You might also like

- Wendy's/Arby's (WEN), by William Ackman, Pershing Square Capital Management, May 2008Document31 pagesWendy's/Arby's (WEN), by William Ackman, Pershing Square Capital Management, May 2008The Manual of IdeasNo ratings yet

- PIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsFrom EverandPIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsNo ratings yet

- Bill Ackman Pershing Square Long StarbucksDocument43 pagesBill Ackman Pershing Square Long Starbucksmarketfolly.com100% (5)

- Financial Fine Print: Uncovering a Company's True ValueFrom EverandFinancial Fine Print: Uncovering a Company's True ValueRating: 3 out of 5 stars3/5 (3)

- ValueAct's Q1 2013 Letter and MSFT PresentationDocument34 pagesValueAct's Q1 2013 Letter and MSFT PresentationckgriffiNo ratings yet

- Loan Workouts and Debt for Equity Swaps: A Framework for Successful Corporate RescuesFrom EverandLoan Workouts and Debt for Equity Swaps: A Framework for Successful Corporate RescuesRating: 5 out of 5 stars5/5 (1)

- Cadbury Trian LetterDocument14 pagesCadbury Trian Letterbillroberts981No ratings yet

- Bill Ackman's Ira Sohn JCP PresentationDocument64 pagesBill Ackman's Ira Sohn JCP PresentationJohnCarney100% (1)

- Merger Arbitrage: A Fundamental Approach to Event-Driven InvestingFrom EverandMerger Arbitrage: A Fundamental Approach to Event-Driven InvestingRating: 5 out of 5 stars5/5 (1)

- Viking Form 2 ADVDocument36 pagesViking Form 2 ADVSOeNo ratings yet

- Competitive Advantage in Investing: Building Winning Professional PortfoliosFrom EverandCompetitive Advantage in Investing: Building Winning Professional PortfoliosNo ratings yet

- Bill Ackman Allergan PresentationDocument110 pagesBill Ackman Allergan PresentationCanadianValue100% (2)

- Active Alpha: A Portfolio Approach to Selecting and Managing Alternative InvestmentsFrom EverandActive Alpha: A Portfolio Approach to Selecting and Managing Alternative InvestmentsNo ratings yet

- Bill Ackman On What Makes A Great InvestmentDocument5 pagesBill Ackman On What Makes A Great InvestmentSww WisdomNo ratings yet

- Private Equity Unchained: Strategy Insights for the Institutional InvestorFrom EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNo ratings yet

- Pershing Square Second-Quarter Investor LetterDocument23 pagesPershing Square Second-Quarter Investor LetterNew York PostNo ratings yet

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsFrom EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsNo ratings yet

- Third Point Q3 2019 LetterDocument13 pagesThird Point Q3 2019 LetterZerohedge100% (2)

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketFrom EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketNo ratings yet

- Mark Yusko's Presentation at iCIO: Year of The AlligatorDocument123 pagesMark Yusko's Presentation at iCIO: Year of The AlligatorValueWalkNo ratings yet

- J-Curve Exposure: Managing a Portfolio of Venture Capital and Private Equity FundsFrom EverandJ-Curve Exposure: Managing a Portfolio of Venture Capital and Private Equity FundsRating: 4 out of 5 stars4/5 (1)

- Pershing Square Target Presentation 2008Document80 pagesPershing Square Target Presentation 2008goldan203454No ratings yet

- BBrief Six Degrees of Tiger Management 01 03 12Document11 pagesBBrief Six Degrees of Tiger Management 01 03 12Sarah RamirezNo ratings yet

- Investing in Junk Bonds: Inside the High Yield Debt MarketFrom EverandInvesting in Junk Bonds: Inside the High Yield Debt MarketRating: 3 out of 5 stars3/5 (1)

- Bill Ackman Ira Sohn Freddie Mac and Fannie Mae PresentationDocument111 pagesBill Ackman Ira Sohn Freddie Mac and Fannie Mae PresentationCanadianValueNo ratings yet

- Distressed Investment Banking - To the Abyss and Back - Second EditionFrom EverandDistressed Investment Banking - To the Abyss and Back - Second EditionNo ratings yet

- Elliott Management's BMC PresentationDocument36 pagesElliott Management's BMC PresentationDealBookNo ratings yet

- The Art of Vulture Investing: Adventures in Distressed Securities ManagementFrom EverandThe Art of Vulture Investing: Adventures in Distressed Securities ManagementNo ratings yet

- ThirdPoint Q1 16Document9 pagesThirdPoint Q1 16marketfolly.comNo ratings yet

- Tech Stock Valuation: Investor Psychology and Economic AnalysisFrom EverandTech Stock Valuation: Investor Psychology and Economic AnalysisRating: 4 out of 5 stars4/5 (1)

