You might also like

- Beware That The Housing Market Is Poised For Another Leg DownDocument4 pagesBeware That The Housing Market Is Poised For Another Leg DownValuEngine.comNo ratings yet

- April 2010 Charleston Market ReportDocument31 pagesApril 2010 Charleston Market ReportbrundbakenNo ratings yet

- The Mortgage Market: Presented By: Brady Anderson Chad Atkinson Charles Jones Mcleod Robinson Laura RogersDocument31 pagesThe Mortgage Market: Presented By: Brady Anderson Chad Atkinson Charles Jones Mcleod Robinson Laura Rogerschhassan7No ratings yet

- Guaranteed to Fail: Fannie Mae, Freddie Mac, and the Debacle of Mortgage FinanceFrom EverandGuaranteed to Fail: Fannie Mae, Freddie Mac, and the Debacle of Mortgage FinanceRating: 2 out of 5 stars2/5 (1)

- Fannie Mae and Freddie MacDocument3 pagesFannie Mae and Freddie MacGeorge di Montorio-VeroneseNo ratings yet

- Committee On Financial Services: United States House of RepresentativesDocument3 pagesCommittee On Financial Services: United States House of RepresentativesDinSFLANo ratings yet

- May 2010 Charleston Market ReportDocument38 pagesMay 2010 Charleston Market ReportbrundbakenNo ratings yet

- Dow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysDocument10 pagesDow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysAlbert L. PeiaNo ratings yet

- Dow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysDocument10 pagesDow Closes Above 11,000 This Rally Has Ignored Fundamentals, and Will Be Corrected Painfully, Hussman SaysAlbert L. PeiaNo ratings yet

- Is This The Initiative That Could Turn Things Around?: Presented by Fred Leamnson, AIFDocument3 pagesIs This The Initiative That Could Turn Things Around?: Presented by Fred Leamnson, AIFapi-118535366No ratings yet

- The Cost of Government Financial Interventions, Past and PresentDocument6 pagesThe Cost of Government Financial Interventions, Past and Presentalex1521dfNo ratings yet

- Fairy Tale Capitalism: Fact and Fiction Behind Too Big to FailFrom EverandFairy Tale Capitalism: Fact and Fiction Behind Too Big to FailNo ratings yet

- Did Deregulation or Nonregulation Cause The Finance Crisis?: Not A Failure of Capitalism-A Failure of GovernmentDocument4 pagesDid Deregulation or Nonregulation Cause The Finance Crisis?: Not A Failure of Capitalism-A Failure of GovernmentSapphire AnhNo ratings yet

- Making Money From The MeltdownDocument52 pagesMaking Money From The Meltdownrnj1230100% (1)

- Four in Four ReportDocument2 pagesFour in Four ReportValuEngine.comNo ratings yet

- The Fed - Its Raining Its Pouring The Old Man Is Snoring - Fed Rains Money On Wall Street-Nothing For Main Street AmericansDocument10 pagesThe Fed - Its Raining Its Pouring The Old Man Is Snoring - Fed Rains Money On Wall Street-Nothing For Main Street Americans83jjmackNo ratings yet

- Memo To Valerie Jarrett RE Fannie Mae and Freddie Mac April2010Document3 pagesMemo To Valerie Jarrett RE Fannie Mae and Freddie Mac April2010Kim HedumNo ratings yet

- Economic Focus January 30, 2012Document1 pageEconomic Focus January 30, 2012Jessica Kister-LombardoNo ratings yet

- Howard Marks Fourth Quarter 2009 MemoDocument12 pagesHoward Marks Fourth Quarter 2009 MemoDealBook100% (3)

- The Economic Backdrop Not As Strong As AdvertisedDocument2 pagesThe Economic Backdrop Not As Strong As AdvertisedValuEngine.comNo ratings yet

- Economic Focus 9-5-11Document1 pageEconomic Focus 9-5-11Jessica Kister-LombardoNo ratings yet

- Housing Crisis ReportDocument26 pagesHousing Crisis ReportsechNo ratings yet

- The Coming Bond Market Collapse: How to Survive the Demise of the U.S. Debt MarketFrom EverandThe Coming Bond Market Collapse: How to Survive the Demise of the U.S. Debt MarketNo ratings yet

