Professional Documents

Culture Documents

Project Report: Submitted By: Submitted To: Shobhna Jain Mrs. Sandhya

Project Report: Submitted By: Submitted To: Shobhna Jain Mrs. Sandhya

Uploaded by

arpanbaisggnOriginal Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Project Report: Submitted By: Submitted To: Shobhna Jain Mrs. Sandhya

Project Report: Submitted By: Submitted To: Shobhna Jain Mrs. Sandhya

Uploaded by

arpanbaisggnCopyright:

Available Formats

Page | 1

PROJECT REPORT

On

Corporate finance

Submitted by: Submitted to:

Shobhna jain Mrs. Sandhya

(pgp sectoral) Prakash

Page | 2

1.1 Introduction

Corporate finance dealing with financial decisions business enterprises

make and the tools and analysis used to make these decisions. The primary

goal of corporate finance is to maximize corporate value while managing the

firm's financial risks. Although it is in principle different from managerial

finance which studies the financial decisions of all firms, rather than

corporations alone, the main concepts in the study of corporate finance are

applicable to the financial problems of all kinds of firms.

In July 1999, Carleton "Carly" Fiorina assumed the position of CEO of

Hewlett-Packard (HP). Investors were pleased with her view of HP's future:

She promised 15 percent annual growth in sales and earnings, quite a goal for a

company with five consecutive years of declining revenue. Ms. Fiorina also

changed the way HP was run. Rather than continuing to operate as separate

product groups, which essentially meant the company operated as dozens of

mini companies, Ms. Fiorina reorganized the company into just two divisions.

In 2002, HP announced that it would merge with Compaq Computers.

However, in one of the more acrimonious corporate battles in recent history, a

group led by Walter Hewlett, son of one of HP's cofounders, fought against the

merger. Ms. Fiorina ultimately prevailed, and the merger took place. With

Compaq in the fold, the company began a two-pronged strategy. It would

compete with Dell in the lower-cost, more commodity-like personal computer

segment and with IBM in the more specialized, high end computing market.

Unfortunately for HP's shareholders, Ms. Fiorina's strategy did not work out as

planned, and in February 2005, under pressure from HP's board of directors,

Ms. Fiorina resigned her position as CEO. Evidently, investors also felt a

change in direction was a good idea; HP's stock price jumped almost seven

percent the day the resignation was announced.

Understanding Ms. Fiorina's rise from corporate executive to chief

executive officer, and finally, ex-employee, takes us into issues involving the

corporate form of organization, corporate goals, and corporate control.

The discipline can be divided into long-term and short-term decisions

and techniques. Capital investment decisions are long-term choices about

which projects receive investment, whether to finance that investment with

equity or debt, and when or whether to pay dividends to shareholders. On the

other hand, the short term decisions can be grouped ". This subject deals with

Page | 3

the short-term balance of current assets and current liabilities; the focus here is

on managing cash, inventories, and short-term borrowing and lending (such as

the terms on credit extended to customers).

The terms corporate finance and corporate financier are also associated

with investment banking. The typical role of an investment bank is to evaluate

the company's financial needs and raise the appropriate type of capital that best

fits those needs.

Page | 4

2.2 Structure of Corporate Finance

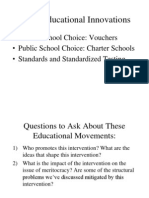

MAXIMIZE THE

VALUE

OF THE BUSINESS

(FIRM)

The Investment Declslon

Invest ln ussets thut eurn

u return greuter thut the

mlnlmum ucceptuble

hurdle rute

The Flnunclng Declslon

Flnd the rlght klnd of debt

for your flrm und the rlght

mix of debt and equity to

fund your operations

The Flnunclng Declslon

Flnd the rlght klnd of debt

for your flrm und the rlght

mlx of debt und equlty to

fund your operutlons

The hurdle

rute should

reflect the

rlsklness of the

lnvestment

und the mlx of

debt und

equlty used to

fund lt

The return

should reflect

the mugnltude

und the tlmlng

of the cush

flows us well

us ull slde

effects

The optlmul

mlx of debt

und equlty

muxlmlzes

flrm vulue

The rlght

klnd of debt

mutches the

tenor of your

ussets

How much

cush you cun

return

depends on

current und

potentlul

lnvestment

opportunltles

How you

choose to

return cush to

the owners

wlll depend on

whether they

prefer

dlvldends or

buybucks

Page | 5

1.3 WHAT IS CORPORATE FINANCE?

Suppose you decide to start a firm to make tennis balls. To do this, you

hire managers to buy raw materials, and you assemble a workforce that will

produce and sell finished tennis balls. In the language of finance, you make an

investment in assets such as inventory, machinery, land, and labor. The amount

of cash you invest in assets must be matched by an equal amount of cash raised

by financing. When you begin to sell tennis balls, your firm will generate cash.

