You might also like

- PdfjoinerDocument115 pagesPdfjoinerAnisha SapraNo ratings yet

- Lesson 7 Bull Call SpreadDocument14 pagesLesson 7 Bull Call Spreadadms100% (3)

- Bull Spread Spread: Montréal ExchangeDocument2 pagesBull Spread Spread: Montréal ExchangepkkothariNo ratings yet

- TSD H4 4majorsDocument3 pagesTSD H4 4majorsapi-3713613No ratings yet

- McDonald Chapter2Document9 pagesMcDonald Chapter2kalus00123100% (1)

- Coupon 6% P.A. - American Barrier at 70% - 1 Year - CHF: Single Barrier Reverse Convertible On Julius BaerDocument1 pageCoupon 6% P.A. - American Barrier at 70% - 1 Year - CHF: Single Barrier Reverse Convertible On Julius Baerapi-25889552No ratings yet

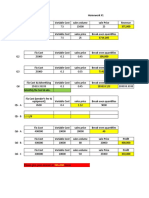

- HW Fin431Document2 pagesHW Fin431Shoaib Iftekhar ShakilNo ratings yet

- Breakeven Calculator: Options Equity/ FuturesDocument3 pagesBreakeven Calculator: Options Equity/ FuturescnsatishNo ratings yet

- Portfolio Revision PDFDocument15 pagesPortfolio Revision PDFMr. Shopper NepalNo ratings yet

- Final Exam: Derivatives and Risk ManagementDocument29 pagesFinal Exam: Derivatives and Risk ManagementTrang Nguyễn Hoàng LêNo ratings yet

- Bear Spread Spread: Montréal ExchangeDocument2 pagesBear Spread Spread: Montréal ExchangepkkothariNo ratings yet

- Covered Ratio SpreadDocument2 pagesCovered Ratio SpreadpkkothariNo ratings yet

- Lesson 03 The Iron CondorDocument14 pagesLesson 03 The Iron CondorMahesh Kumar100% (3)

- MetcryptoDocument15 pagesMetcryptocharles LeeNo ratings yet

- Lesson 8 Bear Put SpreadDocument14 pagesLesson 8 Bear Put Spreadrishab kumarNo ratings yet

- Bear Put Spread: Montréal ExchangeDocument2 pagesBear Put Spread: Montréal ExchangepkkothariNo ratings yet

- Ways of Earnings ComputationsDocument37 pagesWays of Earnings Computationsedu manabatNo ratings yet

- Statement - 66400325 - Muhammad FatimahDocument1 pageStatement - 66400325 - Muhammad FatimahKhadija AminNo ratings yet

- KAS Vertical SpreadsDocument34 pagesKAS Vertical SpreadsPriyanashi Jain100% (3)

- What Is Double Diagonal Spread - FidelityDocument8 pagesWhat Is Double Diagonal Spread - FidelityanalystbankNo ratings yet

- Decision TreeDocument9 pagesDecision TreeSudhanshu Verma100% (1)

- Strategy Tester EA HOUR JOE FEBRUARI 2022Document7 pagesStrategy Tester EA HOUR JOE FEBRUARI 2022Nor NofalNo ratings yet

- Short Butterfly Spread With Puts - FidelityDocument7 pagesShort Butterfly Spread With Puts - FidelityanalystbankNo ratings yet

- Revenue Decision in Perfect CompetitionDocument16 pagesRevenue Decision in Perfect CompetitionShreyansh DabhadiyaNo ratings yet

- Short Condor Spread With Puts - FidelityDocument7 pagesShort Condor Spread With Puts - FidelityanalystbankNo ratings yet

- Futures Margin CalculationDocument79 pagesFutures Margin CalculationMUSKAAN BAHLNo ratings yet

- Problem 1 Grading ExplanationDocument1 pageProblem 1 Grading ExplanationIqra MunawarNo ratings yet

- Decision-Making Using Probability: 6.1 Expected Monetary ValueDocument8 pagesDecision-Making Using Probability: 6.1 Expected Monetary ValueJaya sankarNo ratings yet

- HW1 - Answer - Sheet - 1Document6 pagesHW1 - Answer - Sheet - 1Harry McLinnahanNo ratings yet

- December 2007: Past Papers - Examiner's SolutionsDocument7 pagesDecember 2007: Past Papers - Examiner's SolutionsSijanPokharelNo ratings yet

