You might also like

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Finance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiDocument43 pagesFinance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New Delhipuritansoul100% (2)

- Finance Bill 2010Document51 pagesFinance Bill 2010riddhivakhariaNo ratings yet

- Budget 2020 HighlightsDocument12 pagesBudget 2020 HighlightsPriyankaNo ratings yet

- Union Budget 2012-Income TaxDocument21 pagesUnion Budget 2012-Income TaxFinquity IndiaNo ratings yet

- RSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Document17 pagesRSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Rohan JainNo ratings yet

- @dtaxmcq Income Tax Amendment sheetDocument50 pages@dtaxmcq Income Tax Amendment sheetmshivam617No ratings yet

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 pagesCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsNo ratings yet

- FAQ On Budget FY 2020-21Document9 pagesFAQ On Budget FY 2020-21GUNANo ratings yet

- YYC July NewsletterDocument11 pagesYYC July NewsletterCatherine ChuaNo ratings yet

- The SUPER Budget AnalysisDocument15 pagesThe SUPER Budget AnalysisMahaveer DhelariyaNo ratings yet

- 80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensDocument1 page80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensArjun VermaNo ratings yet

- Tax Rates, Exemptions and AmendmentsDocument25 pagesTax Rates, Exemptions and Amendmentsanshulagarwal62No ratings yet

- Tax Updates For June 2012 ExamsDocument37 pagesTax Updates For June 2012 ExamsShanky MalhotraNo ratings yet

- 56212rtpfinaloldnov19 p7Document52 pages56212rtpfinaloldnov19 p7naveen kumarNo ratings yet

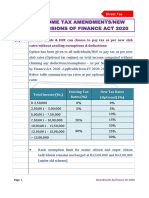

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATSamuel AnthrayoseNo ratings yet

- Amendments in Service TaxDocument15 pagesAmendments in Service TaxShankar NarayananNo ratings yet

- GST Council 43rd Meeting Key RecommendationsDocument6 pagesGST Council 43rd Meeting Key Recommendationssuhani singhNo ratings yet

- Category Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxDocument16 pagesCategory Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxshwetakuppanNo ratings yet

- Chapter 5 Composition Scheme Nov 2020Document41 pagesChapter 5 Composition Scheme Nov 2020Alka GuptaNo ratings yet

- Pawan 115ja JCDocument35 pagesPawan 115ja JCKapasi TejasNo ratings yet

- Elective Ourse in Commerce ECO-11 Elements of Income TaxDocument12 pagesElective Ourse in Commerce ECO-11 Elements of Income TaxJai GorakhNo ratings yet

- MAT and AMT ExplainedDocument17 pagesMAT and AMT ExplainedNitin ChoudharyNo ratings yet

- Paper-18 Supplementary 180221Document109 pagesPaper-18 Supplementary 180221Srihari SrinivasNo ratings yet

- Understanding On: Tax Audit U/s 44AB of I.T. ActDocument29 pagesUnderstanding On: Tax Audit U/s 44AB of I.T. Actspchheda4996No ratings yet

- Tax benefits for electricity generation under section 115BABDocument27 pagesTax benefits for electricity generation under section 115BABABC 123No ratings yet

- AFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)Document14 pagesAFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)salahuddin ahmedNo ratings yet

- Mat - PPT FinalDocument18 pagesMat - PPT FinalAkash PatelNo ratings yet

- Draft File (Shafin)Document11 pagesDraft File (Shafin)MD Shafin AhmedNo ratings yet

- AMENDMENTS – NOV 2020Document30 pagesAMENDMENTS – NOV 2020Afnan KhanNo ratings yet

- Composition SchemeDocument4 pagesComposition Schemecloudstorage567No ratings yet

- Income Tax ActDocument4 pagesIncome Tax ActgoborgonesNo ratings yet

- Imprtant Points-Sales Tax 2016-17 PDFDocument2 pagesImprtant Points-Sales Tax 2016-17 PDFEngr Siraj RahmdilNo ratings yet

- Critical Analysis of Income Tax Ordinance 2010Document16 pagesCritical Analysis of Income Tax Ordinance 2010Dilnawaz KhanNo ratings yet

- Minimum Alternate Tax MAT PDFDocument6 pagesMinimum Alternate Tax MAT PDFmuskan khatriNo ratings yet

- It Goi Note On Mat and AmtDocument17 pagesIt Goi Note On Mat and AmtKapil AroraNo ratings yet

- Decoding Indian Union Budget Finance Bil PDFDocument7 pagesDecoding Indian Union Budget Finance Bil PDFkumarNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- 10.mat and AmtDocument17 pages10.mat and AmtShailendra SainwalNo ratings yet

- BDO Budget Snapshot - 2012-13Document9 pagesBDO Budget Snapshot - 2012-13Pulluri Ravikumar YugandarNo ratings yet

- AMT - Know About Alternative Minimum Tax Applicability, Exemptions, Credits & MoreDocument8 pagesAMT - Know About Alternative Minimum Tax Applicability, Exemptions, Credits & MoreRudrin DasNo ratings yet

- New Income Tax provisions under Finance Act 2020Document26 pagesNew Income Tax provisions under Finance Act 2020Piyush HarlalkaNo ratings yet

- Budget 2013 - 2014Document11 pagesBudget 2013 - 2014sdfdhgtj894No ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Uganda Tax Amendment Bills For 2018Document10 pagesUganda Tax Amendment Bills For 2018jadwongscribdNo ratings yet

- Tax Icsi 2012Document84 pagesTax Icsi 2012Janani ParameswaranNo ratings yet

- Overview of Key Changes to Income Tax Provisions Under TRAIN ActDocument49 pagesOverview of Key Changes to Income Tax Provisions Under TRAIN ActFaith FernandezNo ratings yet

- The Budget 2011 - A Glimpse: Shetty Prabhu & AshokDocument15 pagesThe Budget 2011 - A Glimpse: Shetty Prabhu & AshokMadhusudan MagajiNo ratings yet

- Bos 45290Document23 pagesBos 45290CA Kashish MittalNo ratings yet

- When Will The New Scheme Be Applicable?: Faqs On Budget Fy 2020-21Document6 pagesWhen Will The New Scheme Be Applicable?: Faqs On Budget Fy 2020-21Biswabandhu PalNo ratings yet

- Comparative Analysis of Financial Bills: C C C CCDocument5 pagesComparative Analysis of Financial Bills: C C C CCpdabriwalNo ratings yet

- Commentary On Impact of Finance Bill 2022 On IT SectorDocument10 pagesCommentary On Impact of Finance Bill 2022 On IT SectorurcapkNo ratings yet

- KPMG - Change in Tax Audit ReportDocument5 pagesKPMG - Change in Tax Audit ReportDhananjay KulkarniNo ratings yet

- Budget Highlights 2012Document9 pagesBudget Highlights 2012Anshul GuptaNo ratings yet

- Overview of Key Amendments to the Philippine Tax Code under the TRAIN LawDocument28 pagesOverview of Key Amendments to the Philippine Tax Code under the TRAIN LawScarlette CooperaNo ratings yet

- Tax Laws Practice New Syl Lab Us 06032024Document54 pagesTax Laws Practice New Syl Lab Us 06032024coolboydeepak4No ratings yet

- Amendment 2080-2081Document13 pagesAmendment 2080-2081Neeraj GuptaNo ratings yet

- Minimum Alternate TaxDocument20 pagesMinimum Alternate Taxapi-3832224100% (2)

- TRAIN Briefing - Income TaxDocument48 pagesTRAIN Briefing - Income TaxLovely MagdipigNo ratings yet