This is the basis of value creation. The purpose of the firm is to create value for

you, the owner. The value is reflected in the framework of the simple balance

sheet model of the firm. Following Factor have to be consider before making

the Corporate Finance.

Capital investment decisions

Capital investment decisions are long-term corporate finance decisions

relating to fixed assets and capital structure. Decisions are based on several

inter-related criteria. (1) Corporate management seeks to maximize the value

of the firm by investing in projects which yield a positive net present value

when valued using an appropriate discount rate. (2) These projects must also

be financed appropriately. (3) If no such opportunities exist, maximizing

shareholder value dictates that management must return excess cash to

shareholders (i.e., distribution via dividends). Capital investment decisions

thus comprise an investment decision, a financing decision, and a dividend

decision.

Valuing flexibility

In many cases, for example R&D projects, a project may open or close) paths

of action to the company, but this reality will not typically be captured in a

strict NPV approach. Management will therefore (sometimes) employ tools

which place an explicit value on these options. So, whereas in a DCF valuation

the most likely or average or scenario specific cash flows are discounted, here

the flexible and staged nature of the investment is modeled, and hence "all"

potential payoffs are considered. The difference between the two valuations is

the "value of flexibility" inherent in the project. The two most common tools

are Decision Tree Analysis (DTA) and Real options analysis (ROA); they may

often be used interchangeably:

Page | 6

DTA values flexibility by incorporating possible events (or states) and

consequent management decisions. (For example, a company would build a

factory given that demand for its product exceeded a certain level during the

pilot-phase, and outsource production otherwise. In turn, given further

demand, it would similarly expand the factory, and maintain it otherwise. In

a DCF model, by contrast, there is no "branching" - each scenario must be

modeled separately.) In the decision tree, each management decision in

response to an "event" generates a "branch" or "path" which the company

could follow; the probabilities of each event are determined or specified by

management. Once the tree is constructed: (1) "all" possible events and their

resultant paths are visible to management; (2) given this knowledge of the

events that could follow, and assuming rational decision making,

management chooses the actions corresponding to the highest value path

probability weighted; (3) this path is then taken as representative of project

value. See Decision theory: Choice under uncertainty.

ROA is usually used when the value of a project is contingent on the value

of some other asset or underlying variable. (For example, the viability of a

mining project is contingent on the price of gold; if the price is too low,

management will abandon the mining rights, if sufficiently high,

management will develop the ore body. Again, a DCF valuation would

capture only one of these outcomes.) Here: (1) using financial option theory

as a framework, the decision to be taken is identified as corresponding to

either a call option or a put option; (2) an appropriate valuation technique is

then employed - usually a variant on the Binomial options model or a

bespoke simulation model, while Black Sholes type formulae are used less

often; see Contingent claim valuation. (3) The "true" value of the project is

then the NPV of the "most likely" scenario plus the option value. (Real

options in corporate finance were first discussed by Stewart Myers in 1977;

viewing corporate strategy as a series of options was originally per Timothy

Luehrman, in the late 1990s.)

The Financing Decision

Achieving the goals of corporate finance requires that any corporate

investment be financed appropriately. As above, since both hurdle rate and

cash flows (and hence the riskiness of the firm) will be affected, the

financing mix can impact the valuation. Management must therefore identify

the "optimal mix" of financingthe capital structures those results in

Page | 7

maximum value. (See Balance sheet, WACC, Fisher separation theorem;

but, see also the Modigliani-Miller theorem.).

The sources of financing will, generically, comprise some

combination of debt and equity financing. Financing a project through debt

results in a liability or obligation that must be serviced, thus entailing cash

flow implications independent of the project's degree of success. Equity

financing is less risky with respect to cash flow commitments, but results in

a dilution of ownership, control and earnings. The cost of equity is also

typically higher than the cost of debt (see CAPM and WACC), and so equity

financing may result in an increased hurdle rate which may offset any

reduction in cash flow risk. Management must also attempt to match the

financing mix to the asset being financed as closely as possible, in terms of

both timing and cash flows.

One of the main theories of how firms make their financing decisions

is the Pecking Order Theory, which suggests that firms avoid external

financing while they have internal financing available and avoid new equity

financing while they can engage in new debt financing at reasonably low

interest rates. Another major theory is the Trade-Off Theory in which firms

are assumed to trade-off the tax benefits of debt with the bankruptcy costs of

debt when making their decisions. An emerging area in finance theory is

right-financing whereby investment banks and corporations can enhance

investment return and company value over time by determining the right

investment objectives, policy framework, institutional structure, source of

financing (debt or equity) and expenditure framework within a given

economy and under given market conditions. One last theory about this

decision is the Market timing hypothesis which states that firms look for the

cheaper type of financing regardless of their current levels of internal

resources, debt and equity.

