: Technical Resources: Bank Administration Institute CodesAnilNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)