You might also like

- 49.transfer PricingDocument4 pages49.transfer PricingmercatuzNo ratings yet

- India: Type of Transactions CoveredDocument27 pagesIndia: Type of Transactions CoveredPadmanabha NarayanNo ratings yet

- Transfer PricingDocument53 pagesTransfer PricingkannnamreddyeswarNo ratings yet

- RR 2-2013 PDFDocument23 pagesRR 2-2013 PDFnaldsdomingoNo ratings yet

- United Arab Emirates - Corporate - Group TaxationDocument5 pagesUnited Arab Emirates - Corporate - Group TaxationMuhammad UmarNo ratings yet

- TO: Atty. Stephen Yu FROM: Maria Ludica B. Oja DATE: January 13, 2017 Subject: Transfer Pricing Transfer Pricing DefinedDocument4 pagesTO: Atty. Stephen Yu FROM: Maria Ludica B. Oja DATE: January 13, 2017 Subject: Transfer Pricing Transfer Pricing DefinedLudica OjaNo ratings yet

- India: Type of Transactions CoveredDocument20 pagesIndia: Type of Transactions Coveredss_scribdNo ratings yet

- Transfer Pricing in The PhilippinesDocument8 pagesTransfer Pricing in The PhilippinesJayson Berja de LeonNo ratings yet

- Transfer Pricing' - An International Taxation Issue Concerning The Balance of Interest Between The Tax Payer and Tax AdministratorDocument8 pagesTransfer Pricing' - An International Taxation Issue Concerning The Balance of Interest Between The Tax Payer and Tax AdministratorchristianNo ratings yet

- (2015) 55 Taxmann - Com 40 (Article) Demystifying The Indian Advance Pricing Agreement ProgramDocument10 pages(2015) 55 Taxmann - Com 40 (Article) Demystifying The Indian Advance Pricing Agreement Programsuraj gulipalliNo ratings yet

- Transfer Pricing Regulations Take Off in GhanaDocument5 pagesTransfer Pricing Regulations Take Off in GhanafbuameNo ratings yet

- Transfer PricingDocument111 pagesTransfer PricingMamun0% (1)

- Chile: Transfer Pricing GuideDocument7 pagesChile: Transfer Pricing GuideSebastián Torres SeguelNo ratings yet

- Vietnam Tax Transfer Pricing DecreeDocument36 pagesVietnam Tax Transfer Pricing DecreePaula Aurora MendozaNo ratings yet

- Philippines Transfer Pricing RulesDocument5 pagesPhilippines Transfer Pricing RulesJade BautistaNo ratings yet

- Bos 53930 CP 1Document121 pagesBos 53930 CP 1arashpreet kaur dhanjuNo ratings yet

- The New Transfer Pricing Regime in The United Arab Emirates - ITCDocument9 pagesThe New Transfer Pricing Regime in The United Arab Emirates - ITCmarketingNo ratings yet

- Uae Corporate Tax Transfer Pricing GuideDocument7 pagesUae Corporate Tax Transfer Pricing GuideMuhammad UmarNo ratings yet

- OECD Discussion Draft Implementation Guidance On HTVIDocument8 pagesOECD Discussion Draft Implementation Guidance On HTVIMario AlfaroNo ratings yet

- Income Tax (TP) Regulation Presentation Slide For InductionDocument41 pagesIncome Tax (TP) Regulation Presentation Slide For InductionUmar AbdulkabirNo ratings yet

- TP Rules BaladadDocument3 pagesTP Rules BaladadJomel ManaigNo ratings yet

- TP METHODSDocument22 pagesTP METHODSSrikrishna DharNo ratings yet

- Miller Thomson - An Overview of Transfer Pricing in Canada PDFDocument3 pagesMiller Thomson - An Overview of Transfer Pricing in Canada PDFSen JanNo ratings yet

- Transfer Pricing CasesDocument6 pagesTransfer Pricing CasesShreya SinghNo ratings yet

- Budget 2017 Bringing India Closer To Global PracticesDocument13 pagesBudget 2017 Bringing India Closer To Global PracticesTaxpert mukeshNo ratings yet

- Ransfer Ricing in Anada: Jack BernsteinDocument12 pagesRansfer Ricing in Anada: Jack BernsteinpuneetbadhwarNo ratings yet

- APA - Advance Pricing Agreement in IndiaDocument6 pagesAPA - Advance Pricing Agreement in IndiaJating JamkhandiNo ratings yet

- PPSAS 23 - Revenue From Non-Exchange Trans Oct - 18 2013Document3 pagesPPSAS 23 - Revenue From Non-Exchange Trans Oct - 18 2013Ar LineNo ratings yet

- Transfer Pricing authority tax law MalaysiaDocument9 pagesTransfer Pricing authority tax law MalaysiaazshamNo ratings yet

- Bir Ruling 047-2013Document8 pagesBir Ruling 047-2013Ar Yan SebNo ratings yet

- Profits Tax IX Transfer PricingDocument49 pagesProfits Tax IX Transfer Pricinggary_nggNo ratings yet

- Service Tax Valuation RulesDocument10 pagesService Tax Valuation Rulespriyals92No ratings yet

- GST BILL Highlights of Draft Model GST LawDocument6 pagesGST BILL Highlights of Draft Model GST LawS Sinha RayNo ratings yet

- Transfer PricingDocument13 pagesTransfer Pricingamandeep kansalNo ratings yet

- IMChap 012Document18 pagesIMChap 012Aaron Hamilton100% (2)

