You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Real Estate Securitization Exam NotesDocument33 pagesReal Estate Securitization Exam NotesHeng Kai Li100% (1)

- Ecos3003 Final ReviewDocument30 pagesEcos3003 Final Reviewapi-255740189100% (2)

- fn3092 Hillier Textbook SolutionsDocument169 pagesfn3092 Hillier Textbook SolutionsAmine IzamNo ratings yet

- The Next 200 Years PDFDocument258 pagesThe Next 200 Years PDFkunalwarwickNo ratings yet

- (JP Morgan) All You Ever Wanted To Know About Corporate Hybrids But Were Afraid To AskDocument20 pages(JP Morgan) All You Ever Wanted To Know About Corporate Hybrids But Were Afraid To Ask00aa100% (2)

- Bill Ackman's Presentation On Ratings AgenciesDocument12 pagesBill Ackman's Presentation On Ratings AgenciesDealBook100% (1)

- X 70 15 PDFDocument32 pagesX 70 15 PDFkunalwarwickNo ratings yet

- Yale Som View BookDocument36 pagesYale Som View BookkunalwarwickNo ratings yet

- WatsonPaths - Scenario-basedQuestionAnsweringand Inference Over Unstructured InformationDocument20 pagesWatsonPaths - Scenario-basedQuestionAnsweringand Inference Over Unstructured InformationkunalwarwickNo ratings yet

- Music in The Air - Stairway To HeavenDocument3 pagesMusic in The Air - Stairway To Heavenkunalwarwick0% (1)

- TAP Press Release 01-30-2017Document2 pagesTAP Press Release 01-30-2017kunalwarwickNo ratings yet

- The Next 200 YearsDocument258 pagesThe Next 200 Yearskunalwarwick100% (1)

- NFLX EarningsMiss NoSurpise2015!10!20Document5 pagesNFLX EarningsMiss NoSurpise2015!10!20kunalwarwickNo ratings yet

- Clausing Profit ShiftingDocument32 pagesClausing Profit ShiftingkunalwarwickNo ratings yet

- UBS 2015 Final Final WithNotesDocument148 pagesUBS 2015 Final Final WithNoteskunalwarwickNo ratings yet

- Baker Vertical MergersDocument7 pagesBaker Vertical MergerskunalwarwickNo ratings yet

- Safaricom Feasibility StudyDocument11 pagesSafaricom Feasibility StudykunalwarwickNo ratings yet

- AOL Transcript 2015 05 08T12 00Document19 pagesAOL Transcript 2015 05 08T12 00kunalwarwickNo ratings yet

- Q1 2015 AOL Trending SchedulesDocument4 pagesQ1 2015 AOL Trending ScheduleskunalwarwickNo ratings yet

- Slides Machine Learning and EconometricsDocument44 pagesSlides Machine Learning and EconometricsdiocerNo ratings yet

- Fiscal Policy Nov 2013 FINALDocument7 pagesFiscal Policy Nov 2013 FINALkunalwarwickNo ratings yet

- CMBS 101 Slides (All Sessions)Document41 pagesCMBS 101 Slides (All Sessions)Ken KimNo ratings yet

- 247 Customer Private LimitedDocument7 pages247 Customer Private Limitednayabrasul208No ratings yet

- Amman TRY Sponge and Power Private LimitedDocument4 pagesAmman TRY Sponge and Power Private LimitedKathiresan Mathavi's SonNo ratings yet

- Accounting Theory Handout 1Document43 pagesAccounting Theory Handout 1Ockouri Barnes100% (3)

- Credit RatingDocument50 pagesCredit Ratingmaruf_tanmimNo ratings yet

- CREDIT RATING OF MSMEsDocument16 pagesCREDIT RATING OF MSMEsGaurav KumarNo ratings yet

- 13 QuestionnaireDocument9 pages13 QuestionnaireRahul SNo ratings yet

- 9.15 PNBPerpetual PDFDocument81 pages9.15 PNBPerpetual PDFAbhishekNo ratings yet

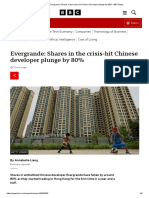

- Evergrande - Shares in The Crisis-Hit Chinese Developer Plunge by 80% - BBC NewsDocument9 pagesEvergrande - Shares in The Crisis-Hit Chinese Developer Plunge by 80% - BBC NewsBookratNo ratings yet

- 7Document22 pages7Sanket MhetreNo ratings yet

- Press Release Saksoft Limited: Details of Instruments/facilities in Annexure-1Document5 pagesPress Release Saksoft Limited: Details of Instruments/facilities in Annexure-1Sandy SanNo ratings yet

- V1. Loan - Application - Form - LoU-18.09.2020Document8 pagesV1. Loan - Application - Form - LoU-18.09.2020Aqueel HusainNo ratings yet

- Corporate Governance: By: 1. Kenneth A. Kim John R. Nofsinger and 2. A. C. FernandoDocument19 pagesCorporate Governance: By: 1. Kenneth A. Kim John R. Nofsinger and 2. A. C. FernandoMaryam MalikNo ratings yet

- Public BankDocument4 pagesPublic BankKhairul AslamNo ratings yet

- AFME Guide To Infrastructure FinancingDocument99 pagesAFME Guide To Infrastructure Financingfunction_analysisNo ratings yet

- Bac310 Lecture MaterialsDocument120 pagesBac310 Lecture MaterialsNdung'u Wa MumbiNo ratings yet

- 2012 Registration DocumentDocument552 pages2012 Registration DocumentMohammed YassinNo ratings yet

- Debentures Information MemorandumDocument61 pagesDebentures Information MemorandumakhilNo ratings yet

- BIBA Apparels Private - R - 22022019Document7 pagesBIBA Apparels Private - R - 22022019swapnil solankiNo ratings yet

- The Government Tele Communication R 03102017Document7 pagesThe Government Tele Communication R 03102017SandeeploguNo ratings yet

- Week 4 PDFDocument30 pagesWeek 4 PDFJohnLuceNo ratings yet

- Financial Credit Score: A Model For Rating Non-Convertible DebenturesDocument31 pagesFinancial Credit Score: A Model For Rating Non-Convertible DebenturesBhavesh AgarwalNo ratings yet

- Agency Problems in Corporate GovernanceDocument112 pagesAgency Problems in Corporate GovernanceFELIPE SORIANONo ratings yet

- Moody's Afirmó La Calificación B2 de Argentina y Bajó Su Perspectiva A NegativaDocument6 pagesMoody's Afirmó La Calificación B2 de Argentina y Bajó Su Perspectiva A NegativaCronista.comNo ratings yet