- Anatomy Subprime CrisisDocument49 pagesAnatomy Subprime CrisisAbhay ManeNo ratings yet

- Fall 2011 Newsletter - Jane JensenDocument4 pagesFall 2011 Newsletter - Jane JensenJane JensenNo ratings yet

- Stock Market Investing for Beginners: And Intermediate. Learn to Generate Passive Income with Investing, Stock Trading, Day Trading Stock. Useful for Cryptocurrency. Great to Listen in a Car!From EverandStock Market Investing for Beginners: And Intermediate. Learn to Generate Passive Income with Investing, Stock Trading, Day Trading Stock. Useful for Cryptocurrency. Great to Listen in a Car!No ratings yet

- White Paper Treasury Fannie Mae FINALDocument19 pagesWhite Paper Treasury Fannie Mae FINALTodd SullivanNo ratings yet

- Economic Stimulus House Plan 0121091Document18 pagesEconomic Stimulus House Plan 0121091AnicaButlerNo ratings yet

- The FBI Estimates That 80 Percent of All Mortgage Fraud Involves Collaboration or Collusion by Industry InsidersDocument31 pagesThe FBI Estimates That 80 Percent of All Mortgage Fraud Involves Collaboration or Collusion by Industry Insiders83jjmack100% (1)

- Max Keiser and Gerald Celente Deconstruct Financial FraudDocument10 pagesMax Keiser and Gerald Celente Deconstruct Financial FraudAlbert L. PeiaNo ratings yet

- The Federal Housing Administration Saved The Housing MarketDocument12 pagesThe Federal Housing Administration Saved The Housing MarketCenter for American ProgressNo ratings yet

- Is It All Just A Ponzi Scheme?: By: Eric Sprott & David FranklinDocument5 pagesIs It All Just A Ponzi Scheme?: By: Eric Sprott & David FranklinZerohedgeNo ratings yet

- House Hearing, 112TH Congress - Fannie Mae, Freddie Mac & Fha: Taxpayer Exposure in The Housing MarketsDocument104 pagesHouse Hearing, 112TH Congress - Fannie Mae, Freddie Mac & Fha: Taxpayer Exposure in The Housing MarketsScribd Government DocsNo ratings yet

- Government Austerity Measures Next StepDocument10 pagesGovernment Austerity Measures Next StepkakeroteNo ratings yet

- US Economy ReportDocument7 pagesUS Economy Reportjuran parkerNo ratings yet

- Crisis FinancieraDocument4 pagesCrisis Financierahawk91No ratings yet

- National Debt ThesisDocument6 pagesNational Debt Thesisbrandygranttallahassee100% (2)

- Housing Special ReportDocument33 pagesHousing Special ReportLDJIIINo ratings yet

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Fannie MaeDocument6 pagesFannie MaeChahnaz KobeissiNo ratings yet

- Legg Mason StrategyDocument6 pagesLegg Mason Strategyapi-26172897No ratings yet

- The Real World of Money and Taxation in AmericaDocument9 pagesThe Real World of Money and Taxation in AmericaPotomacOracleNo ratings yet

- Summary - Reckless EndangermentDocument2 pagesSummary - Reckless Endangermentjigar_parikh1No ratings yet

- Why We Must End Too Big To FailDocument21 pagesWhy We Must End Too Big To FailBryan CastañedaNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document29 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- Is FHA The Next Housing Bailout?: Joseph GyourkoDocument50 pagesIs FHA The Next Housing Bailout?: Joseph GyourkoLarry RobertsNo ratings yet

- The Credit Squeeze Is Intensifying On Main StreetDocument4 pagesThe Credit Squeeze Is Intensifying On Main StreetValuEngine.comNo ratings yet

- How to Reverse World Recession in Matter of Days: Win 10 Million Dollar to Prove It WrongFrom EverandHow to Reverse World Recession in Matter of Days: Win 10 Million Dollar to Prove It WrongNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document17 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- Weekly Market Commentary 07-05-2011Document4 pagesWeekly Market Commentary 07-05-2011Jeremy A. MillerNo ratings yet

- Dissent from the Majority Report of the Financial Crisis Inquiry CommissionFrom EverandDissent from the Majority Report of the Financial Crisis Inquiry CommissionNo ratings yet

