You might also like

- Legal Forms Reviewer.Document18 pagesLegal Forms Reviewer.Jerry Kho100% (1)

- 7.4.14 Red Notes TaxDocument41 pages7.4.14 Red Notes TaxRey Jan N. VillavicencioNo ratings yet

- How To Beat Criminal Charges in Admiralty Courts PDFDocument8 pagesHow To Beat Criminal Charges in Admiralty Courts PDFThomas Bull Rearden100% (3)

- Checklist - Worker's Compensation ClaimsDocument8 pagesChecklist - Worker's Compensation Claimsmsmt1210No ratings yet

- Letter of Intent For Joint VentureDocument10 pagesLetter of Intent For Joint VentureKelvin Kamalata100% (2)

- Cost Accounting Theory NotesDocument41 pagesCost Accounting Theory NotesShrividhya Venkata Prasath83% (6)

- Far 09 Government GrantsDocument9 pagesFar 09 Government GrantsJoshua UmaliNo ratings yet

- Lyari Expressway Rehabilitation ProjectDocument32 pagesLyari Expressway Rehabilitation ProjectKamran KhanNo ratings yet

- BR100 OPM Inventory Application SetupDocument43 pagesBR100 OPM Inventory Application Setupghazouani100% (1)

- May 2017 Advanced Financial Accounting & Reporting Final Pre-BoardDocument20 pagesMay 2017 Advanced Financial Accounting & Reporting Final Pre-BoardPatrick ArazoNo ratings yet

- Presented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019Document2 pagesPresented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019SalsabiilaNo ratings yet

- ACC107 P1 EXAM With Key AnswerDocument9 pagesACC107 P1 EXAM With Key AnswerRyan Malanum AbrioNo ratings yet

- Auditing Problems Audit of Inventory: Problem 1Document6 pagesAuditing Problems Audit of Inventory: Problem 1Mark Anthony TibuleNo ratings yet

- National Minorities Development & Finance Corporaiton: NMDFCDocument9 pagesNational Minorities Development & Finance Corporaiton: NMDFCMunish KharbNo ratings yet

- Estt Rule No. 39/2011Document2 pagesEstt Rule No. 39/2011msnhot40No ratings yet

- Plan Conturi 2013Document15 pagesPlan Conturi 2013Monica MarinNo ratings yet

- HDFC Bank Home LoanDocument30 pagesHDFC Bank Home LoanMark MurphyNo ratings yet

- MEO Class-IV Assesment ChecklistDocument1 pageMEO Class-IV Assesment ChecklistSouvik SamantaNo ratings yet

- Plan Conturi 2014Document13 pagesPlan Conturi 2014Daniela MunteanuNo ratings yet

- Plan Conturi 2013Document15 pagesPlan Conturi 2013tomyclauNo ratings yet

- Section-IV Qualification CriteriaDocument6 pagesSection-IV Qualification CriteriaYohannes GebreNo ratings yet

- Bus 82-201 Summer 2014 SyllabusDocument13 pagesBus 82-201 Summer 2014 SyllabusBoss BallaNo ratings yet

- Plan Conturi 2013Document16 pagesPlan Conturi 2013Diana BaicanNo ratings yet

- C R E A: Ochin Efineries Mployees' Ssociatio N Reg - No.120/67, Ambalamugal, Kochi - 682 302Document3 pagesC R E A: Ochin Efineries Mployees' Ssociatio N Reg - No.120/67, Ambalamugal, Kochi - 682 302erppibuNo ratings yet

- Plan Conturi 2013Document15 pagesPlan Conturi 2013Dana TeleagaNo ratings yet

- BM 850 Revised Rules On MCLEDocument12 pagesBM 850 Revised Rules On MCLElarrybirdyNo ratings yet

- Consultant Non-Disclosure AgreementDocument3 pagesConsultant Non-Disclosure AgreementMuhamad AziziNo ratings yet

- Domain Name Registration AgreementDocument4 pagesDomain Name Registration AgreementMuhamad AziziNo ratings yet

- 2013 Statement of Complaince - Doc (For Ann. Cert.)Document4 pages2013 Statement of Complaince - Doc (For Ann. Cert.)Federal Communications Commission (FCC)No ratings yet