- Note On Combinations of Options, Futures and Stocks (Module 2, Part B)Document21 pagesNote On Combinations of Options, Futures and Stocks (Module 2, Part B)Anosh ModyNo ratings yet

- Modified Put Butterfly - FidelityDocument6 pagesModified Put Butterfly - FidelityNarendra BholeNo ratings yet

- Month To Month Number of Months Cost of Subscription Number of Subscriptions Sold 1 10 20 6 45 15 12 100 1Document3 pagesMonth To Month Number of Months Cost of Subscription Number of Subscriptions Sold 1 10 20 6 45 15 12 100 1Brandon SNo ratings yet

- Covered Calls Are The Same As Cash-Secured PutsDocument4 pagesCovered Calls Are The Same As Cash-Secured PutspkkothariNo ratings yet

- Trader's Destination Intraday Calculators: Edit The Cells in Black Only, Dont Edit Any Other CellsDocument2 pagesTrader's Destination Intraday Calculators: Edit The Cells in Black Only, Dont Edit Any Other CellsKubera TradeNo ratings yet

- BMAN20072 Week 9 Problem Set 2021 - SolutionDocument4 pagesBMAN20072 Week 9 Problem Set 2021 - SolutionAlok AgrawalNo ratings yet

- Options Strategies Quick GuideDocument36 pagesOptions Strategies Quick GuideParikshit KalyankarNo ratings yet

- Coupon 6% P.A. - American Barrier at 80% - 3 Months - EUR: Single Barrier Reverse Convertible On ARCELORMITTALDocument1 pageCoupon 6% P.A. - American Barrier at 80% - 3 Months - EUR: Single Barrier Reverse Convertible On ARCELORMITTALapi-25889552No ratings yet

- Case 1Document3 pagesCase 1Naveen AttigeriNo ratings yet

- Coupon 9% P.A. - American Barrier at 70% - 1 Year - EUR: Single Barrier Reverse Convertible On DEUTSCHE BANKDocument1 pageCoupon 9% P.A. - American Barrier at 70% - 1 Year - EUR: Single Barrier Reverse Convertible On DEUTSCHE BANKapi-25889552No ratings yet

- Derivatives & Risk MGMTDocument25 pagesDerivatives & Risk MGMTAdityaraj PhadnisNo ratings yet

- Scalping EA - GOLD 30M Back Test ReportDocument2 pagesScalping EA - GOLD 30M Back Test ReporthussainNo ratings yet

- Short Butterfly Spread With Calls - FidelityDocument8 pagesShort Butterfly Spread With Calls - FidelityanalystbankNo ratings yet

- FIS 2020-21 End Term AnswerDocument6 pagesFIS 2020-21 End Term AnswerAaryan SarupriaNo ratings yet

- Short Condor Spread With Calls - FidelityDocument7 pagesShort Condor Spread With Calls - Fidelityanalystbank100% (1)

- DRM IntroDocument61 pagesDRM IntroMukul BaviskarNo ratings yet

- Position SizingDocument5 pagesPosition SizingAbbas MuhammadNo ratings yet

- Repair and Exit StrategiesDocument34 pagesRepair and Exit StrategiesaporatNo ratings yet

- Covered Call Option Strategy: Mechanics of Covered CallsDocument3 pagesCovered Call Option Strategy: Mechanics of Covered CallsSamuel MillerNo ratings yet

- DRM Chapter 3 OptionsDocument125 pagesDRM Chapter 3 OptionsJohn MichaelNo ratings yet

- Chap 007Document19 pagesChap 007Anass B100% (1)

- Key Options Strategy GuideDocument18 pagesKey Options Strategy GuideAngelo PosillicoNo ratings yet

- International Financial ManagementDocument8 pagesInternational Financial ManagementAhmed Abdul-AzizNo ratings yet

- Methods of Buyback - Bookbuilding MethodDocument1 pageMethods of Buyback - Bookbuilding MethodMukesh MewaraNo ratings yet

- KearneyCredit Spreads WebinarDocument33 pagesKearneyCredit Spreads WebinarsamNo ratings yet

- Problem 1:-: SolutionsDocument6 pagesProblem 1:-: SolutionsSai kiranNo ratings yet

- Coupon 5.25% P.A. - American Barrier at 69% - 1 Year - CHF: Single Barrier Reverse Convertible On SYNGENTA AG-REGDocument1 pageCoupon 5.25% P.A. - American Barrier at 69% - 1 Year - CHF: Single Barrier Reverse Convertible On SYNGENTA AG-REGapi-25889552No ratings yet

