You might also like

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- Income Not Part of Total Income Full NotesDocument93 pagesIncome Not Part of Total Income Full NotesCA Rishabh DaiyaNo ratings yet

- BIR Ruling 555-12Document4 pagesBIR Ruling 555-12Rebecca ChanNo ratings yet

- NPS - Income Tax Deduction Under Section 80CCC and 80CCDDocument5 pagesNPS - Income Tax Deduction Under Section 80CCC and 80CCDManoj KakkarNo ratings yet

- Income Tax NitDocument6 pagesIncome Tax NitrensisamNo ratings yet

- All Rules of 80 CCD For CPS Employees Income Tax Deductions - APTEACHERS WebsiteDocument7 pagesAll Rules of 80 CCD For CPS Employees Income Tax Deductions - APTEACHERS Websitevinodtiwari808754No ratings yet

- FAQ On Budget FY 2020-21Document9 pagesFAQ On Budget FY 2020-21GUNANo ratings yet

- Salary Tax AssessmentDocument9 pagesSalary Tax Assessmentshuvo134No ratings yet

- IT Deductions Allowed Under Chapter VI-A Sec 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB Etc - APTEACHERS WebsiteDocument13 pagesIT Deductions Allowed Under Chapter VI-A Sec 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB Etc - APTEACHERS WebsiteKIMS IECNo ratings yet

- 18609cp7 PCC Compsuggans TaxationDocument6 pages18609cp7 PCC Compsuggans TaxationDeepal DhamejaNo ratings yet

- Taxiation AssignmentDocument9 pagesTaxiation AssignmentNoman AreebNo ratings yet

- Nepal Budget Highlights - 79-80 - APM & AssociatesDocument89 pagesNepal Budget Highlights - 79-80 - APM & Associatesaasthapoddar155No ratings yet

- Deduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009Document70 pagesDeduction of Tax at Source - Income-Tax Deduction From Salaries Under Section 192 of The Income-Tax Act, 1961 During The Financial Year 2008-2009rhldxmNo ratings yet

- CBDT Circular How To Calculate Tds On Salary For FY 1213Document64 pagesCBDT Circular How To Calculate Tds On Salary For FY 1213skybluehemaNo ratings yet

- Income Tax 2017 Edazdb1013Document50 pagesIncome Tax 2017 Edazdb1013Pradeep PatilNo ratings yet

- Circular On Serction 192 of The Income Tax Act 1961Document74 pagesCircular On Serction 192 of The Income Tax Act 1961Ayush ChatterjeeNo ratings yet

- Income Tax Circular No. 17/2014 Dated 10.12.14Document70 pagesIncome Tax Circular No. 17/2014 Dated 10.12.14Elisabeth MuellerNo ratings yet

- National Institute of Technology CalicutDocument7 pagesNational Institute of Technology CalicutraghuramaNo ratings yet

- 5.3 Exemptions From Income From SalariesDocument3 pages5.3 Exemptions From Income From SalariesYash DedhiaNo ratings yet

- Income Tax All Particulars 2013-14Document72 pagesIncome Tax All Particulars 2013-14kvsgssNo ratings yet

- AmendDocument25 pagesAmendanshulagarwal62No ratings yet

- Salient Features For Income TaxDocument6 pagesSalient Features For Income TaxRimsha AslamNo ratings yet

- When Will The New Scheme Be Applicable?: Faqs On Budget Fy 2020-21Document6 pagesWhen Will The New Scheme Be Applicable?: Faqs On Budget Fy 2020-21Biswabandhu PalNo ratings yet

- Budget 2015 Proposes Additional Deduction of Up To Rs. 50000/-Under Section 80CCD For National Pension System ContributionDocument1 pageBudget 2015 Proposes Additional Deduction of Up To Rs. 50000/-Under Section 80CCD For National Pension System ContributionalisagasaNo ratings yet

