You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Risk & Return AnalysisDocument13 pagesRisk & Return AnalysisTaleya FatimaNo ratings yet

- Goodwill Questions and Their SolutionsDocument8 pagesGoodwill Questions and Their SolutionsAMIN BUHARI ABDUL KHADERNo ratings yet

- Statement of Changes in EquityDocument8 pagesStatement of Changes in EquityGonzalo Jr. RualesNo ratings yet

- Pengaruh Penerapan Penurunan Nilai Aset Tetap Menurut Psak 48 Terhadap Laporan Keuangan Pada Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia Ayu Rahmaniar PertiwiDocument8 pagesPengaruh Penerapan Penurunan Nilai Aset Tetap Menurut Psak 48 Terhadap Laporan Keuangan Pada Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia Ayu Rahmaniar Pertiwim.fauziNo ratings yet

- Leverage Leverage Refers To The Effects That Fixed Costs Have On The Returns That Shareholders Earn. by "Fixed Costs" WeDocument8 pagesLeverage Leverage Refers To The Effects That Fixed Costs Have On The Returns That Shareholders Earn. by "Fixed Costs" WeMarlon A. RodriguezNo ratings yet

- Accounting For ManagerDocument7 pagesAccounting For ManagerMasara OwenNo ratings yet

- Chapter 1 - Recording Business TransactionDocument14 pagesChapter 1 - Recording Business TransactionThủy NguyễnNo ratings yet

- Capital Budgeting: R.KasilingamDocument71 pagesCapital Budgeting: R.Kasilingamvijayadarshini vNo ratings yet

- Exercises 02 INTACC2 Jackson Kervin Rey GDocument12 pagesExercises 02 INTACC2 Jackson Kervin Rey GKervin Rey Jackson100% (1)

- Module 3 Adjusting Journal EntriesDocument25 pagesModule 3 Adjusting Journal EntriesThriztan Andrei BaluyutNo ratings yet

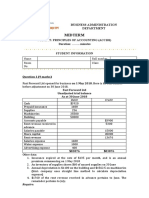

- Midterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationDocument2 pagesMidterm: Hoa Lac Subject: Principles of Accounting (Acc101) Duration: .. Minutes Student InformationNguyen Ngoc Minh Chau (K15 HL)No ratings yet

- Arthaland Analyses of Ratios For The Year 2018Document2 pagesArthaland Analyses of Ratios For The Year 2018ninyapuellaNo ratings yet

- ENTREPRENEURSHIP 12 Q2 M8 Computation of Gross ProfitDocument18 pagesENTREPRENEURSHIP 12 Q2 M8 Computation of Gross ProfitMyleen CastillejoNo ratings yet

- Accounting May-June 2019 EngDocument18 pagesAccounting May-June 2019 Englindort00No ratings yet

- ASE20104 - Examiner Report - March 2019 PDFDocument14 pagesASE20104 - Examiner Report - March 2019 PDFAung Zaw HtweNo ratings yet

- IAS 40 Investment Property PresentationDocument29 pagesIAS 40 Investment Property PresentationNollecy Takudzwa BereNo ratings yet

- SITXFIN004 Learner GuideDocument34 pagesSITXFIN004 Learner GuideTajinder SinghNo ratings yet

- Difference Between Financial and Managerial AccountingDocument10 pagesDifference Between Financial and Managerial AccountingRahman Sankai KaharuddinNo ratings yet

- (Read) Wiley GAAP 2018: Interpretation and Application of Generally Accepted Accounting Principles (Wiley Regulatory Reporting) - For IphoneDocument1 page(Read) Wiley GAAP 2018: Interpretation and Application of Generally Accepted Accounting Principles (Wiley Regulatory Reporting) - For Iphonelipsy250% (1)

- Return On Equity:: A Compelling Case For InvestorsDocument15 pagesReturn On Equity:: A Compelling Case For InvestorsPutri LucyanaNo ratings yet

- Advanced Accounting PDFDocument14 pagesAdvanced Accounting PDFMarie Christine RamosNo ratings yet

- QuestionDocument12 pagesQuestionnmdl123No ratings yet

- Globe Vertical AnalysisDocument22 pagesGlobe Vertical AnalysisArriana RefugioNo ratings yet

- Dba 302 Financial Management Supplementary TestDocument3 pagesDba 302 Financial Management Supplementary Testmulenga lubembaNo ratings yet

- Capital Structure TheoriesDocument31 pagesCapital Structure TheoriesShashank100% (1)

- IAS 32 Financial Instruments - PresentationDocument3 pagesIAS 32 Financial Instruments - PresentationAKNo ratings yet

- Divisible ProfitsDocument45 pagesDivisible Profitsalizai khanNo ratings yet

- Sweet Beginnings Company Balance Sheet For The Year Ended December 31, 2021Document3 pagesSweet Beginnings Company Balance Sheet For The Year Ended December 31, 2021Frylle Kanz Harani PocsonNo ratings yet

- Problem SolvingDocument9 pagesProblem Solvingmax p0% (2)

- Irrecoverable Debts and Allowances For ReceivablesDocument20 pagesIrrecoverable Debts and Allowances For ReceivablesShayan KhanNo ratings yet