You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Laws Affecting Nursing Practice in The PhilippinesDocument6 pagesLaws Affecting Nursing Practice in The PhilippinesEzurn80% (5)

- 132 KV SubstationDocument18 pages132 KV Substationparmodbishyan75% (4)

- NTTP 3 02 1mDocument334 pagesNTTP 3 02 1mfatihy73No ratings yet

- Gillette Personal Care DivisionDocument4 pagesGillette Personal Care DivisionVeer Korra100% (1)

- WW C70 Product-Page English 12-2015 1Document5 pagesWW C70 Product-Page English 12-2015 1rafaelcoserNo ratings yet

- Directional DrillingDocument23 pagesDirectional DrillingConstantino Danilo Zapata Mogollon100% (1)

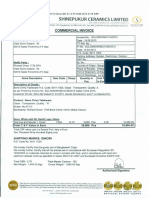

- Commercial Invoice-106-2012Document1 pageCommercial Invoice-106-2012GqyNo ratings yet

- Detection of Homozygous and Hemizygous Complete or Partial Exon Deletions by Whole-Exome SequencingDocument10 pagesDetection of Homozygous and Hemizygous Complete or Partial Exon Deletions by Whole-Exome SequencingMoundir AbderrahmaneNo ratings yet

- Spc250 Truck Crane 25 Tons Lifting Capacity: Quality Changes The WorldDocument9 pagesSpc250 Truck Crane 25 Tons Lifting Capacity: Quality Changes The WorldMK PNPNo ratings yet

- DIY Induction Heater PDFDocument10 pagesDIY Induction Heater PDFPol IllaNo ratings yet

- ACCTG1 Chapter 4Document11 pagesACCTG1 Chapter 4Mark Kevin JavierNo ratings yet

- Group 1: Abordo, Jezzle Anne Boreros, Christall Jane Gumobao, Winzelle Morales, Jane Erica Sibala, Rayshell KateDocument14 pagesGroup 1: Abordo, Jezzle Anne Boreros, Christall Jane Gumobao, Winzelle Morales, Jane Erica Sibala, Rayshell KateRudy LugasNo ratings yet

- Java ProgramsDocument60 pagesJava ProgramsbagrechaamitNo ratings yet

- In The Court of 3Rd Additioal Sessions Judge, District Court, Gandhinagar Cri. Misc. Application No.155/2020 EXH.... ApplicantDocument6 pagesIn The Court of 3Rd Additioal Sessions Judge, District Court, Gandhinagar Cri. Misc. Application No.155/2020 EXH.... Applicantraj trivediNo ratings yet

- Microprocessor: Viva QuestionsDocument6 pagesMicroprocessor: Viva QuestionshrrameshhrNo ratings yet

- Ultrasound - Versana Active BrochureDocument5 pagesUltrasound - Versana Active BrochureAriNo ratings yet

- YqOppZqahKGao5us 219845 210 2023 87945461 230Document1 pageYqOppZqahKGao5us 219845 210 2023 87945461 230noemimb1102No ratings yet

- Hop-On Hop-Of City Sightseeing Tour 2023 2Document1 pageHop-On Hop-Of City Sightseeing Tour 2023 2tbhbhtNo ratings yet

- Ch1 - Sustainable DevelopmentDocument9 pagesCh1 - Sustainable DevelopmentLee Tin YanNo ratings yet

- CS 200 Lab1 ManualDocument7 pagesCS 200 Lab1 Manualumar khanNo ratings yet

- JN4 Jenny MSFS ManualDocument11 pagesJN4 Jenny MSFS ManualmatheusNo ratings yet

- Unit - VI: Computer GraphicsDocument30 pagesUnit - VI: Computer Graphicssri ram reddy arimandaNo ratings yet

- Flynn and Giraldez - Born With A "Silver Spoon" (The Origin of World Trade in 1571)Document22 pagesFlynn and Giraldez - Born With A "Silver Spoon" (The Origin of World Trade in 1571)D-2o4j48dol20iilylz0No ratings yet

- Artikel Bahasa Inggris Tentang Ekonomi Our Economic Woes and Their CureDocument8 pagesArtikel Bahasa Inggris Tentang Ekonomi Our Economic Woes and Their CureandrafitrianNo ratings yet

- Comparison of Workers Comp 2009Document224 pagesComparison of Workers Comp 2009workcovervictim8242No ratings yet

- MGT 300 Chapter 13 NotesDocument31 pagesMGT 300 Chapter 13 NotesSarah PinckNo ratings yet

- Cyanamid Phil V CIRDocument1 pageCyanamid Phil V CIRAnonymous MikI28PkJcNo ratings yet

- Alonzo, Tejano TegacyDocument8 pagesAlonzo, Tejano TegacyGJMONo ratings yet

- Independent Contractor Application PDFDocument11 pagesIndependent Contractor Application PDFmbarrientos12382% (11)