You might also like

- RoarDocument19 pagesRoarFrank HernandezNo ratings yet

- CH 04 Income StatementDocument6 pagesCH 04 Income Statementnreid2701No ratings yet

- Net Revenue and Net ProfitDocument2 pagesNet Revenue and Net ProfitZahid5391No ratings yet

- Example Income Statement:: Gross SalesDocument2 pagesExample Income Statement:: Gross Salesabdirahman YonisNo ratings yet

- Income StatementDocument36 pagesIncome StatementTiffany VinzonNo ratings yet

- Income StatementDocument8 pagesIncome StatementDanDavidLapizNo ratings yet

- Weak Leaner ActivityDocument5 pagesWeak Leaner ActivityAshwini shenolkarNo ratings yet

- Principles of Accounting: Income StatementDocument5 pagesPrinciples of Accounting: Income StatementAhmad GraphicsNo ratings yet

- Income StatementDocument1 pageIncome StatementHabib Ul HaqNo ratings yet

- Income Statement Account TitlesDocument16 pagesIncome Statement Account Titlesmaria cacaoNo ratings yet

- Income StatementsDocument5 pagesIncome StatementsAdetunbi TolulopeNo ratings yet

- Summary Ch4 & Ch5Document10 pagesSummary Ch4 & Ch5beenishyousafNo ratings yet

- Profit and Loss Statement TemplateDocument8 pagesProfit and Loss Statement TemplateJerarudo BoknoyNo ratings yet

- Income StatementDocument3 pagesIncome StatementMamta LallNo ratings yet

- Inc StatmentDocument3 pagesInc StatmentDilawarNo ratings yet

- Left Column For Inner Computation - Right Column For Totals - Peso Sign at The Beginning Amount and at Final Answer TwoDocument6 pagesLeft Column For Inner Computation - Right Column For Totals - Peso Sign at The Beginning Amount and at Final Answer Twoamberle smithNo ratings yet

- Statement of Comprehensive IncomeDocument18 pagesStatement of Comprehensive IncomeCharies Dingal100% (1)

- Buying and Selling: and Net Profit/LossDocument19 pagesBuying and Selling: and Net Profit/LossMarc Graham NacuaNo ratings yet

- 5.3 Income StatementsDocument3 pages5.3 Income StatementsannabellNo ratings yet

- How To Write A Traditional Business Plan: Step 1Document5 pagesHow To Write A Traditional Business Plan: Step 1Leslie Ann Elazegui UntalanNo ratings yet

- Income Statement: Presented by HARI PRIYA - 102114025 JENKINS-102114026 ARVIND-102114027Document47 pagesIncome Statement: Presented by HARI PRIYA - 102114025 JENKINS-102114026 ARVIND-102114027Jenkins Jose Shirley100% (1)

- Income Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Document14 pagesIncome Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Dr. Satish Jangra100% (1)

- Income Statement: Profit and LossDocument7 pagesIncome Statement: Profit and LossNavya NarulaNo ratings yet

- Statement of Comprehensive IncomeDocument38 pagesStatement of Comprehensive IncomeDaphne Gesto SiaresNo ratings yet

- Statement of Comprehensive IncomeDocument25 pagesStatement of Comprehensive IncomeAngel Nichole ValenciaNo ratings yet

- Inc StatDocument9 pagesInc StatAleem JafferyNo ratings yet

- Lecture 5Document4 pagesLecture 5zehratmuzaffarNo ratings yet

- Fabm 2 - Lesson 2 - SCIDocument20 pagesFabm 2 - Lesson 2 - SCIwendell john medianaNo ratings yet

- Multi Step Income Statement For Merchadising BusinessDocument10 pagesMulti Step Income Statement For Merchadising Businessjesi zamoraNo ratings yet

- How To Prepare A Profit and Loss (Income) Statement: Zions Business Resource CenterDocument16 pagesHow To Prepare A Profit and Loss (Income) Statement: Zions Business Resource CenterSiti Asma MohamadNo ratings yet

- Variable Costs and Fixed CostsDocument2 pagesVariable Costs and Fixed CostsDon McArthney TugaoenNo ratings yet

- Fabm2 Week 4Document28 pagesFabm2 Week 4Jeremy SolomonNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive IncomeBlessylyn AguilarNo ratings yet

- What Is The Income Statement?Document3 pagesWhat Is The Income Statement?Mustaeen DarNo ratings yet

- Wiley - Chapter 4: Income Statement and Related InformationDocument42 pagesWiley - Chapter 4: Income Statement and Related InformationIvan Bliminse86% (7)

