You might also like

- Financial Due DiligenceDocument10 pagesFinancial Due Diligenceapi-3822396100% (6)

- FD FeaturesDocument4 pagesFD FeaturesSitaKumari100% (1)

- Kinds of SecuritiesDocument6 pagesKinds of Securitiesdeepa100% (6)

- A simple approach to bond trading: The introductory guide to bond investments and their portfolio managementFrom EverandA simple approach to bond trading: The introductory guide to bond investments and their portfolio managementRating: 5 out of 5 stars5/5 (1)

- Degree CertificateDocument1 pageDegree CertificateVishal DhekaleNo ratings yet

- Financial DerivativesDocument108 pagesFinancial Derivativesramesh158No ratings yet

- Financial Derivatives: Robert M. Hayes 2002Document108 pagesFinancial Derivatives: Robert M. Hayes 2002Suryanarayanan VenkataramananNo ratings yet

- Financial DerivativesDocument24 pagesFinancial DerivativesResmi NidhinNo ratings yet

- Financial DerivativesDocument6 pagesFinancial DerivativesAlfred osafo100% (4)

- Algorithmic Trading (ALGO Trading) : Algorithmic Trading (Also Called Automated Trading, BlackDocument5 pagesAlgorithmic Trading (ALGO Trading) : Algorithmic Trading (Also Called Automated Trading, BlacksamikhanNo ratings yet

- Investment LawDocument11 pagesInvestment LawHarmanSinghNo ratings yet

- Derivative (Finance) : UsesDocument20 pagesDerivative (Finance) : Usescuteperson01No ratings yet

- Evolution of Derivatives Market in IndiaDocument4 pagesEvolution of Derivatives Market in IndiaSujeet GuptaNo ratings yet

- Derivative Markets: S.Y.B.F.MDocument20 pagesDerivative Markets: S.Y.B.F.MBhagyesh ShahNo ratings yet

- O o o o O: Option (Finance)Document12 pagesO o o o O: Option (Finance)waibhavNo ratings yet

- Derivative Instruments: in The Financial Marketplace Some Instruments Are Regarded AsDocument53 pagesDerivative Instruments: in The Financial Marketplace Some Instruments Are Regarded AsRita NyairoNo ratings yet

- Derivates NotesDocument7 pagesDerivates NotesSachin MethreeNo ratings yet

- W ElcomeDocument18 pagesW ElcomeRamesha SNo ratings yet

- Prakash 123Document47 pagesPrakash 123Prakash VishwakarmaNo ratings yet

- Notes F.D. Unit - 4Document15 pagesNotes F.D. Unit - 4kamya saxenaNo ratings yet

- Financial Instrument Asset Index Underlying Futures ContractDocument9 pagesFinancial Instrument Asset Index Underlying Futures Contractkristel-marie-pitogo-4419No ratings yet

- Finance: Sources of FundingDocument11 pagesFinance: Sources of FundingvikysaraNo ratings yet

- TypesofswapDocument5 pagesTypesofswapshweta jaiswalNo ratings yet

- Security (Finance)Document11 pagesSecurity (Finance)jackie555No ratings yet

- What Are Derivative InstrumentsDocument3 pagesWhat Are Derivative InstrumentsAnonymous PXYboWdvm100% (1)

- SwapDocument3 pagesSwapJohana ReyesNo ratings yet

- Derivatives and OptionsDocument23 pagesDerivatives and OptionsSathya Keerthy KNo ratings yet

- Financial Derivtives Futures & Options at KarvyDocument95 pagesFinancial Derivtives Futures & Options at KarvycityNo ratings yet

- Swaps ForexDocument6 pagesSwaps ForexNeeti KhanchandaniNo ratings yet

- Fixed Income Overview W-O Derivatives & W-O ForeignDocument13 pagesFixed Income Overview W-O Derivatives & W-O ForeignTrisha BolastigNo ratings yet

- Finance Interview Questions For Financial AnalystDocument3 pagesFinance Interview Questions For Financial Analystnishi100% (1)

- Bond MarketDocument5 pagesBond MarketJonahNo ratings yet

- What Does Derivative Mean?Document23 pagesWhat Does Derivative Mean?shrikantyemulNo ratings yet

- Derivatives: You Need To Know About Derivatives TradingDocument35 pagesDerivatives: You Need To Know About Derivatives TradingPooja mahadikNo ratings yet

