You might also like

- Solution Manual For Managerial Economics 6th Edition Paul KeatDocument3 pagesSolution Manual For Managerial Economics 6th Edition Paul Keatalifertekin45% (11)

- Titan EyePlus Frame InvoiceDocument2 pagesTitan EyePlus Frame InvoiceBharatSubramonyNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- Tactical Financing DecisionsDocument24 pagesTactical Financing DecisionsAccounting TeamNo ratings yet

- Homework Questions For Tutorial in Week 7 With SolutionDocument12 pagesHomework Questions For Tutorial in Week 7 With SolutionrickNo ratings yet

- National Fabricators 1Document8 pagesNational Fabricators 1Sam Addi33% (3)

- Goldman SachsDocument15 pagesGoldman Sachs9986212378No ratings yet

- Acknowledgement of DebtDocument2 pagesAcknowledgement of DebttaskforcestfNo ratings yet

- ALK CHP 11 - GROUP 5 - (Ovilia, George, Rukmayanti, Laurensia, Fedryansyah)Document6 pagesALK CHP 11 - GROUP 5 - (Ovilia, George, Rukmayanti, Laurensia, Fedryansyah)mutia rasyaNo ratings yet

- Mergers and AcquisitionsDocument46 pagesMergers and Acquisitionszyra liam styles0% (1)

- Combine PDFDocument77 pagesCombine PDFKriztela CuisiaNo ratings yet

- Chapter 1 - IBFDocument11 pagesChapter 1 - IBFmariumzehraNo ratings yet

- Acceptance Criteria For Foreign InvestmentsDocument20 pagesAcceptance Criteria For Foreign InvestmentsHarsh Vardhan GuptaNo ratings yet

- Tutorial-1 FMADocument5 pagesTutorial-1 FMALê Thiên Giang 2KT-19No ratings yet

- Chapter 15 Alternative Restructuring StrategiesDocument22 pagesChapter 15 Alternative Restructuring StrategiesSAna KhAnNo ratings yet

- Solutions Corporate FinanceDocument28 pagesSolutions Corporate FinanceUsman UddinNo ratings yet

- BP Dividend Valuation FinancingDocument31 pagesBP Dividend Valuation FinancingTowhidul IslamNo ratings yet

- FIN Ass MSE 13 AprilDocument5 pagesFIN Ass MSE 13 AprilHarshit gargNo ratings yet

- Inv. Ch-5&6-1Document76 pagesInv. Ch-5&6-1Mahamoud HassenNo ratings yet

- Financing, Accounting and Taxation On Merger and AcquisitionDocument26 pagesFinancing, Accounting and Taxation On Merger and AcquisitionHesty OktarizaNo ratings yet

- Mergers and Acquisitions PDFDocument65 pagesMergers and Acquisitions PDFAhmad QuNo ratings yet

- Factors Affecting Cost of CapitalDocument11 pagesFactors Affecting Cost of CapitalGairik Deb100% (4)

- VCE SUMMMER INTERNSHIP PROGRAM (Financial Modellimg Task 3)Document10 pagesVCE SUMMMER INTERNSHIP PROGRAM (Financial Modellimg Task 3)Annu KashyapNo ratings yet

- Chapter 13 - Corporate Financing and Market Efficiency (Pages 351 - 354, 368 - 369)Document4 pagesChapter 13 - Corporate Financing and Market Efficiency (Pages 351 - 354, 368 - 369)Rajendra LamsalNo ratings yet

- Capital Structure: Limits To The: Use of DebtDocument9 pagesCapital Structure: Limits To The: Use of DebtLâm Thanh Huyền NguyễnNo ratings yet

- Ch.1 Overview of Financial Management and Financial EnvironmentDocument37 pagesCh.1 Overview of Financial Management and Financial EnvironmentNguyễn ThảoNo ratings yet

- Week 2 TUTE Chapter 1 SolutionsDocument6 pagesWeek 2 TUTE Chapter 1 SolutionsDylan AdrianNo ratings yet

- Overview of Financial ManagementDocument187 pagesOverview of Financial ManagementashrawNo ratings yet

- Module 4-CoC-1Document13 pagesModule 4-CoC-1Abida RiazNo ratings yet

- IGNOU MBA MS - 04 Solved Assignment 2011Document16 pagesIGNOU MBA MS - 04 Solved Assignment 2011Kiran PattnaikNo ratings yet

- 05-01-09 How To Value E and P CompaniesDocument6 pages05-01-09 How To Value E and P CompaniesGabby BlazaNo ratings yet

- Strategic AnalysisDocument20 pagesStrategic AnalysisUserNo ratings yet

- Profit and Shareholder MaximizationDocument23 pagesProfit and Shareholder MaximizationDaodu Ladi BusuyiNo ratings yet

- Corp - Restructuring, Lbo, MboDocument54 pagesCorp - Restructuring, Lbo, MboRaveendra RaoNo ratings yet