- Chapter 4 - StudentDocument46 pagesChapter 4 - StudenttsatsrallNo ratings yet

- 8 Financial StatementDocument11 pages8 Financial StatementLin Latt Wai AlexaNo ratings yet

- Accounting DocumentsDocument6 pagesAccounting DocumentsMae AroganteNo ratings yet

- Lesson 1.2: SciDocument4 pagesLesson 1.2: SciIshi MaxineNo ratings yet

- 2 Income Statement FormatDocument3 pages2 Income Statement Formatapi-299265916No ratings yet

- Chapter 4 - Reporting Financial PerformanceDocument6 pagesChapter 4 - Reporting Financial PerformanceCait PostNo ratings yet

- Finals - Fina 221Document14 pagesFinals - Fina 221MARITONI MEDALLANo ratings yet

- Understanding The Income StatementDocument4 pagesUnderstanding The Income Statementluvujaya100% (1)

- Business Studies: 5.3 - Income StatementsDocument9 pagesBusiness Studies: 5.3 - Income StatementsUpasana ChaubeNo ratings yet

- Financial Statement DefinitionsDocument4 pagesFinancial Statement Definitionsj_osire7483No ratings yet

- Income Statement TemplateDocument4 pagesIncome Statement TemplateAnonymous gFcnQ4goNo ratings yet

- Operating Income: Gross Profit Total Sales CogsDocument2 pagesOperating Income: Gross Profit Total Sales CogsBeth GuiangNo ratings yet

- Income Statement - Format - Types - ExampleDocument3 pagesIncome Statement - Format - Types - ExampleIoana DragneNo ratings yet

- Financial StatementDocument83 pagesFinancial StatementDarkie DrakieNo ratings yet

- Accounting For Non - Accountants - Simple - Business OperationsDocument37 pagesAccounting For Non - Accountants - Simple - Business OperationsTesda CACSNo ratings yet

- 2-Income StatementDocument22 pages2-Income StatementSanz GuéNo ratings yet

- FABM 2 Module 3 Statement of Comprehensive IncomeDocument10 pagesFABM 2 Module 3 Statement of Comprehensive IncomebabyjamskieNo ratings yet

- Expense - Expense Is A Type of Expenditure Which Go Through The Income Statement, ItDocument5 pagesExpense - Expense Is A Type of Expenditure Which Go Through The Income Statement, ItDanielNo ratings yet

- Statement of Comprehensive Income (SCI)Document35 pagesStatement of Comprehensive Income (SCI)Jung WonnieNo ratings yet

- Key Terms and Concepts - CH 09Document2 pagesKey Terms and Concepts - CH 09danterozaNo ratings yet

- Statement of Comprehensive IncomeDocument33 pagesStatement of Comprehensive IncomeZalvy Gwen RecimoNo ratings yet

- CFI Team 05072022 - Income StatementDocument8 pagesCFI Team 05072022 - Income StatementDR WONDERS PIBOWEINo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Hotel Aryaduta: The Heart of Contemporary IndonesiaDocument1 pageHotel Aryaduta: The Heart of Contemporary IndonesiaJahja AjaNo ratings yet

- Group 5 - Grolsch GloballyDocument3 pagesGroup 5 - Grolsch GloballyJahja AjaNo ratings yet

- WAC Apollo Hospitals - JahjaDocument2 pagesWAC Apollo Hospitals - JahjaJahja Aja0% (1)

- Exam International MarketingDocument1 pageExam International MarketingJahja AjaNo ratings yet

- Group 5 - Grolsch GloballyDocument3 pagesGroup 5 - Grolsch GloballyJahja AjaNo ratings yet

- Boiler Installation Project 1Document3 pagesBoiler Installation Project 1Jahja AjaNo ratings yet

- Ses 9 - The Fifth P in MarketingDocument5 pagesSes 9 - The Fifth P in MarketingJahja AjaNo ratings yet

- Ses 9 - Nissan's Carlos GhosnDocument14 pagesSes 9 - Nissan's Carlos GhosnJahja Aja100% (1)

- KPI Dictionary Vol1 PreviewDocument12 pagesKPI Dictionary Vol1 PreviewJahja Aja64% (11)

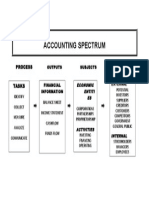

- Accounting SpectrumDocument1 pageAccounting SpectrumJahja AjaNo ratings yet

- Wendys AnalysisDocument31 pagesWendys AnalysisJahja Aja100% (1)