You might also like

- Presented by Group 18: Neha Srivastava Sneha Shivam Garg TarunaDocument41 pagesPresented by Group 18: Neha Srivastava Sneha Shivam Garg TarunaNeha SrivastavaNo ratings yet

- Electrolight - New Product LaunchDocument4 pagesElectrolight - New Product LaunchNeha SrivastavaNo ratings yet

- 7 CoagulationDocument103 pages7 CoagulationAkulSenapatiNo ratings yet

- CitibankDocument1 pageCitibankNeha SrivastavaNo ratings yet

- Dogfight RyanairDocument4 pagesDogfight RyanairKiran Banshiwal60% (5)

- How Did Lisa Get Into The Current Mess? Compare It With Her Behaviour in Other Company?Document1 pageHow Did Lisa Get Into The Current Mess? Compare It With Her Behaviour in Other Company?Neha SrivastavaNo ratings yet

- Presentation Industrial AwarenessDocument5 pagesPresentation Industrial AwarenessNeha SrivastavaNo ratings yet

- PP Form OnlineDocument1 pagePP Form OnlineNeha SrivastavaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 1 Introduction To BankingDocument8 pages1 Introduction To BankingGurnihalNo ratings yet

- Country Wide Litigation Database 01072007Document15 pagesCountry Wide Litigation Database 01072007Carrieonic100% (1)

- Swiss Challenge Method by Govt of Madhya Pradesh - SCM11022013FinalDocument46 pagesSwiss Challenge Method by Govt of Madhya Pradesh - SCM11022013FinalkpindiaNo ratings yet

- Document No 76 - Debt Fund Update Jan' 23Document3 pagesDocument No 76 - Debt Fund Update Jan' 23AmrutaNo ratings yet

- List of Groups and Topic For Practical Assignment 1Document5 pagesList of Groups and Topic For Practical Assignment 1pareek gopalNo ratings yet

- Meta Reports Fourth Quarter and Full Year 2022 Results 2023Document12 pagesMeta Reports Fourth Quarter and Full Year 2022 Results 2023Fady EhabNo ratings yet

- CLS Gathers Momentum, Rao, CCILDocument6 pagesCLS Gathers Momentum, Rao, CCILShrishailamalikarjunNo ratings yet

- Solved Rollo and Andrea Are Equal Owners of Gosney Company DuringDocument1 pageSolved Rollo and Andrea Are Equal Owners of Gosney Company DuringAnbu jaromiaNo ratings yet

- Combined Pdfs Katarina BookDocument6 pagesCombined Pdfs Katarina Bookapi-300353710No ratings yet

- Money-Time Relationships: PrinciplesDocument32 pagesMoney-Time Relationships: Principlesimran_chaudhryNo ratings yet

- SIMPLE and COMPOUND INTEREST 11Document69 pagesSIMPLE and COMPOUND INTEREST 11Jay QuinesNo ratings yet

- Chapter 2 Cost Concepts and The Cost Accounting Information SystemDocument44 pagesChapter 2 Cost Concepts and The Cost Accounting Information Systemelite76No ratings yet

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVara Prasad AvulaNo ratings yet

- Certificate in Bookkeeping and Accounting Level 2Document38 pagesCertificate in Bookkeeping and Accounting Level 2McKay TheinNo ratings yet

- Assignment - 2: Semester Spring 2021Document3 pagesAssignment - 2: Semester Spring 2021Amina HamidNo ratings yet

- NEW DT Bullet (MCQ'S) by CA Saumil Manglani - CS Exec June 22 & Dec 22 ExamsDocument168 pagesNEW DT Bullet (MCQ'S) by CA Saumil Manglani - CS Exec June 22 & Dec 22 ExamsAkash MalikNo ratings yet

- Financial Report (October 2017)Document2 pagesFinancial Report (October 2017)Marija DukićNo ratings yet

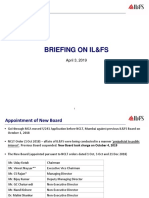

- ILFS Briefing (April 2019)Document15 pagesILFS Briefing (April 2019)Richard DierdreNo ratings yet

- Partnership Deed Bareilly Gorakhpur Liquor CompanyDocument8 pagesPartnership Deed Bareilly Gorakhpur Liquor CompanyDeepkamal JaiswalNo ratings yet

- Maria Hernandez and AssociatesDocument9 pagesMaria Hernandez and Associatesvineet383No ratings yet

- Effects of A High CAD EssayDocument2 pagesEffects of A High CAD EssayfahoutNo ratings yet

- Central Bank-Monetary Policy ReviewDocument6 pagesCentral Bank-Monetary Policy ReviewAda DeranaNo ratings yet

- Valuation of Bonds and SharesDocument39 pagesValuation of Bonds and Shareskunalacharya5No ratings yet

- LMOR Session 123BLK1Document85 pagesLMOR Session 123BLK1Seera HarisNo ratings yet

- MBA (E) 2021-23, 3rd Semester All Subjects SyllabusDocument40 pagesMBA (E) 2021-23, 3rd Semester All Subjects SyllabusANISHA DUTTANo ratings yet

- Mayuga Vs MetroDocument4 pagesMayuga Vs MetroPaulitoPunongbayanNo ratings yet

- Liska PaystubDocument1 pageLiska PaystubCreative Puppy100% (1)

- Galgotias University Vishwajeet Singh S/O Kuldeep SinghDocument1 pageGalgotias University Vishwajeet Singh S/O Kuldeep SinghAashika SinghNo ratings yet

- Akuntansi 11Document3 pagesAkuntansi 11Zhida PratamaNo ratings yet

- Chapter 4 Accounts Receivable Learning Objectives: Receivables."Document4 pagesChapter 4 Accounts Receivable Learning Objectives: Receivables."Misiah Paradillo JangaoNo ratings yet