You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- May 2013 Advanced TaxationDocument4 pagesMay 2013 Advanced TaxationTIMOREGHNo ratings yet

- Utility, Rationality and Beyond - From Behavioral Finance To Informational FinanceDocument134 pagesUtility, Rationality and Beyond - From Behavioral Finance To Informational FinanceTIMOREGHNo ratings yet

- Internal Revenue Regulations, 2001 (LI 1675)Document48 pagesInternal Revenue Regulations, 2001 (LI 1675)TIMOREGHNo ratings yet

- Advanced Taxation & Fiscal Policy-QuestionDocument2 pagesAdvanced Taxation & Fiscal Policy-QuestionTIMOREGHNo ratings yet

- An Introduction To The History of International Human Rights LawDocument31 pagesAn Introduction To The History of International Human Rights LawAnkit YadavNo ratings yet

- 21 Selected Copyright CasesDocument1 page21 Selected Copyright CasesTIMOREGHNo ratings yet

- Exams Questions For TACDocument7 pagesExams Questions For TACTIMOREGHNo ratings yet

- Capital Allowance QuestionsDocument8 pagesCapital Allowance QuestionsTIMOREGH100% (2)

- Practise Questions E LogisticsDocument5 pagesPractise Questions E LogisticsTIMOREGHNo ratings yet

- Notes On NegotiationDocument111 pagesNotes On NegotiationTIMOREGHNo ratings yet

- Current Trends in NegotiationsDocument60 pagesCurrent Trends in NegotiationsTIMOREGHNo ratings yet

- Steps To Becoming A CPADocument15 pagesSteps To Becoming A CPAImtiaz Mohammed ArafeenNo ratings yet

- Chapter One 20.4.2014Document8 pagesChapter One 20.4.2014TIMOREGHNo ratings yet

- CBI Effectiveness Negotiation TrainingDocument23 pagesCBI Effectiveness Negotiation TrainingTIMOREGHNo ratings yet

- Driver and Vehicle Licensing Authority ActDocument8 pagesDriver and Vehicle Licensing Authority ActTIMOREGHNo ratings yet

- 2013 Tax ChangesDocument8 pages2013 Tax ChangesTIMOREGHNo ratings yet

- ASEA Yearbook2008Document213 pagesASEA Yearbook2008TIMOREGHNo ratings yet

- Doctoral StudiesDocument1 pageDoctoral StudiesTIMOREGHNo ratings yet

- Getting People To Pay Their Taxes: ARTICLE FOR PUBICATION: by Timore B. FrancisDocument4 pagesGetting People To Pay Their Taxes: ARTICLE FOR PUBICATION: by Timore B. FrancisTIMOREGHNo ratings yet

- Li 1996-Bonus Tax in GhanaDocument1 pageLi 1996-Bonus Tax in GhanaTIMOREGHNo ratings yet

- Cost and Management AccountingDocument6 pagesCost and Management AccountingTIMOREGHNo ratings yet

- TaxationDocument6 pagesTaxationTIMOREGHNo ratings yet

- Sample Questions 1Document13 pagesSample Questions 1TIMOREGHNo ratings yet

- F7 TipsDocument26 pagesF7 TipsTIMOREGHNo ratings yet

- CPGA May 2011Document20 pagesCPGA May 2011TIMOREGHNo ratings yet

- Cost and Management AccountingDocument6 pagesCost and Management AccountingTIMOREGHNo ratings yet

- A Synopsis of The National Pensions Act 2008Document5 pagesA Synopsis of The National Pensions Act 2008Fred Ampomah-darkoNo ratings yet

- The Student AccountantDocument1 pageThe Student AccountantTIMOREGHNo ratings yet

- Corporate Tax RatesDocument5 pagesCorporate Tax RatesTIMOREGHNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Analysis of The Impacts of China's Foreign Direct Investment in VietnamDocument4 pagesAnalysis of The Impacts of China's Foreign Direct Investment in VietnamJenNo ratings yet

- Trade Restrictions in RussiaDocument15 pagesTrade Restrictions in Russiasayalipatil1196No ratings yet

- شروط الاستفادة من عقود الامتياز في إطار المستثمرات الفلاحية الجديدةDocument16 pagesشروط الاستفادة من عقود الامتياز في إطار المستثمرات الفلاحية الجديدةNoro BenslamaNo ratings yet

