You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- JFSP Bernard MeasuringtheValueofaGLWB 032010Document6 pagesJFSP Bernard MeasuringtheValueofaGLWB 032010sammysmithaztNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Us 20060073976Document31 pagesUs 20060073976kloppigNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- 2012 JP Morgan Whistle Blower 3-14-2012Document6 pages2012 JP Morgan Whistle Blower 3-14-2012sammysmithaztNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Weapon Disposal at Sea Ic - Munitions - Seabed - RepDocument90 pagesWeapon Disposal at Sea Ic - Munitions - Seabed - RepsammysmithaztNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Wire Woven EarringsDocument3 pagesWire Woven EarringssammysmithaztNo ratings yet

- Basic Blacksmithing - David Harries PDFDocument132 pagesBasic Blacksmithing - David Harries PDFMichele Perrone FilhoNo ratings yet

- Steele v. United States of America - Document No. 70Document23 pagesSteele v. United States of America - Document No. 70Justia.com0% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Financial - DictionaryDocument242 pagesFinancial - DictionarySreni VasanNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- 403SavingPlans PDFDocument20 pages403SavingPlans PDFEscalation ACN WhirlpoolNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

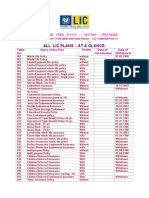

- All LIC PlansDocument4 pagesAll LIC Planslicvivek100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- 288 Comparative Study in Life Insurance Sector For Kotak MahindraDocument87 pages288 Comparative Study in Life Insurance Sector For Kotak MahindraKaran LuthraNo ratings yet

- Annexure To Income Tax CircularDocument6 pagesAnnexure To Income Tax CircularDipti BhanjaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- From Here To There: A Clear View of Retirement For Women - Webinar by Gemma JablonskiDocument41 pagesFrom Here To There: A Clear View of Retirement For Women - Webinar by Gemma JablonskiLNP MEDIA GROUP, Inc.No ratings yet

- Time Value of Money (Problems)Document4 pagesTime Value of Money (Problems)Mohammad RashidNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Bank of EnglandDocument39 pagesBank of EnglandNguyen Ha QuanNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- 4Document445 pages4lilylikesturtle75% (4)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- VantageDocument16 pagesVantageDie001No ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- FrontLines Magazine Fall 2013Document16 pagesFrontLines Magazine Fall 2013Human Life InternationalNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Retirement Planning ChecklistDocument3 pagesRetirement Planning ChecklistbvbenhamNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Retirement Budget WorksheetDocument2 pagesRetirement Budget WorksheetBella MelendresNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- SAPM by Syam Kerala University s3 MbaDocument88 pagesSAPM by Syam Kerala University s3 Mbasyam kumar sNo ratings yet

- What's More: Quarter 2 - Module 7: Deferred AnnuityDocument4 pagesWhat's More: Quarter 2 - Module 7: Deferred AnnuityChelsea NicoleNo ratings yet

- AXA Reference Document 2015Document424 pagesAXA Reference Document 2015Timothy RvansNo ratings yet

- Metlife Case StudyDocument2 pagesMetlife Case StudyheyNo ratings yet

- Week 13-14: Chapter 9: Investing For The Future: Growing Your Financial ResourcesDocument36 pagesWeek 13-14: Chapter 9: Investing For The Future: Growing Your Financial ResourcesGiselle Bronda CastañedaNo ratings yet

- ADIB YAZID - Contoh Soalan PCEIA SET B (Bahasa Inggeris)Document35 pagesADIB YAZID - Contoh Soalan PCEIA SET B (Bahasa Inggeris)carollim1008100% (1)

- LiveWell MF IRA Brochure PDFDocument12 pagesLiveWell MF IRA Brochure PDFAmy Nga LeNo ratings yet

- Carpenters Annuity Fund 2006Document20 pagesCarpenters Annuity Fund 2006Latisha WalkerNo ratings yet

- Series 7 Qualification Exam: General Securities Representative Study Manual - 42nd EditionDocument499 pagesSeries 7 Qualification Exam: General Securities Representative Study Manual - 42nd EditionGiovanni100% (5)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Bancassurance v. Insurance BrokersDocument23 pagesBancassurance v. Insurance BrokersKhizar Jamal Siddiqui100% (2)

- CFA Level III 2010 Exam AnswersDocument67 pagesCFA Level III 2010 Exam AnswersAkash KumarNo ratings yet

- Insurance Basic QuestionDocument152 pagesInsurance Basic QuestionKrupa VoraNo ratings yet

- Concise Encyclopedia of InvestingDocument103 pagesConcise Encyclopedia of InvestingMohammad Hamdan Abo AdnanNo ratings yet

- John Hancock Mut. Life Ins. Co. v. Harris Trust and Sav. Bank, 510 U.S. 86 (1993)Document30 pagesJohn Hancock Mut. Life Ins. Co. v. Harris Trust and Sav. Bank, 510 U.S. 86 (1993)Scribd Government DocsNo ratings yet

- Running Head: The Insurance Industry in The Cayman Islands 1Document26 pagesRunning Head: The Insurance Industry in The Cayman Islands 1api-331051038No ratings yet

- Key Insurance Terms - Clements Worldwide - Expat Insurance SpecialistDocument12 pagesKey Insurance Terms - Clements Worldwide - Expat Insurance Specialist91651sgd54sNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)