- Important: If Payment Is Being Made by A Company Cheque or Credit Card Please Tick Here and Provide Full Company Name & Address OverleafDocument8 pagesImportant: If Payment Is Being Made by A Company Cheque or Credit Card Please Tick Here and Provide Full Company Name & Address Overleaft.mohammedNo ratings yet

- Conditions of Contract: 1.-Confirmation and PaymentDocument1 pageConditions of Contract: 1.-Confirmation and PaymentAlexander Davalos ValenzuelaNo ratings yet

- New Contractor'S License Application: Required Items Complied Yes No NADocument23 pagesNew Contractor'S License Application: Required Items Complied Yes No NAsharmine_ruizNo ratings yet

- 1.garcia Vs SSSDocument20 pages1.garcia Vs SSSLexter CruzNo ratings yet

- Please Complete ALL Sections of This Form.: Recruitment, PLUS, 8 Celbridge Mews, London, W2 6EU. Fax: +44 20 7792 8717Document3 pagesPlease Complete ALL Sections of This Form.: Recruitment, PLUS, 8 Celbridge Mews, London, W2 6EU. Fax: +44 20 7792 8717Cô SúpNo ratings yet

- Teacher of ArtDocument10 pagesTeacher of ArtChrist's SchoolNo ratings yet

- Petty Cash VoucherDocument2 pagesPetty Cash Vouchersaneesh81No ratings yet

- SathishDocument3 pagesSathishAmanda PriceNo ratings yet

- Pres IssuancesDocument8 pagesPres IssuancesZan BillonesNo ratings yet

- Plan Conturi 2013Document12 pagesPlan Conturi 2013Calin BocaNo ratings yet

- Acsi Cpni Cert 2013Document3 pagesAcsi Cpni Cert 2013Federal Communications Commission (FCC)No ratings yet

- BPI VsDocument2 pagesBPI VsHao Wei WeiNo ratings yet

- Cir Vs Sony Philippines Inc (GR 178697 November 17 2010)Document11 pagesCir Vs Sony Philippines Inc (GR 178697 November 17 2010)Brian BaldwinNo ratings yet

- Si... Ock Entry Form 2014 PDFDocument2 pagesSi... Ock Entry Form 2014 PDFTomato WiFiNo ratings yet

- AsdjiosdDocument15 pagesAsdjiosddawn.devNo ratings yet

- Concept of IncomeDocument12 pagesConcept of IncomeCara HenaresNo ratings yet

- Oral Postal DetailsDocument5 pagesOral Postal DetailsMahesh BabuNo ratings yet

- IT-2 TY-2013 Without Formula - 2013Document12 pagesIT-2 TY-2013 Without Formula - 2013Muhammad TausifNo ratings yet

- Application Form For Diploma Courses 2013-14 NewDocument4 pagesApplication Form For Diploma Courses 2013-14 NewogakhanNo ratings yet

- BPPM FulltextDocument673 pagesBPPM FulltextAhmad Fauzi MehatNo ratings yet

- 1.0 Purpose: Surveys and InspectionDocument33 pages1.0 Purpose: Surveys and InspectionKr ManuNo ratings yet

- Accounting Group Study 1Document13 pagesAccounting Group Study 1ahmustNo ratings yet

- 1. Proposal for Services - ThảoDocument3 pages1. Proposal for Services - ThảoThao NguyenNo ratings yet

- Takeover CodeDocument25 pagesTakeover CodejoshitejasNo ratings yet

- Sca Labour Drafting 1Document24 pagesSca Labour Drafting 1Sunil LodhaNo ratings yet

- Minor Project Report Final (Diploma Xyz)Document53 pagesMinor Project Report Final (Diploma Xyz)Jigar ShahNo ratings yet

- Essay On The Next Global StageDocument16 pagesEssay On The Next Global StageEsteban JacksonNo ratings yet

- Individual Charge Account DenialDocument2 pagesIndividual Charge Account DenialtewngomNo ratings yet

- Orld Rade Rganization: United States - Continued Suspension of Obligations in The Ec - Hormones DisputeDocument65 pagesOrld Rade Rganization: United States - Continued Suspension of Obligations in The Ec - Hormones DisputeFadlul Akbar HerfiantoNo ratings yet