- Financial Assets MarketDocument4 pagesFinancial Assets MarketShellian CunninghamNo ratings yet

- Financial Terms: AccountDocument13 pagesFinancial Terms: AccountrajbrinderNo ratings yet

- Forward Contract Future ContractDocument10 pagesForward Contract Future ContractSanjai SivañanthamNo ratings yet

- Investment Chapter 1Document22 pagesInvestment Chapter 1History and EventNo ratings yet

- Repos: SecuritiesDocument5 pagesRepos: SecuritiesSURYANo ratings yet

- DerivativesDocument18 pagesDerivativesJay Lord FlorescaNo ratings yet

- DerivativesDocument17 pagesDerivativesnehal panchasaraNo ratings yet

- Off Balance SheetDocument15 pagesOff Balance SheetHussain khawajaNo ratings yet

- Security (Finance) : ClassificationDocument10 pagesSecurity (Finance) : ClassificationAnulekha AtriNo ratings yet

- Chapter 6Document5 pagesChapter 6Muhammed YismawNo ratings yet

- What Is The Money MarketDocument22 pagesWhat Is The Money MarketMuhammad HasnainNo ratings yet

- Financial SecurityDocument3 pagesFinancial SecurityJackie BallaranNo ratings yet

- Financial DerivativesDocument64 pagesFinancial DerivativesKirabpalNo ratings yet

- Lai Suat 05fm9Document12 pagesLai Suat 05fm9Huu DuyNo ratings yet

- Please Read: A Personal Appeal From Wikipedia Founder Jimmy WalesDocument14 pagesPlease Read: A Personal Appeal From Wikipedia Founder Jimmy WalesJay BhattNo ratings yet

- Introduction of DerivativesDocument23 pagesIntroduction of DerivativesBhavani Singh RathoreNo ratings yet

- Sip ReportDocument77 pagesSip ReportRosita JacobNo ratings yet

- Info On Nature Risks of InvestmentsDocument0 pagesInfo On Nature Risks of InvestmentsIndra PramanaNo ratings yet

- Chapter One Introduction To InvestmentDocument13 pagesChapter One Introduction To InvestmentAdugna KeneaNo ratings yet

- Chapter One Introduction To InvestmentDocument15 pagesChapter One Introduction To InvestmentHaileNo ratings yet

- Stock Market ConceptDocument16 pagesStock Market ConceptparamgkNo ratings yet

- Project On: Swaps-Structure, Irs and How To HedgingswapsDocument17 pagesProject On: Swaps-Structure, Irs and How To HedgingswapsanudonNo ratings yet

- Derivatives Are Financial Instruments RINUDocument13 pagesDerivatives Are Financial Instruments RINUkennyajay100% (2)

- Internet MarketingDocument62 pagesInternet MarketingVishal DhekaleNo ratings yet

- Adam Craig GilchristDocument4 pagesAdam Craig GilchristVishal DhekaleNo ratings yet

- Chris GayleDocument7 pagesChris GayleVishal DhekaleNo ratings yet

- Title Plant IndexingDocument1 pageTitle Plant IndexingVishal DhekaleNo ratings yet

- Pitra Dosha NivaranDocument4 pagesPitra Dosha NivaranVishal DhekaleNo ratings yet

- Real Estate Black BookDocument9 pagesReal Estate Black BookVishal Dhekale0% (2)

- Marcello MalpighiDocument2 pagesMarcello MalpighiVishal DhekaleNo ratings yet

- Homas Alva Edison: Early LifeDocument3 pagesHomas Alva Edison: Early LifeVishal DhekaleNo ratings yet

- Max Planck: Early LifeDocument2 pagesMax Planck: Early LifeVishal DhekaleNo ratings yet

- Paul Ehrlich: Early Life and EducationDocument2 pagesPaul Ehrlich: Early Life and EducationVishal DhekaleNo ratings yet

- J. J. Thomson: Beginnings: School and UniversityDocument8 pagesJ. J. Thomson: Beginnings: School and UniversityVishal DhekaleNo ratings yet

- Robert BunsenDocument9 pagesRobert BunsenVishal DhekaleNo ratings yet

- Brahma GuptaDocument3 pagesBrahma GuptaVishal DhekaleNo ratings yet

- Inge LehmannDocument8 pagesInge LehmannVishal DhekaleNo ratings yet

- ThalesDocument7 pagesThalesVishal DhekaleNo ratings yet

- Naresh Axis Bank ProjectDocument44 pagesNaresh Axis Bank ProjectRuppa_Rakesh_172167% (3)

