You might also like

- Financial Forecasting: SIFE Lakehead 2009Document7 pagesFinancial Forecasting: SIFE Lakehead 2009Marius AngaraNo ratings yet

- Financial Statements, Cash Flows, and TaxesDocument31 pagesFinancial Statements, Cash Flows, and Taxesjoanabud100% (1)

- Financial Statements, Cash Flow, and TaxesDocument43 pagesFinancial Statements, Cash Flow, and TaxesshimulNo ratings yet

- Parcor 003Document26 pagesParcor 003Vincent Larrie MoldezNo ratings yet

- Investment VI FINC 404 Company ValuationDocument52 pagesInvestment VI FINC 404 Company ValuationMohamed MadyNo ratings yet

- Introduction To Corporate Finance: Mcgraw-Hill/IrwinDocument105 pagesIntroduction To Corporate Finance: Mcgraw-Hill/IrwinVKrishna Kilaru100% (2)

- Financial Statements and Financial AnalysisDocument17 pagesFinancial Statements and Financial AnalysisVaibhav MahajanNo ratings yet

- Financial Analysis - Molycorp, Inc. Produces Rare Earth Minerals. the Company Produces Rare Earth Products, Including Oxides, Metals, Alloys and Magnets for a Variety of Applications Including Clean Energy TechnologiesDocument8 pagesFinancial Analysis - Molycorp, Inc. Produces Rare Earth Minerals. the Company Produces Rare Earth Products, Including Oxides, Metals, Alloys and Magnets for a Variety of Applications Including Clean Energy TechnologiesQ.M.S Advisors LLCNo ratings yet

- Investment Analysis and Portfolio Management 2012Document61 pagesInvestment Analysis and Portfolio Management 2012Nelson Ivan Acosta100% (1)

- CH 02Document30 pagesCH 02AhsanNo ratings yet

- NOPAT NOPAT2011 - NOPAT20010 (Note ' MeansDocument5 pagesNOPAT NOPAT2011 - NOPAT20010 (Note ' MeansBryan LluismaNo ratings yet

- Corporate Finance 3rd Edition Graham Solution ManualDocument15 pagesCorporate Finance 3rd Edition Graham Solution ManualMark PanchitoNo ratings yet

- Concepts Review and Critical Thinking Questions 4Document6 pagesConcepts Review and Critical Thinking Questions 4fnrbhcNo ratings yet

- Accounting For Manufacturing ActivitiesDocument27 pagesAccounting For Manufacturing ActivitiesGerald B. Garcia100% (2)

- 35 Basic Accounting Test QuestionsDocument9 pages35 Basic Accounting Test QuestionsDenny OctavianoNo ratings yet

- ch02 Financial Statement, Cash Flows and TaxesDocument30 pagesch02 Financial Statement, Cash Flows and TaxesAffan AhmedNo ratings yet

- Financial Management 2 - BirminghamDocument21 pagesFinancial Management 2 - BirminghamsimuragejayanNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument29 pagesFinancial Statements, Cash Flow, and TaxesHooriaKhanNo ratings yet

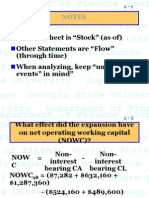

- Balance Sheet Is "Stock" (As Of) Other Statements Are "Flow" (Through Time) When Analyzing, Keep "Unusual Events" in Mind"Document22 pagesBalance Sheet Is "Stock" (As Of) Other Statements Are "Flow" (Through Time) When Analyzing, Keep "Unusual Events" in Mind"kegnataNo ratings yet

- CH #3Document7 pagesCH #3Waleed Ayaz UtmanzaiNo ratings yet

- CH 3 - Financial Statements, Cash FlowDocument48 pagesCH 3 - Financial Statements, Cash Flowssierras1No ratings yet

- Chapter 2 Buiness FinanxceDocument38 pagesChapter 2 Buiness FinanxceShajeer HamNo ratings yet

- Chapter 03 PenDocument27 pagesChapter 03 PenJeffreyDavidNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument36 pagesFinancial Statements, Cash Flow, and TaxesHussainNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument40 pagesFinancial Statements, Cash Flow, and TaxesKamran Ali AnsariNo ratings yet

- Chapter 03Document29 pagesChapter 03andi.w.rahardjoNo ratings yet

- Financial Statements, Taxes, and Cash Flows: Mcgraw-Hill/IrwinDocument24 pagesFinancial Statements, Taxes, and Cash Flows: Mcgraw-Hill/IrwinMd Musa PatoaryNo ratings yet

