You might also like

- Studies in Tape ReadingDocument204 pagesStudies in Tape ReadingDerek Fong100% (9)

- Indian Financial SystemDocument107 pagesIndian Financial SystemAkram Hasan89% (9)

- IntroductionDocument6 pagesIntroductionCarol SilveiraNo ratings yet

- SENSEX - The Barometer of Indian Capital Markets: Dollex Series of BSE Indices'Document6 pagesSENSEX - The Barometer of Indian Capital Markets: Dollex Series of BSE Indices'yraghav_1No ratings yet

- SENSEX - The Barometer of Indian Capital MarketsDocument7 pagesSENSEX - The Barometer of Indian Capital MarketsSachin KingNo ratings yet

- SENSEX - The Barometer of Indian Capital MarketsDocument7 pagesSENSEX - The Barometer of Indian Capital MarketsSandeep S SalviNo ratings yet

- Free Float IndexDocument8 pagesFree Float IndexJaishalNo ratings yet

- Submitted by V.Uthra 1091057: What Are The Criteria Applied To Include Stocks in BseDocument12 pagesSubmitted by V.Uthra 1091057: What Are The Criteria Applied To Include Stocks in BseUthra VijayNo ratings yet

- Financial Market CH - 2Document53 pagesFinancial Market CH - 2amita_singhNo ratings yet

- Calculation of Sensex: Submitted by Ashish GargDocument10 pagesCalculation of Sensex: Submitted by Ashish Gargashishanilgarg100% (3)

- Chapter 6Document5 pagesChapter 6kamma1No ratings yet

- Stock MarketDocument12 pagesStock MarketMuhammad Saleem SattarNo ratings yet

- ProjectDocument80 pagesProjectShameem AnwarNo ratings yet

- SENSEX - The Barometer of Indian Capital Markets: Index SpecificationDocument25 pagesSENSEX - The Barometer of Indian Capital Markets: Index SpecificationsathwickbNo ratings yet

- How To Calculate The Value of The Sensitive IndexDocument6 pagesHow To Calculate The Value of The Sensitive IndexMohankumarpgdmNo ratings yet

- Correlation Between NSE and BSE Indices: Project Work OnDocument27 pagesCorrelation Between NSE and BSE Indices: Project Work OnKishan SekhadaNo ratings yet

- Stock Market Indicies AssingmentDocument11 pagesStock Market Indicies AssingmenttullipsNo ratings yet

- KSE - 30 IndexDocument21 pagesKSE - 30 IndexNadeem uz Zaman100% (1)

- Kse - 30 Index Based On Free-Float: The Karachi Stock Exchange (Guarantee) LimitedDocument21 pagesKse - 30 Index Based On Free-Float: The Karachi Stock Exchange (Guarantee) LimitedJan Muhammad MemonNo ratings yet

- Method Nifty 50Document16 pagesMethod Nifty 50Richard JonesNo ratings yet

- Q.1 Frame The Investment Process For A Person of Your Age GroupDocument5 pagesQ.1 Frame The Investment Process For A Person of Your Age GroupNikhil KeshavNo ratings yet

- Method Nifty 50Document16 pagesMethod Nifty 50divyajeetNo ratings yet

- Nifty 50: Index MethodologyDocument14 pagesNifty 50: Index MethodologyAkshay AgarwalNo ratings yet

- Introduction To MFDocument52 pagesIntroduction To MFAnupam MardhekarNo ratings yet

- Stock Market Indices (BBA)Document5 pagesStock Market Indices (BBA)Akshita DhyaniNo ratings yet

- Security Analysis and Portfolio Management: Presented By: OmkarDocument25 pagesSecurity Analysis and Portfolio Management: Presented By: Omkarpatil0055No ratings yet

- Indian Stock Exchanges and How Their Indices Are CalculatedDocument30 pagesIndian Stock Exchanges and How Their Indices Are CalculatedAapnijche FakeidNo ratings yet

- A Study On Mutual Funds in IndiaDocument31 pagesA Study On Mutual Funds in Indianikhil5822No ratings yet

- A Study On Mutual Funds in IndiaDocument18 pagesA Study On Mutual Funds in IndiarnbiswalNo ratings yet

- A Study On Mutual Funds in IndiaDocument17 pagesA Study On Mutual Funds in IndiaAlok ShahNo ratings yet