- Proforma Affidavit App FormDocument9 pagesProforma Affidavit App Formsamplc2011No ratings yet

- Irr Republic Act 10951Document50 pagesIrr Republic Act 10951Anna Marie Dayanghirang100% (1)

- Articles of PartnershipDocument4 pagesArticles of PartnershipJuly Lumantas100% (1)

- ContractsDocument11 pagesContractsAtulNo ratings yet

- Secor Chrystal Jean E. Shareholders EquityDocument53 pagesSecor Chrystal Jean E. Shareholders EquityAbriel BumatayNo ratings yet

- SOCPA IFRS Transition ProjectDocument51 pagesSOCPA IFRS Transition ProjectArslan Zafar0% (1)

- Ravi Kishore BookDocument3 pagesRavi Kishore BookZeeshan Sikandar0% (1)

- Populi - John - Nouel - B. - AT2B.docx - Filename UTF-8''Populi, John Nouel B. AT2BDocument8 pagesPopuli - John - Nouel - B. - AT2B.docx - Filename UTF-8''Populi, John Nouel B. AT2BKindred WolfeNo ratings yet

- Comprehensive Course List: FitforbankingDocument13 pagesComprehensive Course List: FitforbankingLon NarothNo ratings yet

- Mauboussin - Employee Stock Options - Theory and Practice PDFDocument10 pagesMauboussin - Employee Stock Options - Theory and Practice PDFRob72081No ratings yet

- MCQ'sDocument14 pagesMCQ'sKawalpreet Singh Makkar71% (7)

- Agri As GDPDocument165 pagesAgri As GDPKrishna SinghNo ratings yet

- Bookkeeping: Bookkeeping Is The Recording of Financial Transactions. Transactions Include SalesDocument7 pagesBookkeeping: Bookkeeping Is The Recording of Financial Transactions. Transactions Include SalesCharlie True FriendNo ratings yet

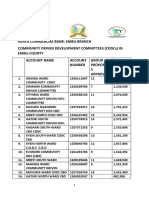

- Account Details For Cddcs & Pos-Dec 2019Document3 pagesAccount Details For Cddcs & Pos-Dec 2019Global ComputerNo ratings yet

- Algorithmic Trading & DMA: by Barry JohnsonDocument8 pagesAlgorithmic Trading & DMA: by Barry JohnsonRaghav ThaparNo ratings yet

- 9706 w17 QP 11Document11 pages9706 w17 QP 11Vinetha KarunanithiNo ratings yet

- Credit Risk Modelling - Facts, Theory and Applications (Terry Benzschawel) (Z-Library)Document1,624 pagesCredit Risk Modelling - Facts, Theory and Applications (Terry Benzschawel) (Z-Library)Anderson DuarteNo ratings yet

- Risk Management NotesDocument27 pagesRisk Management NoteskomalNo ratings yet

- Incidents in The Life of Negotiable InstrumentsDocument2 pagesIncidents in The Life of Negotiable InstrumentsMona Liza33% (3)

- Sri Lanka's No. 1 Brand BOC Dented by Bond ScamDocument8 pagesSri Lanka's No. 1 Brand BOC Dented by Bond ScamThavamNo ratings yet

- CFA Research Challenge Contestant PackDocument19 pagesCFA Research Challenge Contestant PackkevinNo ratings yet

- Adani EnterprisesDocument8 pagesAdani EnterprisesZAHIR ALAMNo ratings yet

- Mathematics of FinanceDocument22 pagesMathematics of FinanceKaren S. EsguerraNo ratings yet

- All-Time High Stocks - Why 52-Week and All-Time Highs OutperformDocument3 pagesAll-Time High Stocks - Why 52-Week and All-Time Highs Outperform_karr99100% (1)

- 3.vol 01 Issue 05 Lenin Kumar Cluster Analysis of Mutual FundsDocument24 pages3.vol 01 Issue 05 Lenin Kumar Cluster Analysis of Mutual FundsRaaj SinghNo ratings yet

- A Study On Credit Risk ManagementDocument44 pagesA Study On Credit Risk ManagementShabreen Sultana100% (1)

- Market Analysis Feb 2024Document17 pagesMarket Analysis Feb 2024Subba TNo ratings yet

- Business Plan ProposalDocument8 pagesBusiness Plan ProposalAirah Mondonedo100% (2)