- Accounting For Financial ManagementDocument42 pagesAccounting For Financial ManagementTIDURLANo ratings yet

- EFM2e, CH 02, SlidesDocument19 pagesEFM2e, CH 02, SlidesEricLiangtoNo ratings yet

- Chapter 2Document35 pagesChapter 2Aimes AliNo ratings yet

- Chap 002Document24 pagesChap 002samina aliNo ratings yet

- Financial AccountingDocument9 pagesFinancial AccountingRiya DhanukaNo ratings yet

- Full Download Solutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111 PDF Full ChapterDocument36 pagesFull Download Solutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111 PDF Full Chapterurocelespinningnuyu100% (20)

- Solutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111Document36 pagesSolutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111epha.thialol.lqoc100% (50)

- Fin 311 Chapter 02 HandoutDocument7 pagesFin 311 Chapter 02 HandouteinsteinspyNo ratings yet

- Solution Manual For Essentials of Corporate Finance 10th by RossDocument38 pagesSolution Manual For Essentials of Corporate Finance 10th by Rossjohnniewalshhtlw100% (21)

- Fap All AnswersDocument192 pagesFap All Answerssahudhruv1908No ratings yet

- Financial Statements, Taxes, and Cash Flow: Mcgraw-Hill/IrwinDocument45 pagesFinancial Statements, Taxes, and Cash Flow: Mcgraw-Hill/IrwinMinh PhươngNo ratings yet

- FinMan - Case #1Document3 pagesFinMan - Case #1Shaula Tan SombilonNo ratings yet

- Cash Flows - Part II: Analysing The Cash Flow Statement: DirectorDocument5 pagesCash Flows - Part II: Analysing The Cash Flow Statement: DirectorRaniNo ratings yet

- Financial Statements, Taxes and Cash Flow: Chapter TwoDocument21 pagesFinancial Statements, Taxes and Cash Flow: Chapter TwoKids SocietyNo ratings yet

- CH 2Document36 pagesCH 2TakouhiNo ratings yet

- MBA CF Session 3 PDFDocument22 pagesMBA CF Session 3 PDFbiranchinpNo ratings yet

- Financial Statements: The Balance Sheet, Income Statement, and Cash Flow StatementDocument8 pagesFinancial Statements: The Balance Sheet, Income Statement, and Cash Flow Statementr.jeyashankar9550No ratings yet

- Walmart ValuationDocument24 pagesWalmart ValuationnessawhoNo ratings yet

- Laporan Keuangan Dan PajakDocument39 pagesLaporan Keuangan Dan PajakpurnamaNo ratings yet

- Tax Estimates: April 15 June 15 September 15 December 15Document30 pagesTax Estimates: April 15 June 15 September 15 December 15Lana BoydNo ratings yet

- FIN 310 - Chapter 2 Questions - AnswersDocument7 pagesFIN 310 - Chapter 2 Questions - AnswersKelby BahrNo ratings yet

- Ias 12,7 Ifrs 9Document10 pagesIas 12,7 Ifrs 9AssignemntNo ratings yet

- Financial PlanningDocument28 pagesFinancial Planningdabigshow85No ratings yet

- Glosario de FinanzasDocument9 pagesGlosario de FinanzasRaúl VargasNo ratings yet

- Submitted To: Hashem M Khaiyyum (KHM) Lecturer Department of Finance and Accounting School of Business North South UniversityDocument5 pagesSubmitted To: Hashem M Khaiyyum (KHM) Lecturer Department of Finance and Accounting School of Business North South UniversitySamin ChowdhuryNo ratings yet

- Laporan Keuangan Dan PajakDocument39 pagesLaporan Keuangan Dan PajakFerry JohNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument8 pagesFinancial Statements, Cash Flow, and TaxesRaihan Eibna RezaNo ratings yet

- BT-Chap 2Document11 pagesBT-Chap 2Diệu Quỳnh100% (1)

- Solution Manual For Fundamentals of Corporate Finance 10Th Edition by Ross Westerfield Jordan Isbn 0078034639 9780078034633 Full Chapter PDFDocument33 pagesSolution Manual For Fundamentals of Corporate Finance 10Th Edition by Ross Westerfield Jordan Isbn 0078034639 9780078034633 Full Chapter PDFjudy.pierce330100% (12)