- Third Point Investor PresentationDocument29 pagesThird Point Investor PresentationValueWalkNo ratings yet

- Pershing Square European Investor Meeting PresentationDocument67 pagesPershing Square European Investor Meeting Presentationmarketfolly.com100% (1)

- Starboard Value LP AAP Presentation 09.30.15Document23 pagesStarboard Value LP AAP Presentation 09.30.15marketfolly.com100% (1)

- Guaranteed to Fail: Fannie Mae, Freddie Mac, and the Debacle of Mortgage FinanceFrom EverandGuaranteed to Fail: Fannie Mae, Freddie Mac, and the Debacle of Mortgage FinanceRating: 2 out of 5 stars2/5 (1)

- Atticus Global Letter To InvestorsDocument2 pagesAtticus Global Letter To InvestorsDealBookNo ratings yet

- Distress Investing: Principles and TechniqueFrom EverandDistress Investing: Principles and TechniqueRating: 4 out of 5 stars4/5 (5)

- Arlington Value's 2013 LetterDocument7 pagesArlington Value's 2013 LetterValueWalk100% (7)

- Buyouts: Success for Owners, Management, PEGs, ESOPs and Mergers and AcquisitionsFrom EverandBuyouts: Success for Owners, Management, PEGs, ESOPs and Mergers and AcquisitionsNo ratings yet

- Graham Doddsville Spring 2016Document54 pagesGraham Doddsville Spring 2016marketfolly.comNo ratings yet

- Roe To CfroiDocument30 pagesRoe To CfroiSyifa034No ratings yet

- Seth Klarman Views (24 PGS) June 2013Document24 pagesSeth Klarman Views (24 PGS) June 2013kumarp13No ratings yet

- Fixed Income Relative Value Analysis: A Practitioners Guide to the Theory, Tools, and TradesFrom EverandFixed Income Relative Value Analysis: A Practitioners Guide to the Theory, Tools, and TradesNo ratings yet

- Seth Klarman's Baupost Fund Semi-Annual Report 19991Document24 pagesSeth Klarman's Baupost Fund Semi-Annual Report 19991nabsNo ratings yet

- Diary of a Very Bad Year: Interviews with an Anonymous Hedge Fund ManagerFrom EverandDiary of a Very Bad Year: Interviews with an Anonymous Hedge Fund ManagerRating: 4 out of 5 stars4/5 (17)

- Scion 2006 4q Rmbs Cds Primer and FaqDocument8 pagesScion 2006 4q Rmbs Cds Primer and FaqsabishiiNo ratings yet

- GGP Ackman Presentation Ira Sohn Conf 5-26-10Document89 pagesGGP Ackman Presentation Ira Sohn Conf 5-26-10fstreet100% (2)

- Sequoia Ann 14Document36 pagesSequoia Ann 14CanadianValueNo ratings yet

- Li Lu's 2010 Lecture at Columbia My Previous Transcript View A More Recent LectureDocument14 pagesLi Lu's 2010 Lecture at Columbia My Previous Transcript View A More Recent Lecturepa_langstrom100% (1)

- Bill Ackman Case Study of GGP - Incentives Matter - Value Investing Congress - 10.1Document102 pagesBill Ackman Case Study of GGP - Incentives Matter - Value Investing Congress - 10.1Caleb Peter Hobart100% (1)

- Arlington Value 2006 Annual Shareholder LetterDocument5 pagesArlington Value 2006 Annual Shareholder LetterSmitty WNo ratings yet

- Wolf Bytes 20: Equity Research-AmericasDocument20 pagesWolf Bytes 20: Equity Research-Americasvouzvouz7127No ratings yet

- Icahn LetterDocument3 pagesIcahn Lettergrw7No ratings yet

- Letter About Carl IcahnDocument4 pagesLetter About Carl IcahnCNBC.com100% (1)

- Stan Druckenmiller The Endgame SohnDocument10 pagesStan Druckenmiller The Endgame SohnCanadianValueNo ratings yet

- Charlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFDocument18 pagesCharlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFaakashshah85No ratings yet

- Stan Druckenmiller Sohn TranscriptDocument8 pagesStan Druckenmiller Sohn Transcriptmarketfolly.com100% (1)

- Greenlight UnlockedDocument7 pagesGreenlight UnlockedZerohedgeNo ratings yet

- KaseFundannualletter 2015Document20 pagesKaseFundannualletter 2015CanadianValueNo ratings yet

- Hussman Funds Semi-Annual ReportDocument84 pagesHussman Funds Semi-Annual ReportCanadianValueNo ratings yet

- The Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500Document6 pagesThe Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500dpbasicNo ratings yet

- Whitney Tilson Favorite Long and Short IdeasDocument103 pagesWhitney Tilson Favorite Long and Short IdeasCanadianValueNo ratings yet