- Plan Conturi 2013Document9 pagesPlan Conturi 2013Neacsu AndreeaNo ratings yet

- Office of The Principal, RTTC, BHUBANESWAR-751007. (An ISO:9001:2008 Certified Institute)Document1 pageOffice of The Principal, RTTC, BHUBANESWAR-751007. (An ISO:9001:2008 Certified Institute)sukujeNo ratings yet

- Subject: Date: - CP No.Document12 pagesSubject: Date: - CP No.S Kalu SivalingamNo ratings yet

- Divided States: Strategic Divisions in EU-Russia RelationsFrom EverandDivided States: Strategic Divisions in EU-Russia RelationsNo ratings yet

- The Global Player: How to become "the logistics company for the world"From EverandThe Global Player: How to become "the logistics company for the world"No ratings yet

- ACCCOB1 Quiz 1 Monday Set A Answer Key PDFDocument4 pagesACCCOB1 Quiz 1 Monday Set A Answer Key PDFfanchasticommsNo ratings yet

- This Study Resource Was: Problem 1-PatentDocument6 pagesThis Study Resource Was: Problem 1-PatentJan JanNo ratings yet

- First Solar, Inc. (FSLR) : 3 - NeutralDocument6 pagesFirst Solar, Inc. (FSLR) : 3 - NeutralCarlos TresemeNo ratings yet

- Review of Related Literature and StudiesDocument10 pagesReview of Related Literature and StudiesJaira May BustardeNo ratings yet

- Using General LedgerDocument376 pagesUsing General LedgerarvindappNo ratings yet

- Terminal Sample 2 UnsolvedDocument7 pagesTerminal Sample 2 UnsolvedFami FamzNo ratings yet

- CH 2 Cost Concepts and BehaviorDocument37 pagesCH 2 Cost Concepts and BehaviorRexmar Christian BernardoNo ratings yet

- Introduction of AccountingDocument23 pagesIntroduction of AccountingOnse AlaxusNo ratings yet

- The Audit Standards' Setting ProcessDocument36 pagesThe Audit Standards' Setting Processahmad fikriNo ratings yet

- Continuous Auditing and Risk-Based Audit PlanningDocument29 pagesContinuous Auditing and Risk-Based Audit PlanningFulky HNo ratings yet

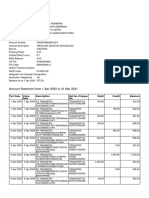

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNo ratings yet

- BKAF3073 Chapter 1Document53 pagesBKAF3073 Chapter 1Shahrul IzwanNo ratings yet

- Listado 22Document1,047 pagesListado 22HéctorValleNo ratings yet

- Name: Muhyideen Abdulganiyu Wallet Number: 8180955581Document2 pagesName: Muhyideen Abdulganiyu Wallet Number: 8180955581abubakarameenuabdulkadirNo ratings yet

- Week 6 7 ULOa Lets Check and Lets AnalyzeDocument4 pagesWeek 6 7 ULOa Lets Check and Lets Analyzeemem resuentoNo ratings yet

- PT Test Questions IcaiDocument66 pagesPT Test Questions IcaiRS Desai67% (3)

- Zoom Febrero 2016 PDFDocument1 pageZoom Febrero 2016 PDFjuanluismegaNo ratings yet

- Boynton SM Ch.07Document17 pagesBoynton SM Ch.07Eza R100% (2)

- 2012-2013 Scholarship Application 2-Year and Undergraduate Scholarships DUE March 1, 2012 To The ChapterDocument3 pages2012-2013 Scholarship Application 2-Year and Undergraduate Scholarships DUE March 1, 2012 To The ChapterrebbeccafentonNo ratings yet

- Rekening Koran Bulan Mei Juli 2023Document3 pagesRekening Koran Bulan Mei Juli 2023Panji PrakosoNo ratings yet

- HahahDocument13 pagesHahahSuzaka - ChanNo ratings yet

- 247806Document51 pages247806Jack ToutNo ratings yet

- Bkas 2013 - Revision Set Suggested SolutionDocument8 pagesBkas 2013 - Revision Set Suggested SolutionsyuhunniepieNo ratings yet

- Ifsa Chapter14Document34 pagesIfsa Chapter14Nageswara KorrakutiNo ratings yet