- SALES INCREASED BY $2,602,000.: Accruals Payable Accounts S Inventorie Receivable Accounts CashDocument4 pagesSALES INCREASED BY $2,602,000.: Accruals Payable Accounts S Inventorie Receivable Accounts CashChristine Khay Gabriel BulawitNo ratings yet

- Illustration On AFN (FE 12)Document39 pagesIllustration On AFN (FE 12)Jessica Adharana KurniaNo ratings yet

- ' Chapter 2 Lecture Notes STUDENTS SEPT 2023Document19 pages' Chapter 2 Lecture Notes STUDENTS SEPT 2023evelyngoveaNo ratings yet

- Assignment FsaDocument4 pagesAssignment Fsamolka BouzribaNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Project at A Glance - Top Sheet: Taluk/Block: District: Pin: State: E-Mail: MobileDocument7 pagesProject at A Glance - Top Sheet: Taluk/Block: District: Pin: State: E-Mail: MobileFaruk AlamNo ratings yet

- Higher Secondary Accounts Syllabus NewDocument10 pagesHigher Secondary Accounts Syllabus NewBIKASH166No ratings yet

- S&P500 Handbook SheetDocument2 pagesS&P500 Handbook SheetRavi Swaminathan0% (1)

- Pertemuan -5 (1)Document12 pagesPertemuan -5 (1)Frida SalsabilaNo ratings yet

- Answer 11Document10 pagesAnswer 11kamallNo ratings yet

- Property, Plant and Equipment: Group 8 LeaderDocument35 pagesProperty, Plant and Equipment: Group 8 LeaderApril ManjaresNo ratings yet

- Chapter 1Document34 pagesChapter 1Aira Nhaira MecateNo ratings yet

- Afar QuestionsDocument16 pagesAfar QuestionsJessarene Fauni Depante50% (18)

- FSA 5 Ratio AnalysisDocument50 pagesFSA 5 Ratio AnalysisTanbir Ahsan RubelNo ratings yet

- Individual Assignment Financial Accounting and Report 1Document7 pagesIndividual Assignment Financial Accounting and Report 1Sahal Cabdi AxmedNo ratings yet

- A Study On Working CapitalDocument7 pagesA Study On Working CapitalkpmazeedNo ratings yet

- Acc Finalpracticalfile Class12Document30 pagesAcc Finalpracticalfile Class12Kartik RawatNo ratings yet

- Which of The Following Is An Auditor Least Likely To Consider A Departure From Generally Accepted Accounting PrinciplesDocument3 pagesWhich of The Following Is An Auditor Least Likely To Consider A Departure From Generally Accepted Accounting PrinciplesKudryNo ratings yet

- # Solution: 900,000/100,000 9:. 9 16 144Document5 pages# Solution: 900,000/100,000 9:. 9 16 144Joel Christian MascariñaNo ratings yet

- Chap 5Document43 pagesChap 5Akm Engida67% (3)

- FIN2601 Study Unit 6 Exam QuestionsDocument6 pagesFIN2601 Study Unit 6 Exam QuestionsLungile SitholeNo ratings yet

- The Value of Common StocksDocument14 pagesThe Value of Common StocksAalo M ChakrabortyNo ratings yet

- UntitledDocument9 pagesUntitledTaneo, Anesa P.No ratings yet

- Student SpreadsheetDocument28 pagesStudent SpreadsheetDebeesantosh Prakash50% (2)

- Ar Ada NR - 223Document4 pagesAr Ada NR - 223Maliha KansiNo ratings yet

- Tata Moters" 2011-2013 A Project Report On Financial Analysis of "Tata Motors"Document46 pagesTata Moters" 2011-2013 A Project Report On Financial Analysis of "Tata Motors"Arpkin_loveNo ratings yet

- Chapter 1 The Accounting ProcessDocument15 pagesChapter 1 The Accounting ProcessRazel De DiosNo ratings yet

- Ratio Analysis About Ganesh Metals CompanyDocument41 pagesRatio Analysis About Ganesh Metals CompanyshaileshNo ratings yet

- Capital and Revenue ReceiptDocument14 pagesCapital and Revenue ReceiptMuskan BohraNo ratings yet

- 1 - Ifrs 1-First-Time Adoption of IfrsDocument56 pages1 - Ifrs 1-First-Time Adoption of Ifrsyonas alemuNo ratings yet

- Introduction To Managerial Accounting and Job Order Cost SystemsDocument57 pagesIntroduction To Managerial Accounting and Job Order Cost SystemsRajanNo ratings yet