- Shelter from the Storm: How a COVID Mortgage Meltdown Was AvertedFrom EverandShelter from the Storm: How a COVID Mortgage Meltdown Was AvertedNo ratings yet

- Treasury and Conservatorship by Timothy Howard Jan 11 2015Document8 pagesTreasury and Conservatorship by Timothy Howard Jan 11 2015dpsimswm100% (1)

- Subprime Is The Cause of USA Economy Melt Down. It Is The Very Popular News AmongDocument18 pagesSubprime Is The Cause of USA Economy Melt Down. It Is The Very Popular News AmongPradeep SahooNo ratings yet

- Government Austerity Measures Next StepDocument10 pagesGovernment Austerity Measures Next StepkakeroteNo ratings yet

- Stock Market Investing for Beginners: The Keys to Protecting Your Wealth and Making Big Profits In a Market CrashFrom EverandStock Market Investing for Beginners: The Keys to Protecting Your Wealth and Making Big Profits In a Market CrashNo ratings yet

- The Real Crash: America's Coming Bankruptcy - How to Save Yourself and Your CountryFrom EverandThe Real Crash: America's Coming Bankruptcy - How to Save Yourself and Your CountryRating: 4 out of 5 stars4/5 (5)

- Diamond and Kashyap On The Recent Financial Upheavals: Steven D. LevittDocument6 pagesDiamond and Kashyap On The Recent Financial Upheavals: Steven D. LevittfarrukhazeemNo ratings yet

- Asymmetric Information and Financial Crises: Group MembersDocument13 pagesAsymmetric Information and Financial Crises: Group MembersTayyaba RehmanNo ratings yet

- Snack With Dave: David A. RosenbergDocument9 pagesSnack With Dave: David A. RosenbergroquessudeNo ratings yet

- March 2010 Charleston Market ReportDocument26 pagesMarch 2010 Charleston Market ReportbrundbakenNo ratings yet

- February 2010 Charleston Market ReportDocument23 pagesFebruary 2010 Charleston Market ReportbrundbakenNo ratings yet

- May 2010 Charleston Market ReportDocument38 pagesMay 2010 Charleston Market ReportbrundbakenNo ratings yet

- December 2009 Charleston Market ReportDocument25 pagesDecember 2009 Charleston Market ReportbrundbakenNo ratings yet

- November 2009 Charleston Market ReportDocument20 pagesNovember 2009 Charleston Market ReportbrundbakenNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document29 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- Q3 2007 Charleston Market ReportDocument7 pagesQ3 2007 Charleston Market ReportbrundbakenNo ratings yet

- Q2 2008 Charleston Market ReportDocument32 pagesQ2 2008 Charleston Market ReportbrundbakenNo ratings yet

- Q3 2008 Charleston Market ReportDocument23 pagesQ3 2008 Charleston Market ReportbrundbakenNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document36 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document36 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- December 2007 Charleston Market ReportDocument13 pagesDecember 2007 Charleston Market ReportbrundbakenNo ratings yet

- August 2007 Charleston Market ReportDocument7 pagesAugust 2007 Charleston Market ReportbrundbakenNo ratings yet

- September 2007 Charleston Market ReportDocument7 pagesSeptember 2007 Charleston Market ReportbrundbakenNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document29 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Document17 pagesThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenNo ratings yet

- January 2007 Charleston Market ReportDocument4 pagesJanuary 2007 Charleston Market ReportbrundbakenNo ratings yet

- Feb 2009 CMR1Document26 pagesFeb 2009 CMR1brundbakenNo ratings yet

- Feb 2009 CMRDocument26 pagesFeb 2009 CMRbrundbaken100% (2)

- MPP 2017nov15 Digitalization Full ReportDocument60 pagesMPP 2017nov15 Digitalization Full ReportSkimboNo ratings yet

- RMC No. 5-2009Document1 pageRMC No. 5-2009CROCS Acctg & Audit Dep'tNo ratings yet

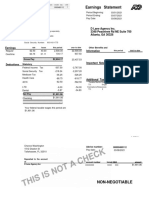

- Earnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Document1 pageEarnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Muhammad AdeelNo ratings yet