- IFRS 15 Revenue From Contracts With Customers-2Document8 pagesIFRS 15 Revenue From Contracts With Customers-2abbyNo ratings yet

- 132_2020_ND-CP_459238 -englishDocument56 pages132_2020_ND-CP_459238 -englishmaile.dhcdNo ratings yet

- OtesvatDocument18 pagesOtesvatRichelle Joy Reyes BenitoNo ratings yet

- Singapore Transfer Pricing Guidelines 3rdDocument106 pagesSingapore Transfer Pricing Guidelines 3rdLim Jiew KwangNo ratings yet

- PWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018Document12 pagesPWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018sourabhbansal108No ratings yet

- 2019 Transfer Pricing Overview For HungaryDocument13 pages2019 Transfer Pricing Overview For HungaryAccaceNo ratings yet

- Rmo No. 14 2021Document13 pagesRmo No. 14 2021Christine Fe BuencaminoNo ratings yet

- Working Capital Adjustments Under Transfer PricingDocument9 pagesWorking Capital Adjustments Under Transfer PricingTaxpert Professionals Private LimitedNo ratings yet

- (2012) 6 ILT 496 (Article) India Enters A New Era in Transfer Pricing With Introduction of Advance Pricing AgreementsDocument10 pages(2012) 6 ILT 496 (Article) India Enters A New Era in Transfer Pricing With Introduction of Advance Pricing Agreementssuraj gulipalliNo ratings yet

- Transfer PricingDocument6 pagesTransfer Pricingrpulgam09No ratings yet

- Note 4Document116 pagesNote 4sohamdivekar9867No ratings yet

- UN Manual TransferPricingDocument37 pagesUN Manual TransferPricingannichiaricofabianNo ratings yet

- Transfer Pricing Audit Guidelines, Revenue Audit Memorandum Order No. 001-19, (August 20, 2019) PDFDocument49 pagesTransfer Pricing Audit Guidelines, Revenue Audit Memorandum Order No. 001-19, (August 20, 2019) PDFKriszan ManiponNo ratings yet

- ContentsDocument26 pagesContentsTlhadia KabubiNo ratings yet

- US Internal Revenue Service: rp-06-9Document38 pagesUS Internal Revenue Service: rp-06-9IRSNo ratings yet

- Pricing: Transfer Pricing Law in IndiaDocument15 pagesPricing: Transfer Pricing Law in IndiaVenky BabluNo ratings yet

- Taxation IIDocument3 pagesTaxation IIAnonymous BNrz1arNo ratings yet

- f2 Taxation Revenue AuditDocument5 pagesf2 Taxation Revenue AuditKishan KudiaNo ratings yet

- Transfer Pricing SruthiDocument12 pagesTransfer Pricing Sruthisruthi karthiNo ratings yet

- Tax Audit Manual - 2Document168 pagesTax Audit Manual - 2tolera100% (3)

- TRANSFER PRICING IN TANZANIADocument4 pagesTRANSFER PRICING IN TANZANIAbernardsway02No ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Transparency in Financial Reporting: A concise comparison of IFRS and US GAAPFrom EverandTransparency in Financial Reporting: A concise comparison of IFRS and US GAAPRating: 4.5 out of 5 stars4.5/5 (3)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Budget, 2010 Amendment at A Glance: Compiled By: PAMS & AssociatesDocument15 pagesBudget, 2010 Amendment at A Glance: Compiled By: PAMS & Associatespawanagrawal83No ratings yet

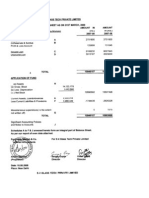

- Balance SheetDocument13 pagesBalance Sheetpawanagrawal83No ratings yet

- MOADocument19 pagesMOApawanagrawal83No ratings yet

- Budget 2010 HighlightsDocument11 pagesBudget 2010 Highlightspawanagrawal83No ratings yet

- (The Companies Act, 1956) (Company Limited byDocument5 pages(The Companies Act, 1956) (Company Limited bypawanagrawal83No ratings yet

- (The Companies Act, 1956) (Company Limited byDocument6 pages(The Companies Act, 1956) (Company Limited bypawanagrawal83No ratings yet

- Articles of Association of Dadri Commercial PrivateDocument9 pagesArticles of Association of Dadri Commercial Privatepawanagrawal83No ratings yet

- Sennheiser Electronics (India) Private Limited: Transfer Pricing DocumentationDocument63 pagesSennheiser Electronics (India) Private Limited: Transfer Pricing Documentationpawanagrawal8386% (7)

- Profile Word FileDocument20 pagesProfile Word Filepawanagrawal83No ratings yet

- (The Companies Act, 1956) (Company Limited byDocument5 pages(The Companies Act, 1956) (Company Limited bypawanagrawal83No ratings yet

- (The Companies Act, 1956) (Company Limited by Shares) MEMORANDUM ofDocument6 pages(The Companies Act, 1956) (Company Limited by Shares) MEMORANDUM ofpawanagrawal83No ratings yet

- (The Companies Act, 1956) (Company Limited by Shares) MEMORANDUM ofDocument6 pages(The Companies Act, 1956) (Company Limited by Shares) MEMORANDUM ofpawanagrawal83No ratings yet

- Articles of Association of Purotech Home Appliances (P) LimitedDocument9 pagesArticles of Association of Purotech Home Appliances (P) Limitedpawanagrawal83No ratings yet