You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Home Trade ScamDocument6 pagesHome Trade ScamVikas Barbhaya100% (1)

- Ebtke Conex 2012 ProposalDocument15 pagesEbtke Conex 2012 ProposalFahmi Adha NurdinNo ratings yet

- Strategy TemplatesDocument52 pagesStrategy TemplatesMathias Wafawanaka100% (3)

- Zero Bound Elsarticle-RevisedDocument43 pagesZero Bound Elsarticle-RevisedBrunéNo ratings yet

- Challenges in Agribusiness in NigeriaDocument3 pagesChallenges in Agribusiness in NigeriaTomilola Odejayi Balogun50% (2)

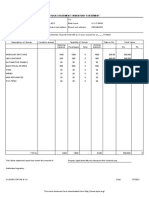

- Stock Statement Format For Bank LoanDocument1 pageStock Statement Format For Bank Loanpsycho Neha40% (5)

- BAIUBRMW2Formulating The TopicExampleDocument10 pagesBAIUBRMW2Formulating The TopicExampleTrungNgôNo ratings yet

- Presentation The Vega Trap Dan Passarelli PDFDocument45 pagesPresentation The Vega Trap Dan Passarelli PDFabiel_guerraNo ratings yet

- Kaleleoul FanatyeDocument72 pagesKaleleoul FanatyeWonde GebeyehuNo ratings yet

- Bolivar NI43-101 TR 470200-160 Rev23 20170406Document264 pagesBolivar NI43-101 TR 470200-160 Rev23 20170406Anonymous cMBxGA100% (1)

- 1h Bingham CH 8 Prof Chauvins Instructions Student VersionDocument9 pages1h Bingham CH 8 Prof Chauvins Instructions Student VersionAstha GoplaniNo ratings yet

- How Will The Belt and Road Initiative Advance ChinaDocument7 pagesHow Will The Belt and Road Initiative Advance ChinaGundeep SinghNo ratings yet

- Ethanol From Sugar - Gareth Forber AOF2022Document18 pagesEthanol From Sugar - Gareth Forber AOF2022Parush PatelNo ratings yet

- Pre-Colonial EraDocument126 pagesPre-Colonial Era1400440% (5)

- Cle F ArcusbalslDocument2 pagesCle F ArcusbalslGanesh VijayNo ratings yet

- RCC Question BankDocument3 pagesRCC Question BankPurab PatelNo ratings yet

- Naac Criteria 4Document7 pagesNaac Criteria 4veerpathranNo ratings yet

- 4 - DeclarationDocument1 page4 - DeclarationSonu YadavNo ratings yet

- Consulting Resource GuideDocument7 pagesConsulting Resource Guideivon86No ratings yet

- Return Service AgreementDocument1 pageReturn Service Agreementkay tunaNo ratings yet

- Hold - Definition of Hold by Merriam-WebsterDocument3 pagesHold - Definition of Hold by Merriam-WebsterGenelle Mae MadrigalNo ratings yet

- Purposive Communication 4Document38 pagesPurposive Communication 4Rod TempraNo ratings yet

- Why BGC Is The Next CBDDocument8 pagesWhy BGC Is The Next CBDEnp Gus AgostoNo ratings yet

- Pom Class Notes - OrganisingDocument70 pagesPom Class Notes - OrganisingKumarNo ratings yet

- 02.18 - SCahilog - FOI - List of CoopsDocument2,102 pages02.18 - SCahilog - FOI - List of Coopsero feinaNo ratings yet

- Corporation Law Outline (Jacinto)Document16 pagesCorporation Law Outline (Jacinto)anon-856821100% (2)

- ECO 2020 Syllabus 2014Document7 pagesECO 2020 Syllabus 2014inlukashaNo ratings yet

- Course Outline PFMDocument7 pagesCourse Outline PFMmohamedNo ratings yet

- Framing MMT - Modern Money NetworkDocument23 pagesFraming MMT - Modern Money NetworkUmkc Economists86% (7)

- A Brief On NPS & RFBDocument2 pagesA Brief On NPS & RFBRushikeshRameshchandraLachureNo ratings yet