- IGNOU MBA MS - 04 Solved Assignment 2011Document12 pagesIGNOU MBA MS - 04 Solved Assignment 2011Nazif LcNo ratings yet

- Project Finance Question Bank: 1) What Is Financial Appraisal? What Are The Factors To Be Considered For Preparing It?Document47 pagesProject Finance Question Bank: 1) What Is Financial Appraisal? What Are The Factors To Be Considered For Preparing It?Anvesha TyagiNo ratings yet

- Bva 3Document7 pagesBva 3najaneNo ratings yet

- READING 11 Private Company ValuationDocument33 pagesREADING 11 Private Company ValuationDandyNo ratings yet

- UEU Manajemen Keuangan Pertemuan 7Document42 pagesUEU Manajemen Keuangan Pertemuan 7HendriMaulanaNo ratings yet

- Caiib Fmmodbacs Nov08Document91 pagesCaiib Fmmodbacs Nov08monirba48No ratings yet

- CAIIB-Financial Management-Module B Study of Financial StatementsDocument91 pagesCAIIB-Financial Management-Module B Study of Financial StatementsDeepak RathoreNo ratings yet

- Merger & Akuisisi TKMKDocument65 pagesMerger & Akuisisi TKMKArieAnggono100% (1)

- Af208 Fe s1 2018 Revision Package - SolutionsDocument20 pagesAf208 Fe s1 2018 Revision Package - SolutionsAryan KalyanNo ratings yet

- Financial Management CTDocument7 pagesFinancial Management CTJoy NathNo ratings yet

- Potential Agency ProblemsDocument16 pagesPotential Agency ProblemslimsterryNo ratings yet

- Chapter 1Document6 pagesChapter 1amelia gemNo ratings yet

- CFA Level 1 Corporate Finance E Book - Part 2Document31 pagesCFA Level 1 Corporate Finance E Book - Part 2Zacharia VincentNo ratings yet

- Financial ManagementDocument26 pagesFinancial ManagementbassramiNo ratings yet

- Exam QA - Corporate Finance-1Document38 pagesExam QA - Corporate Finance-1NigarNo ratings yet

- CFINDocument10 pagesCFINAnuj AgarwalNo ratings yet

- Corporate Finance Assignment 1Document6 pagesCorporate Finance Assignment 1Kûnãl SälîañNo ratings yet

- Dwnload Full Foundations of Financial Management Canadian 9th Edition Hirt Solutions Manual PDFDocument36 pagesDwnload Full Foundations of Financial Management Canadian 9th Edition Hirt Solutions Manual PDFhenrykr7men100% (12)

- Strategic Analysis For More Profitable AcquisitionsDocument26 pagesStrategic Analysis For More Profitable Acquisitionsankur khudaniaNo ratings yet

- An Overview of Financial Management: Answers To End-Of-Chapter QuestionsDocument7 pagesAn Overview of Financial Management: Answers To End-Of-Chapter QuestionsDaodu Ladi BusuyiNo ratings yet

- Chapter Outline 28Document16 pagesChapter Outline 28Yajie ZouNo ratings yet

- Capital Structure: Limits To The: Use of DebtDocument9 pagesCapital Structure: Limits To The: Use of DebtArini FalahiyahNo ratings yet

- Financial DistressDocument5 pagesFinancial DistresspalkeeNo ratings yet

- Vce Smart Task 3 (Project Finance) PDFDocument3 pagesVce Smart Task 3 (Project Finance) PDFRonak Jain83% (6)

- Unit 5 6TH Sem CemDocument6 pagesUnit 5 6TH Sem CemParas HarsheNo ratings yet

- Unit V IOME Sem VDocument6 pagesUnit V IOME Sem VJagmohan Rajput100% (1)

- Settling KlayDocument1 pageSettling KlayBharatSubramonyNo ratings yet

- Marketing Calendar 2019Document6 pagesMarketing Calendar 2019BharatSubramonyNo ratings yet

- Titan Eyeplus PrescriptionDocument2 pagesTitan Eyeplus PrescriptionBharatSubramonyNo ratings yet

- Beneficiary Nomination-GratuityDocument2 pagesBeneficiary Nomination-GratuityBharatSubramonyNo ratings yet

- Price ... ///////////// SizeDocument3 pagesPrice ... ///////////// SizeBharatSubramonyNo ratings yet

- Beneficiary Nomination-Provident FundDocument2 pagesBeneficiary Nomination-Provident FundBharatSubramonyNo ratings yet

- alkylphenolMST2013978 87 92903 99 0Document181 pagesalkylphenolMST2013978 87 92903 99 0BharatSubramonyNo ratings yet

- 2018 TV Portfolio BaseDocument18 pages2018 TV Portfolio BaseBharatSubramonyNo ratings yet

- Ethoxylates AlkylphenolsDocument16 pagesEthoxylates AlkylphenolsBharatSubramonyNo ratings yet

- Qualification Institute Board/University Year % / CgpaDocument1 pageQualification Institute Board/University Year % / CgpaBharatSubramonyNo ratings yet