- How Have Mutual Funds Been ClassifiedDocument7 pagesHow Have Mutual Funds Been Classifiedritvik singh rautelaNo ratings yet

- Nifty 50: Index MethodologyDocument16 pagesNifty 50: Index MethodologyObhiejitNo ratings yet

- PSX Indices AssDocument7 pagesPSX Indices AssFlourish edible CrockeryNo ratings yet

- ACF Report Sec D Group 7Document11 pagesACF Report Sec D Group 7Amit JhaNo ratings yet

- A Study On Mutual Funds in IndiaDocument32 pagesA Study On Mutual Funds in IndiaAbhranil DasNo ratings yet

- MF0010 - Sem 3 - Fall 2011Document7 pagesMF0010 - Sem 3 - Fall 2011Sonal PomalNo ratings yet

- NBPPGI Index BrochureDocument10 pagesNBPPGI Index BrochureHadia SarwarNo ratings yet

- SensexDocument24 pagesSensexAmit MittalNo ratings yet

- A Study On Price Volatility in The Stocks of BseDocument6 pagesA Study On Price Volatility in The Stocks of BseNicole PayneNo ratings yet

- InvestmentDocument78 pagesInvestmentSanchita NaikNo ratings yet

- A Study On Mutual Funds in IndiaDocument40 pagesA Study On Mutual Funds in IndiaYaseer ArafathNo ratings yet

- Bse FunctionsDocument41 pagesBse FunctionsSree LakshmiNo ratings yet

- Biswal01 03Document8 pagesBiswal01 03mrugenNo ratings yet

- Stock Index of Bangladesh Stock MarketDocument9 pagesStock Index of Bangladesh Stock MarketFuhad AhmedNo ratings yet

- Executive SummaryDocument17 pagesExecutive SummarySiva GuruNo ratings yet

- Stock Market Indices in India: Raghunandan HelwadeDocument38 pagesStock Market Indices in India: Raghunandan HelwadeRaghunandan HelwadeNo ratings yet

- Project Report On: "Computation of Indices (Sensex and Nifty) "Document61 pagesProject Report On: "Computation of Indices (Sensex and Nifty) "raayya100% (1)

- Master of Business Administration: Third Semester MF0010Document15 pagesMaster of Business Administration: Third Semester MF0010Rajesh PhulwaniNo ratings yet

- 1.equity Market & Equity Valuation PDFDocument11 pages1.equity Market & Equity Valuation PDFRajeev KNo ratings yet

- Stock Index of Stock Market in Bangladesh PDFDocument11 pagesStock Index of Stock Market in Bangladesh PDFSajeed Mahmud MaheeNo ratings yet

- Indian Stock Exchanges and How Their Indices Are CalculatedDocument30 pagesIndian Stock Exchanges and How Their Indices Are CalculatedKirron ThakurNo ratings yet

- 1.1 General Introduction: Security AssetsDocument20 pages1.1 General Introduction: Security AssetschenchukalNo ratings yet

- Finance ConceptsDocument2 pagesFinance Conceptssandesh_mnitNo ratings yet

- Nifty, Sensex A Long Way From Truly Representing The EconomyDocument22 pagesNifty, Sensex A Long Way From Truly Representing The Economyharsh_monsNo ratings yet

- Sen SexDocument4 pagesSen Sexvaibs14No ratings yet

- Index Number Formation in The Chittagong Stock ExchangeDocument12 pagesIndex Number Formation in The Chittagong Stock ExchangeSakibSourovNo ratings yet

- Dissertation, BBADocument37 pagesDissertation, BBAGarvit AgarwalNo ratings yet

- Digital Assignment 2Document7 pagesDigital Assignment 2Prithish PreeNo ratings yet

- Studt of Mutual Fund in India Final ProjectDocument38 pagesStudt of Mutual Fund in India Final ProjectjitendraouatNo ratings yet

- Stock Market Income Genesis: Internet Business Genesis Series, #8From EverandStock Market Income Genesis: Internet Business Genesis Series, #8No ratings yet

- Technical AnalysisDocument31 pagesTechnical AnalysismubinNo ratings yet

- Ipru Value Discovery FundDocument4 pagesIpru Value Discovery FundJ.K. GarnayakNo ratings yet

- Accounting Vol. IIDocument405 pagesAccounting Vol. IISaibhumi100% (3)