- Capital OneDocument4 pagesCapital OneArunothai RattananorasateNo ratings yet

- Tax Saving (ELSS) Statement: Bijoy DuttaDocument1 pageTax Saving (ELSS) Statement: Bijoy DuttaBijoy DuttaNo ratings yet

- Quiz 1 Partnership AnswersDocument4 pagesQuiz 1 Partnership Answersdianel villarico100% (2)

- SBR - Mock A - AnswersDocument14 pagesSBR - Mock A - AnswersDylan MutambanengweNo ratings yet

- Banking Laws and RegulationDocument19 pagesBanking Laws and RegulationAbdullah ZakariyyaNo ratings yet

- Int AccDocument37 pagesInt AccjoeywuykNo ratings yet

- Abin Corrected Converted - pdf2Document62 pagesAbin Corrected Converted - pdf2jbum93257No ratings yet

- FG2233Document11 pagesFG2233Hassan Sheikh0% (1)

- The Weekly Peak: Peak Theories Research LLCDocument6 pagesThe Weekly Peak: Peak Theories Research LLCfcamargoeNo ratings yet

- CH 09Document63 pagesCH 09Utsav DubeyNo ratings yet

- QuickBooks Online Core Certification Exercise Book V22.4.1Document28 pagesQuickBooks Online Core Certification Exercise Book V22.4.1Shirshah LashkariNo ratings yet

- ProfessionalLoanTermsAndConditions PDFDocument20 pagesProfessionalLoanTermsAndConditions PDFAkash PanwarNo ratings yet

- Registration and Stamps Department (Commercial Tax) Madhya PradeshDocument1 pageRegistration and Stamps Department (Commercial Tax) Madhya PradeshVipul ShrivastvaNo ratings yet

- 800 Super Report PDFDocument19 pages800 Super Report PDFChua Qi NengNo ratings yet

- 06 Feb 2024 - 451362AccStmtDownloadReport 1 4Document4 pages06 Feb 2024 - 451362AccStmtDownloadReport 1 4mohammedNo ratings yet

- Cost of Capital Final Ppt1Document12 pagesCost of Capital Final Ppt1Mehul ShuklaNo ratings yet

- Debt Recovery Agency in IndiaDocument22 pagesDebt Recovery Agency in Indiarecreatecredit CollectionsNo ratings yet

- 1E SLATER-SIMPLE DISCOUNT Vye TO POSTDocument31 pages1E SLATER-SIMPLE DISCOUNT Vye TO POSTJohn Arlo SanchezNo ratings yet

- Siddharth Canara 17733213733Document3 pagesSiddharth Canara 17733213733SiddharthNo ratings yet

- Participant's Note - Meaning and Scope of Supply and Time and Valuation of SupplyDocument20 pagesParticipant's Note - Meaning and Scope of Supply and Time and Valuation of SupplyaskNo ratings yet

- EconomicsDocument12 pagesEconomicsASMARA HABIBNo ratings yet

- Aug 2021 G E Army Peshawar: Cnic No: 12345-6789012-3Document1 pageAug 2021 G E Army Peshawar: Cnic No: 12345-6789012-3Mehtab MalikNo ratings yet

- 5.2. Investmnt-FunctionDocument21 pages5.2. Investmnt-FunctionAbhishek VermaNo ratings yet

- UCC Tradeline ProcessDocument16 pagesUCC Tradeline ProcessTyrone Brown100% (3)

- Craig Hayward - 2021 - 1065 - K1 3Document6 pagesCraig Hayward - 2021 - 1065 - K1 3Craig HaywardNo ratings yet

- Menton Bank: The New Focus On Customer Service at Menton BankDocument9 pagesMenton Bank: The New Focus On Customer Service at Menton BankmiladNo ratings yet

- Auditing Problem Cash and Cash Equivalent - Compress 1Document19 pagesAuditing Problem Cash and Cash Equivalent - Compress 1Vianney Claire RabeNo ratings yet

- 5010 Ohada Fin Reporting p2Document12 pages5010 Ohada Fin Reporting p2serge folegweNo ratings yet

- Bench - Co Income Statement Excel TemplateDocument31 pagesBench - Co Income Statement Excel TemplateMay CañebaNo ratings yet

- MBA 806 Corporate Finance 01 and 02Document22 pagesMBA 806 Corporate Finance 01 and 02ALPASLAN TOKERNo ratings yet