- Marico Over The Wall Sales Case StudyDocument4 pagesMarico Over The Wall Sales Case StudyBharatSubramonyNo ratings yet

- Gas Turbines:: Moving To Prime TimeDocument4 pagesGas Turbines:: Moving To Prime TimeBharatSubramonyNo ratings yet

- Rural Marketing Competitive Strategies-614Document8 pagesRural Marketing Competitive Strategies-614BharatSubramonyNo ratings yet

- A3 Cola WarsDocument29 pagesA3 Cola WarsBharatSubramonyNo ratings yet

- Group B04 - MM2 - Pepper Spray Product LaunchDocument34 pagesGroup B04 - MM2 - Pepper Spray Product LaunchBharatSubramonyNo ratings yet

- Group4 AppleDocument28 pagesGroup4 AppleBharatSubramonyNo ratings yet

- Operation Study and Analysis of Steel Rolling MillDocument31 pagesOperation Study and Analysis of Steel Rolling MillBharatSubramony100% (1)

- Credit Policy of J&K BankDocument64 pagesCredit Policy of J&K BankBilal Ah Parray100% (3)

- IS Milan New Student Fees 23 24Document1 pageIS Milan New Student Fees 23 24Bharani DhanasekarNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSaran ManiNo ratings yet

- Asma RiskDocument2 pagesAsma RiskAsma ShoaibNo ratings yet

- 12 - Consolidated Financial Statement (July 23) 1Document474 pages12 - Consolidated Financial Statement (July 23) 1Shaheryar ShahidNo ratings yet

- Finals Mathematics of InvestmentDocument5 pagesFinals Mathematics of InvestmentJohn Rhimon Abaga Gelacio100% (1)

- MP and The Crisis - SvensonDocument6 pagesMP and The Crisis - SvensonDamien PuyNo ratings yet

- (Download pdf) Macroeconomics Principles And Policy 14Th Edition William J Baumol full chapter pdf docxDocument69 pages(Download pdf) Macroeconomics Principles And Policy 14Th Edition William J Baumol full chapter pdf docxkgobebazoge100% (5)

- Stock MarketDocument31 pagesStock MarketNugusayoNo ratings yet

- International BankingDocument25 pagesInternational Bankingvikas nabikNo ratings yet

- Early Release of Super - Human ServicesDocument10 pagesEarly Release of Super - Human ServicesOzDamo2No ratings yet

- Variable Examination Review Session (Verse) Mock ExamDocument12 pagesVariable Examination Review Session (Verse) Mock ExamArvinALNo ratings yet

- Name Desc Logo Binance Coin Ethereum Tether SolanaDocument30 pagesName Desc Logo Binance Coin Ethereum Tether SolanaNgoc Son PhamNo ratings yet

- ReceiptDocument2 pagesReceiptleandrosouza.dasilva14No ratings yet

- ISFM Equity Market Module PDFDocument99 pagesISFM Equity Market Module PDFISFM, Stock Market SchoolNo ratings yet

- AS 24 Discontinuing OperationsDocument14 pagesAS 24 Discontinuing OperationsHemanth SNo ratings yet

- Currency WarDocument25 pagesCurrency WarSumanta Kumar BiswalNo ratings yet

- Cash Flow Statement ProblemsDocument11 pagesCash Flow Statement ProblemsRaman SachdevaNo ratings yet

- Estmt - 2021-05-06 2Document6 pagesEstmt - 2021-05-06 2Moctar GueyeNo ratings yet

- Harshad Mehta ScamDocument20 pagesHarshad Mehta ScamRohan MahabalNo ratings yet

- Mcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument13 pagesMcgraw-Hill/Irwin © 2004 The Mcgraw-Hill Companies, Inc., All Rights ReservedHarpreet SinghNo ratings yet

- Ednovate CAF Accounts UT 1 QDocument3 pagesEdnovate CAF Accounts UT 1 QROCKYNo ratings yet

- IntroductionDocument58 pagesIntroductionSumit AgarwalNo ratings yet

- Handout ASI 2405 FS RestatementDocument4 pagesHandout ASI 2405 FS RestatementMaureen Kaye PaloNo ratings yet

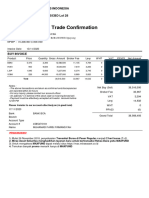

- Trade ConfirmationDocument1 pageTrade ConfirmationCKS CateringNo ratings yet

- Kanalu-Linda T. Darling - Revenue Raising and Legitimacy - Tax Collection and Finance Administration in The Ottoman EmpireDocument30 pagesKanalu-Linda T. Darling - Revenue Raising and Legitimacy - Tax Collection and Finance Administration in The Ottoman EmpireChristian Camilo Casas GarcíaNo ratings yet

- SVS Fuel Station - TrialDocument4 pagesSVS Fuel Station - TrialRCA SHARMANo ratings yet

- Finance ExamDocument14 pagesFinance ExamAnanthu NairNo ratings yet