- Munger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16Document12 pagesMunger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16CanadianValueNo ratings yet

- OakTree Real EstateDocument13 pagesOakTree Real EstateCanadianValue100% (1)

- Market Macro Myths Debts Deficits and DelusionsDocument13 pagesMarket Macro Myths Debts Deficits and DelusionsCanadianValueNo ratings yet

- Einhorn Q4 2015Document7 pagesEinhorn Q4 2015CanadianValueNo ratings yet

- Einhorn Consol PresentationDocument107 pagesEinhorn Consol PresentationCanadianValueNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Investor Call Re Valeant PharmaceuticalsDocument39 pagesInvestor Call Re Valeant PharmaceuticalsCanadianValueNo ratings yet

- Letter To Clients and ShareholdersDocument3 pagesLetter To Clients and ShareholdersJulia Reynolds La RocheNo ratings yet

- Starboard Value LP AAP Presentation 09.30.15Document23 pagesStarboard Value LP AAP Presentation 09.30.15marketfolly.com100% (1)

- Absolute Return Oct 2015Document9 pagesAbsolute Return Oct 2015CanadianValue0% (1)

- Mortgages 2019Document60 pagesMortgages 2019Ivana JayNo ratings yet

- Blue Chip Stocks TipsDocument16 pagesBlue Chip Stocks TipsPinal MehtaNo ratings yet

- Co Operative Housing SocietyDocument29 pagesCo Operative Housing Societyvenkynaidu100% (1)

- Indzara Personal Finance Manager 2010 v2Document8 pagesIndzara Personal Finance Manager 2010 v2AlexandruDanielNo ratings yet

- Nmims SBM Mumbai Final Placement Report 2016Document8 pagesNmims SBM Mumbai Final Placement Report 2016IshaanVijaywargiyaNo ratings yet

- EcsmformDocument1 pageEcsmform0sandeepNo ratings yet

- Class Notes On Income Tax On CorporationsDocument3 pagesClass Notes On Income Tax On CorporationsJeremie R. PlazaNo ratings yet

- Account Closure Form Citi BankDocument1 pageAccount Closure Form Citi BankSarfaraz AhmedNo ratings yet

- App Aud - Prelim Exam (Key)Document16 pagesApp Aud - Prelim Exam (Key)Shaina Kaye De GuzmanNo ratings yet

- 2551QDocument3 pages2551QJerry Bantilan JrNo ratings yet

- Kantox FX Guide For CFODocument20 pagesKantox FX Guide For CFOfcatalaoNo ratings yet

- Fin MarDocument2 pagesFin MarKoleen Mae LindayenNo ratings yet

- CIF vs. FOB - What's The DifferenceDocument8 pagesCIF vs. FOB - What's The DifferenceCHAITANYANo ratings yet

- (On The Letterhead of The Bidder/CONSULTANT) : Format For Advice of Vendor DetailsDocument2 pages(On The Letterhead of The Bidder/CONSULTANT) : Format For Advice of Vendor DetailsNinad SherawalaNo ratings yet

- Alpha PDFDocument13 pagesAlpha PDFWARWICKJNo ratings yet

- Instrumentation Experts Club Individual Membership Registration FormDocument1 pageInstrumentation Experts Club Individual Membership Registration FormSanjay SoniNo ratings yet

- Notice: Banks and Bank Holding Companies: Formations, Acquisitions, and MergersDocument1 pageNotice: Banks and Bank Holding Companies: Formations, Acquisitions, and MergersJustia.comNo ratings yet

- Submitted To:-Ms - Priya Singh Chauhan: Topic: - Analysis On Administrative Regulation On Corporate Finance in IndiaDocument10 pagesSubmitted To:-Ms - Priya Singh Chauhan: Topic: - Analysis On Administrative Regulation On Corporate Finance in IndiaharshNo ratings yet

- THE OF Outsourcing: J U N e 2 0 0 8Document60 pagesTHE OF Outsourcing: J U N e 2 0 0 8kamaraniNo ratings yet

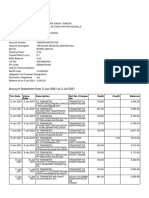

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- Project by Vidhi Seth and Nandini KediaDocument19 pagesProject by Vidhi Seth and Nandini KediavidhisethNo ratings yet

- PESONet ParticipantsDocument2 pagesPESONet ParticipantsKylene Maranan VillamarNo ratings yet

- Problem 01 Answer KeyDocument6 pagesProblem 01 Answer KeyAngelito Eclipse100% (5)

- Nmims Final Report123 PDFDocument46 pagesNmims Final Report123 PDFHimanshu KhandelwalNo ratings yet

- IIF ReportDocument152 pagesIIF ReportJuan Manuel Lopez LeonNo ratings yet

- A Dishonest Client Will Get The Best ofDocument1 pageA Dishonest Client Will Get The Best ofrewasNo ratings yet