- 31188sm DTL Finalnew-May-Nov14 Cp28Document66 pages31188sm DTL Finalnew-May-Nov14 Cp28gvcNo ratings yet

- The Budget 2011 - A Glimpse: Shetty Prabhu & AshokDocument15 pagesThe Budget 2011 - A Glimpse: Shetty Prabhu & AshokMadhusudan MagajiNo ratings yet

- Question and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofDocument6 pagesQuestion and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofAnamika VatsaNo ratings yet

- 1 .Income Tax On Salaries - (01.06.2015)Document57 pages1 .Income Tax On Salaries - (01.06.2015)yvNo ratings yet

- Dfletter AllDocument11 pagesDfletter AllelangoNo ratings yet

- Budget 2013 - 2014Document11 pagesBudget 2013 - 2014sdfdhgtj894No ratings yet

- Bonus Act, 2030 (1974) Last AmendmentsDocument11 pagesBonus Act, 2030 (1974) Last AmendmentsDeep JoshiNo ratings yet

- Salient Features Income Tax)Document5 pagesSalient Features Income Tax)bbaahmad89No ratings yet

- Income Tax Circular For FY 2015-16 PDFDocument77 pagesIncome Tax Circular For FY 2015-16 PDFvaibhinavNo ratings yet

- Direct Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnDocument5 pagesDirect Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnPriya KudnekarNo ratings yet

- IT Circular 2011-12Document56 pagesIT Circular 2011-12Narasimha SastryNo ratings yet

- Deductions On Section 80CDocument12 pagesDeductions On Section 80CViraja GuruNo ratings yet

- Tax Updates For December 2011 31 10 2011Document35 pagesTax Updates For December 2011 31 10 2011gangadhardaNo ratings yet

- Tax Updates For December 2011 31 10 2011Document35 pagesTax Updates For December 2011 31 10 2011Rakhi ChaubeyNo ratings yet

- 80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensDocument1 page80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensArjun VermaNo ratings yet

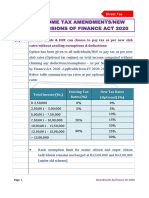

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Tax UpdateDocument149 pagesTax UpdateJamz LopezNo ratings yet

- Changes in GSTDocument4 pagesChanges in GSTRanjodh KaurNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- 30851ipcc May Nov14 It Vol1 CP 9.unlockedDocument43 pages30851ipcc May Nov14 It Vol1 CP 9.unlockedavesatanas13No ratings yet

- Part I: Statutory Update: © The Institute of Chartered Accountants of IndiaDocument4 pagesPart I: Statutory Update: © The Institute of Chartered Accountants of IndiaRamanNo ratings yet

- Taxation Assignment Budget Proposal 2020Document20 pagesTaxation Assignment Budget Proposal 2020Shivani DuttNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- 80C IndiaDocument7 pages80C IndiapingbadriNo ratings yet

- Income From House Property Income From Business or Profession Capital Gains Income From Other SourcesDocument4 pagesIncome From House Property Income From Business or Profession Capital Gains Income From Other SourcesPooja TanejaNo ratings yet

- Salient Features For The Budget 2010-11Document11 pagesSalient Features For The Budget 2010-11kaashifhassanNo ratings yet

- Indian Institute of Technology Madras: CircularDocument5 pagesIndian Institute of Technology Madras: CircularAravinthram R am18m002No ratings yet

- Disclaimer: Dr. Satish Modi Assistant Professor Department of Commerce, IGN Tribal University, Amarkantak (M.P.)Document26 pagesDisclaimer: Dr. Satish Modi Assistant Professor Department of Commerce, IGN Tribal University, Amarkantak (M.P.)VENKATESWARLUMCOMNo ratings yet

- 100 Eou SchemeDocument4 pages100 Eou SchemeD Attitude KidNo ratings yet

- Deductions From Gross Total Income: HapterDocument20 pagesDeductions From Gross Total Income: HapterJAWED MOHAMMADNo ratings yet

