You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Sample Business StatementDocument4 pagesSample Business StatementLy Hoang100% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Bank Statement Abbreviations Found On BankDocument3 pagesBank Statement Abbreviations Found On BankRobert D.PalbanNo ratings yet

- E BankingDocument3 pagesE BankingSumedhaa Srivastava 34 Sem-1,CNo ratings yet

- SAP FI-MM-SD IntegrationDocument13 pagesSAP FI-MM-SD IntegrationAniruddha ChakrabortyNo ratings yet

- URr VG EZsy Y0 VHHJ YDocument3 pagesURr VG EZsy Y0 VHHJ YNitin DawarNo ratings yet

- Fee StatusDocument1 pageFee StatusYogeshNo ratings yet

- Glossary of Banking Terms and DefinitionsDocument23 pagesGlossary of Banking Terms and Definitionsalok_sycogony1No ratings yet

- CHOICE Australia - April 2023Document76 pagesCHOICE Australia - April 2023Emilian GomoiNo ratings yet

- Account StatementDocument2 pagesAccount StatementDebashis MahantaNo ratings yet

- Project Report On Bank of AsiaDocument54 pagesProject Report On Bank of AsiaSeema Chapagain100% (1)

- CreditCardCreditAgreement 1323-28042013Document7 pagesCreditCardCreditAgreement 1323-28042013Fabian DeeNo ratings yet

- Statement of Axis Account No:080010100183918 For The Period (From: 19-10-2020 To: 18-10-2021)Document4 pagesStatement of Axis Account No:080010100183918 For The Period (From: 19-10-2020 To: 18-10-2021)Ketan PatelNo ratings yet

- Improving Security Challeges of Atm System in Commercial Bank of Ethiopia: The Case of Wolaita Zone, Sodo CityDocument21 pagesImproving Security Challeges of Atm System in Commercial Bank of Ethiopia: The Case of Wolaita Zone, Sodo CityInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- BillImage 1Document3 pagesBillImage 1Carlos Andres Barrera CastillaNo ratings yet

- UBL Internship ReportDocument68 pagesUBL Internship ReportAisha rashid100% (1)

- CCAvenue Integration - Ver 2.0Document33 pagesCCAvenue Integration - Ver 2.0Pravin ThakurNo ratings yet

- TJJ810322503278RPOSDocument2 pagesTJJ810322503278RPOSRakesh MataiNo ratings yet

- IPCE - November - 2022 - Guidance Notes - SifyDocument23 pagesIPCE - November - 2022 - Guidance Notes - SifySakshiK ChaturvediNo ratings yet

- Shyam Prasad Singh vs. Birla Sun Life Insurance LimitedDocument11 pagesShyam Prasad Singh vs. Birla Sun Life Insurance LimitedVikas DeniaNo ratings yet

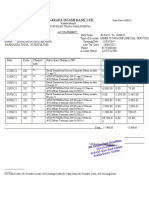

- Al-Arafa Islami Bank LTD.: V-V - V - V - V - V - V - V - VDocument2 pagesAl-Arafa Islami Bank LTD.: V-V - V - V - V - V - V - V - VRaju AhamedNo ratings yet

- Pep Boys Visa Prepaid Card Rebate Claim FormDocument2 pagesPep Boys Visa Prepaid Card Rebate Claim FormHarry SamsungNo ratings yet

- 21 Down 16 Down ECS Information InstructionsDocument3 pages21 Down 16 Down ECS Information Instructionsmnj_gautamNo ratings yet

- FAQsDocument3 pagesFAQsManikanta Sai KumarNo ratings yet

- MAR 2020 eBill-Vodafone PDFDocument4 pagesMAR 2020 eBill-Vodafone PDFNikunjNo ratings yet

- Fixedline and Broadband Services: Your Account Summary This Month'S ChargesDocument2 pagesFixedline and Broadband Services: Your Account Summary This Month'S ChargesnarakribNo ratings yet

- Jio 9Document1 pageJio 9dwall29292No ratings yet

- Bank ReconciliationDocument4 pagesBank ReconciliationNalan TafanaNo ratings yet

- Kevin O DonnellDocument4 pagesKevin O DonnellITNo ratings yet

- ConnectPay UABDocument17 pagesConnectPay UABAhmer HussainNo ratings yet

- Lntership ReportDocument52 pagesLntership ReportShivraj JoshiNo ratings yet