- The Role of Ceo in The Strategic PlanningDocument18 pagesThe Role of Ceo in The Strategic PlanningmanofhonourNo ratings yet

- FYP Risk Management HDFC SecuritiesDocument82 pagesFYP Risk Management HDFC Securitiespadmakar_rajNo ratings yet

- 2016 2017 PDFDocument44 pages2016 2017 PDFHay Jirenyaa100% (1)

- 2.3 Audit AssuranceDocument27 pages2.3 Audit AssurancemohedNo ratings yet

- Dear Chairman: Boardroom Battles and the Rise of Shareholder ActivismFrom EverandDear Chairman: Boardroom Battles and the Rise of Shareholder ActivismRating: 4 out of 5 stars4/5 (15)

- Achieving Post-Merger Success: A Stakeholder's Guide to Cultural Due Diligence, Assessment, and IntegrationFrom EverandAchieving Post-Merger Success: A Stakeholder's Guide to Cultural Due Diligence, Assessment, and IntegrationNo ratings yet

- Guns Galore!: How to Buy and Sell Guns, Knives, and Ammo in Online Auctions Easily Without eBay!From EverandGuns Galore!: How to Buy and Sell Guns, Knives, and Ammo in Online Auctions Easily Without eBay!No ratings yet

- Inside CEO Succession: The Essential Guide to Leadership TransitionFrom EverandInside CEO Succession: The Essential Guide to Leadership TransitionNo ratings yet

- The Nonprofit Board Answer Book: A Practical Guide for Board Members and Chief ExecutivesFrom EverandThe Nonprofit Board Answer Book: A Practical Guide for Board Members and Chief ExecutivesRating: 4 out of 5 stars4/5 (1)

- 2017 Guide to Buying and Selling Antiques and Collectables, Critical “Dos” and “Don’ts” for your antiques and collectables retail businessFrom Everand2017 Guide to Buying and Selling Antiques and Collectables, Critical “Dos” and “Don’ts” for your antiques and collectables retail businessNo ratings yet

- How to Sell on Amazon: Step by Step Guide to Making Money Consistently and Build a Profitable Business with AmazonFrom EverandHow to Sell on Amazon: Step by Step Guide to Making Money Consistently and Build a Profitable Business with AmazonNo ratings yet

- Model Policies and Procedures for Not-for-Profit OrganizationsFrom EverandModel Policies and Procedures for Not-for-Profit OrganizationsNo ratings yet

- The Public Company Handbook: A Corporate Governance and Disclosure Guide for Directors and ExecutivesFrom EverandThe Public Company Handbook: A Corporate Governance and Disclosure Guide for Directors and ExecutivesNo ratings yet

- Take the Lead: Motivate, Inspire, and Bring Out the Best in Yourself and Everyone Around YouFrom EverandTake the Lead: Motivate, Inspire, and Bring Out the Best in Yourself and Everyone Around YouRating: 3.5 out of 5 stars3.5/5 (4)

- Alliances: An Executive Guide to Designing Successful Strategic PartnershipsFrom EverandAlliances: An Executive Guide to Designing Successful Strategic PartnershipsNo ratings yet

- Who Is In Your Personal Boardroom? How to Choose People, Assign Roles and Have Conversations With PurposeFrom EverandWho Is In Your Personal Boardroom? How to Choose People, Assign Roles and Have Conversations With PurposeNo ratings yet

- The Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board MembersFrom EverandThe Handbook of Board Governance: A Comprehensive Guide for Public, Private, and Not-for-Profit Board MembersNo ratings yet

- The $12 Million Stuffed Shark: The Curious Economics of Contemporary ArtFrom EverandThe $12 Million Stuffed Shark: The Curious Economics of Contemporary ArtRating: 4 out of 5 stars4/5 (9)

- CEO Leadership: Navigating the New Era in Corporate GovernanceFrom EverandCEO Leadership: Navigating the New Era in Corporate GovernanceNo ratings yet

- Corporate Governance Best Practices: Strategies for Public, Private, and Not-for-Profit OrganizationsFrom EverandCorporate Governance Best Practices: Strategies for Public, Private, and Not-for-Profit OrganizationsNo ratings yet

- Startup Boards: Getting the Most Out of Your Board of DirectorsFrom EverandStartup Boards: Getting the Most Out of Your Board of DirectorsRating: 4 out of 5 stars4/5 (5)

- Corporate Boards That Create Value: Governing Company Performance from the BoardroomFrom EverandCorporate Boards That Create Value: Governing Company Performance from the BoardroomRating: 4 out of 5 stars4/5 (1)

- Money on the Table: How to Increase Profits through Gender-Balanced LeadershipFrom EverandMoney on the Table: How to Increase Profits through Gender-Balanced LeadershipNo ratings yet