- GST Update124Document6 pagesGST Update124suhani singhNo ratings yet

- Moot ProblemDocument14 pagesMoot ProblemSaumya RaizadaNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Proc For Aided School - 28 08 2010Document2 pagesProc For Aided School - 28 08 2010TNGTFNo ratings yet

- Proc 02082010Document2 pagesProc 02082010TNGTFNo ratings yet

- G.O.No.198 dt.21.07.09Document9 pagesG.O.No.198 dt.21.07.09TNGTFNo ratings yet

- Elementary Dir Proceeding Dated 05/08/2010Document3 pagesElementary Dir Proceeding Dated 05/08/2010TNGTFNo ratings yet

- G.O.No.196 dt.19.07.09Document15 pagesG.O.No.196 dt.19.07.09TNGTFNo ratings yet

- GO MS NO 270, Dated 26.08.2010Document1 pageGO MS NO 270, Dated 26.08.2010TNGTF0% (1)

- Fin e 51082 2010Document19 pagesFin e 51082 2010kailasasundaramNo ratings yet

- Elementary Dir Proceeding Dated 05/08/2010Document3 pagesElementary Dir Proceeding Dated 05/08/2010TNGTFNo ratings yet

- Aasan Madal June July 2010Document2 pagesAasan Madal June July 2010TNGTFNo ratings yet

- Aasan Madal June-July 2010Document2 pagesAasan Madal June-July 2010TNGTFNo ratings yet

- G.O.No.196 dt.19.07.09Document15 pagesG.O.No.196 dt.19.07.09TNGTFNo ratings yet

- Aasan Madal June July 2010Document2 pagesAasan Madal June July 2010TNGTFNo ratings yet

- Kovai PhooDocument1 pageKovai PhooTNGTFNo ratings yet

- Kovai PhooDocument1 pageKovai PhooTNGTFNo ratings yet

- Kovai Semmozhi ManaduDocument1 pageKovai Semmozhi ManaduTNGTFNo ratings yet

- GO - NO 26 Dated 12.02.2010Document2 pagesGO - NO 26 Dated 12.02.2010TNGTFNo ratings yet

- GO No.65 Date 15.03.10Document1 pageGO No.65 Date 15.03.10TNGTFNo ratings yet

- SamaCheer Kalvi Commity MeetingDocument1 pageSamaCheer Kalvi Commity MeetingTNGTFNo ratings yet

- Pca Ii InstallmentDocument1 pagePca Ii InstallmentTNGTFNo ratings yet

- Transfer Relieving - Dated Ele - Dir Proceeding 12300/d1/2010 Dated 31.05.2010Document1 pageTransfer Relieving - Dated Ele - Dir Proceeding 12300/d1/2010 Dated 31.05.2010TNGTFNo ratings yet

- G.O. No.64 Dated 15.03.10Document4 pagesG.O. No.64 Dated 15.03.10TNGTFNo ratings yet

- Tamilnadu Govt 10% DA HIKE (35% To 45%) GO 371 24.9.2010 EnglishDocument3 pagesTamilnadu Govt 10% DA HIKE (35% To 45%) GO 371 24.9.2010 EnglishMohankumar P KNo ratings yet

- GO No.65 Date 15.03.10Document1 pageGO No.65 Date 15.03.10TNGTFNo ratings yet

- Villupuram District TNGTF MeetingDocument3 pagesVillupuram District TNGTF MeetingTNGTFNo ratings yet

- GO No.65 Date 15.03.10Document1 pageGO No.65 Date 15.03.10TNGTFNo ratings yet

- G.O. No.64 Dated 15.03.10Document4 pagesG.O. No.64 Dated 15.03.10TNGTFNo ratings yet

- Pca Ii InstallmentDocument1 pagePca Ii InstallmentTNGTFNo ratings yet

- G.O. No.64 Dated 15.03.10Document4 pagesG.O. No.64 Dated 15.03.10TNGTFNo ratings yet