- NovemberDocument9 pagesNovemberkaty.haugland2No ratings yet

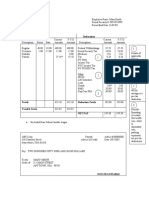

- Earnings: Hourly Ot Sick Cctips Mealper Prempay RetailcomDocument1 pageEarnings: Hourly Ot Sick Cctips Mealper Prempay Retailcomalfredo velezNo ratings yet

- Publicación 963 IRS (Seguro Social) PDFDocument172 pagesPublicación 963 IRS (Seguro Social) PDFEmily RamosNo ratings yet

- 11 Memorial Victims SSA Death Index Cross ReferenceDocument128 pages11 Memorial Victims SSA Death Index Cross ReferenceanasirralhaqNo ratings yet

- Employee's Withholding Certificate 2020Document4 pagesEmployee's Withholding Certificate 2020CNBC.comNo ratings yet

- Structural Deficit PowerPointDocument11 pagesStructural Deficit PowerPointGovernor Tom WolfNo ratings yet

- File by Mail Instructions For Your 2019 Federal Tax ReturnDocument7 pagesFile by Mail Instructions For Your 2019 Federal Tax ReturnKevin Osorio100% (2)

- Pay Stub Template 03 PDFDocument1 pagePay Stub Template 03 PDFchairgraveyardNo ratings yet

- POR7 Voting Results 0812229120213000000000026Document389 pagesPOR7 Voting Results 0812229120213000000000026joeMcoolNo ratings yet

- Sample Business Plan 1 2021 2022Document23 pagesSample Business Plan 1 2021 2022Claudio MatarazzoNo ratings yet

- Ten Mile Day-SummaryDocument1 pageTen Mile Day-SummaryPsic. Ó. Bernardo Duarte B.100% (1)

- Tanf Syep Eligibility/Screening: Purpose 1Document1 pageTanf Syep Eligibility/Screening: Purpose 1Kevin CardosoNo ratings yet

- Form W-4 (2019) : Specific InstructionsDocument5 pagesForm W-4 (2019) : Specific Instructionsjok mongNo ratings yet

- 1701qjuly2008 (ENCS)Document6 pages1701qjuly2008 (ENCS)alvie_budNo ratings yet

- Demetrious Dabadee 08-15-2023-3Document1 pageDemetrious Dabadee 08-15-2023-3Irfan khanNo ratings yet

- United States Bankruptcy Court Southern District of New YorkDocument13 pagesUnited States Bankruptcy Court Southern District of New YorkChapter 11 DocketsNo ratings yet

- Pay Stub Portal3Document1 pagePay Stub Portal3cwhite2150No ratings yet

- Business PlanDocument19 pagesBusiness Planmahrooj rathana zafarNo ratings yet

- Indian Economy Growth Since IndependenceDocument11 pagesIndian Economy Growth Since Independencevinay jodNo ratings yet

- Sample Computaion of Estate TaxDocument6 pagesSample Computaion of Estate TaxlheyniiNo ratings yet

- WrightRogersAmeSoc HowItReallyWorksDocument429 pagesWrightRogersAmeSoc HowItReallyWorksmataraokina05No ratings yet

- Roosevelt's New Deal: The Revolution of Socialist Ideals in A Capitalist Nation Annotated Bibliography Primary Sources DocumentsDocument14 pagesRoosevelt's New Deal: The Revolution of Socialist Ideals in A Capitalist Nation Annotated Bibliography Primary Sources Documentsapi-126648439No ratings yet

- Exhibit 2 Case 1.12-cv-01398-LAK 01-2Document11 pagesExhibit 2 Case 1.12-cv-01398-LAK 01-2JaniceWolkGrenadierNo ratings yet

- Us Person (Irs)Document2 pagesUs Person (Irs)georaw9588No ratings yet

- 02475792798Document1 page02475792798Edwin Zamora PastorNo ratings yet

- Family Economics and Public Policy, 1800s-PRESENTDocument327 pagesFamily Economics and Public Policy, 1800s-PRESENTMücahit 1907No ratings yet

- Citizens Guide 2008Document12 pagesCitizens Guide 2008DeliajrsNo ratings yet