- Dr. Ram Manohar Lohiya National Law University Lucknow: Monetary Policy of The Reserve Bank of India: An AnalysisDocument17 pagesDr. Ram Manohar Lohiya National Law University Lucknow: Monetary Policy of The Reserve Bank of India: An AnalysisGarima ParakhNo ratings yet

- Proposed Counsel To The Debtors and Debtors-in-Possession: United States Bankruptcy Court Southern District of New YorkDocument85 pagesProposed Counsel To The Debtors and Debtors-in-Possession: United States Bankruptcy Court Southern District of New Yorkgreeen.pat6918No ratings yet

- The Institute of Bankers Pakistan: Sample PaperDocument6 pagesThe Institute of Bankers Pakistan: Sample PaperMasaab KhanNo ratings yet

- "Fuelling" Engines : Initiating CoverageDocument16 pages"Fuelling" Engines : Initiating CoverageGajendra BurhadeNo ratings yet

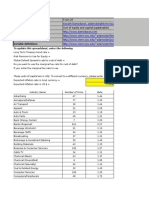

- Date Updated: Created By: What Is This Data? Home Page: Data Website: Companies in Each Industry: Variable DefinitionsDocument15 pagesDate Updated: Created By: What Is This Data? Home Page: Data Website: Companies in Each Industry: Variable DefinitionsPedro CooperNo ratings yet

- A Clear Understanding of The Industry: Is Cfa Institute Investment Foundations Right For You?Document17 pagesA Clear Understanding of The Industry: Is Cfa Institute Investment Foundations Right For You?SAHIL GUPTANo ratings yet

- Bindal FX Trading Plan Template PDFDocument13 pagesBindal FX Trading Plan Template PDFf2662961100% (1)

- 01 - Global Finantial MarketsDocument16 pages01 - Global Finantial MarketsManjuNo ratings yet

- Vodafone Idea MergerDocument20 pagesVodafone Idea MergerCyvita Veigas100% (1)

- Assignment #5: Currency Value FundDocument3 pagesAssignment #5: Currency Value Fundgoot11No ratings yet

- FPA SystemDocument21 pagesFPA SystemVicaas VSNo ratings yet

- SEBI Slaps Rs 50 Lakh Fine On 6 Entities For Fraudulent Trade in Polar Pharma Shares - The New Indian ExpressDocument10 pagesSEBI Slaps Rs 50 Lakh Fine On 6 Entities For Fraudulent Trade in Polar Pharma Shares - The New Indian ExpressSachinNo ratings yet

- UBS WM - Equity Model Portfolios - What's Changing - June 2019Document3 pagesUBS WM - Equity Model Portfolios - What's Changing - June 2019Blue RunnerNo ratings yet

- The Meaning of Foreign ExchangeDocument5 pagesThe Meaning of Foreign ExchangeRohini ManiNo ratings yet

- Ch17 - Analysis of Bonds W Embedded Options.ADocument25 pagesCh17 - Analysis of Bonds W Embedded Options.Akerenkang100% (1)

- Corporate Governance and The Financial Crisis: What Have We Missed?Document15 pagesCorporate Governance and The Financial Crisis: What Have We Missed?Tarun SinghNo ratings yet

- Induction RMDocument22 pagesInduction RMkabaatNo ratings yet

- The Role of A Corporate Governance Task Force - ShabrawishiDocument23 pagesThe Role of A Corporate Governance Task Force - ShabrawishirahimsajedNo ratings yet

- Swot Analysis of Asset ClassesDocument3 pagesSwot Analysis of Asset ClassesAmal JoyNo ratings yet

- Ventura Securities Limited CIN No: U67120MH1994PLC082048Document2 pagesVentura Securities Limited CIN No: U67120MH1994PLC082048Pranav PatilNo ratings yet

- Chap7 AnsDocument9 pagesChap7 AnsJane MingNo ratings yet

- CORPORATE GOVERNANCE Subex LimitedDocument4 pagesCORPORATE GOVERNANCE Subex LimitedBhawana SaloneNo ratings yet

- Blackrock PeriodicDocument2 pagesBlackrock Periodicsameer1987kazi4405No ratings yet

- 137.COSV: Council of Orthodox Synagogues of Victoria LTD: Current & Historical Company ExtractDocument9 pages137.COSV: Council of Orthodox Synagogues of Victoria LTD: Current & Historical Company ExtractFlinders TrusteesNo ratings yet