- STURCTURAL STEEL AND TMT RegisterDocument64 pagesSTURCTURAL STEEL AND TMT RegisterSalman ShahNo ratings yet

- 12th FINANCE COMMISSIONDocument2 pages12th FINANCE COMMISSIONMONIDIPA DHARNo ratings yet

- Press Release - Strengthening The Coffee Industry of Basilan Province v2Document2 pagesPress Release - Strengthening The Coffee Industry of Basilan Province v2Prince Yaz ElardoNo ratings yet

- LOS Rise SupplyDocument1 pageLOS Rise SupplyJohn Adrian Nasayao MatubaranNo ratings yet

- SWOT Analysis of Indian EconomyDocument11 pagesSWOT Analysis of Indian EconomyHarish InglikarNo ratings yet

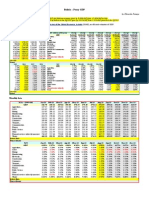

- Bolivia - Proxy GDPDocument1 pageBolivia - Proxy GDPEduardo PetazzeNo ratings yet

- FYJC Eco TERM II Question Bank 50 MarksDocument3 pagesFYJC Eco TERM II Question Bank 50 MarksPRAPTI PARMARNo ratings yet

- The Political Economy of International TradeDocument16 pagesThe Political Economy of International TradeWilsonNo ratings yet

- Sro 967 (I) 2022Document3 pagesSro 967 (I) 2022Hassan MujtabaNo ratings yet

- T1-Global MarketDocument27 pagesT1-Global Marketcristell rodriguezNo ratings yet

- Assessment of Government Influence On Exchange RatesDocument1 pageAssessment of Government Influence On Exchange Ratestrilocksp SinghNo ratings yet

- Footwear MarketDocument2 pagesFootwear MarketAkshay SinghNo ratings yet

- The Importance of Agriculture Towards The Development of Nigeria EconomyDocument1 pageThe Importance of Agriculture Towards The Development of Nigeria EconomyAKINYEMI ADISA KAMORUNo ratings yet

- Fiscal Management Reaction PaperDocument2 pagesFiscal Management Reaction PaperChristopher B. Albino100% (6)

- Foreign ExchangeDocument15 pagesForeign ExchangeAnuranjanSinha100% (1)

- Presented by Anmoldeep Anil Kumar Sanjay Singh Deepak Kumar Gursharan PreetDocument10 pagesPresented by Anmoldeep Anil Kumar Sanjay Singh Deepak Kumar Gursharan PreetRuchi GoenkaNo ratings yet

- BA Quiz PDF 25 June Copy 1Document6 pagesBA Quiz PDF 25 June Copy 1Rahul singhNo ratings yet

- Tyre Industry in IndiaDocument11 pagesTyre Industry in IndiaAlok ChowdhuryNo ratings yet

- Topic 63 Country Risk Determinants, Measures and ImplicationsDocument2 pagesTopic 63 Country Risk Determinants, Measures and ImplicationsSoumava PalNo ratings yet

- Assignment 2: Topic: Dumping and Its Impact On India With Reference To ChinaDocument16 pagesAssignment 2: Topic: Dumping and Its Impact On India With Reference To Chinarashi bakshNo ratings yet

- Absolute Advantage and Comp Cost AdvantageDocument33 pagesAbsolute Advantage and Comp Cost AdvantageWilson MorasNo ratings yet

- KashifRasool - 2333 - 16644 - 6 - Lecture 3 - International Trade Theory, Hill - 300116Document31 pagesKashifRasool - 2333 - 16644 - 6 - Lecture 3 - International Trade Theory, Hill - 300116AhmadNo ratings yet

- Tugas 1 Bahasa Inggris NiagaDocument2 pagesTugas 1 Bahasa Inggris NiagaPengawasan Kepulauan AnambasNo ratings yet

- Rejected BankDocument3 pagesRejected Banksigitsutoko8765No ratings yet

- c1 Salary BenchmarksDocument44 pagesc1 Salary BenchmarkssnhdnebdhNo ratings yet

- Examen Parcial - Semana 4: Historial de IntentosDocument11 pagesExamen Parcial - Semana 4: Historial de Intentosedgar salamancaNo ratings yet