The Dividend Decision

Whether to issue dividends, and what amount, is calculated mainly on

the basis of the company's inappropriate profit and its earnings prospects for

the coming year. If there are no NPV positive opportunities, i.e. projects where

returns exceed the hurdle rate, then management must return excess cash to

investors. These free cash flows comprise cash remaining after all business

expenses have been met.

Page | 8

This is the general case, however there are exceptions. For example,

investors in a "Growth stock", expect that the company will, almost by

definition, retain earnings so as to fund growth internally. In other cases, even

though an opportunity is currently NPV negative, management may consider

investment flexibility / potential payoffs and decide to retain cash flows; see

above and Real options.

Management must also decide on the form of the dividend distribution,

generally as cash dividends or via a share buyback. Various factors may be

taken into consideration: where shareholders must pay tax on dividends, firms

may elect to retain earnings or to perform a stock buyback, in both cases

increasing the value of shares outstanding. Alternatively, some companies will

pay "dividends" from stock rather than in cash; see corporate action. Today, it

is generally accepted that dividend policy is value neutral (see Modigliani-

Miller theorem).

Working capital management

Decisions relating to working capital and short term financing are

referred to as working capital management. These involve managing the

relationship between a firm's short-term assets and its short-term liabilities.

As above, the goal of Corporate Finance is the maximization of firm

value. In the context of long term, capital investment decisions, firm value is

enhanced through appropriately selecting and funding NPV positive

investments. These investments, in turn, have implications in terms of cash

flow and cost of capital.

The goal of Working capital management is therefore to ensure that the

firm is able to operate, and that it has sufficient cash flow to service long term

debt, and to satisfy both maturing short-term debt and upcoming operational

expenses. In so doing, firm value is enhanced when, and if, the return on

capital exceeds the cost of capital.

Financial Risk Management

Risk management is the process of measuring risk and then developing

and implementing strategies to manage that risk. Financial risk management

focuses on risks that can be managed ("hedged") using traded financial

instruments (typically changes in commodity prices, interest rates, foreign

Page | 9

exchange rates and stock prices). Financial risk management will also play an

important role in cash management.

This area is related to corporate finance in two ways. Firstly, firm

exposure to business risk is a direct result of previous Investment and

Financing decisions. Secondly, both disciplines share the goal of enhancing, or

preserving, firm value. All

large corporations have risk management teams, and

small firms practice informal, if not formal, risk management. There is a

fundamental debate on the value of "Risk Management" and shareholder value

that questions a shareholder's desire to optimize risk versus taking exposure to

pure risk. The debate links value of risk management in a market to the cost of

bankruptcy in that market.

Derivatives are the instruments most

commonly used in financial risk

management. Because unique derivative contracts tend to be costly to create

and monitor, the most cost-effective financial risk management methods

usually involve derivatives that trade on well-established financial markets or

exchanges. These standard derivative instruments include options, futures

contracts, forward contracts, and swaps. More customized and second

generation derivatives known as exotics trade over the counter (OTC).

Financial risk; Default (finance); Credit risk; Interest rate risk; Liquidity

risk; Market risk; Operational risk; Volatility risk; Settlement risk; Value at

Risk;.

Page | 10

2.1 Relationship with Other Areas in Finance

Investment Banking

Use of the term corporate finance varies considerably across the

world. In the United States it is used, as above, to describe activities, decisions

and techniques that deal with many aspects of a companys finances and

capital. In the United Kingdom and Commonwealth countries, the terms

corporate finance and corporate financier tend to be associated with

investment banking - i.e. with transactions in which capital is raised for the

corporation. These may include

Raising seed, start-up, development or expansion capital

Mergers, demergers, acquisitions or the sale of private companies

Mergers, demergers and takeovers of public companies, including public-to-

private deals.

Management buy-out, buy-in or similar of companies, divisions or

subsidiaries - typically backed by private equity.

Equity issues by companies, including the flotation of companies on a

recognised stock exchange in order to raise capital for development and/or to

restructure ownership.

Raising capital via the issue of other forms of equity, debt and related

securities for the refinancing and restructuring of businesses.

Financing joint ventures, project finance, infrastructure finance, public-

private partnerships and privatisations.

Secondary equity issues, whether by means of private placing or further

issues on a stock market, especially where linked to one of the transactions

listed above.

Raising debt and restructuring debt, especially when linked to the types of

transactions listed above.

Page | 11

2.2 CORPORATE FINANCE IN INDIA

This site provides comprehensive information on Corporate Finance

India. It also focuses on types of services offered by Corporate Financing

Community in India. The economic renaissance in the 1990s brought by

liberation of Indian economy had a stupendous effect on the financial health of

India. The Indian financial market which was previously insulated from

foreign investors were thrown open for foreign investments. And with modern

economic policies (at par with western countries) in operation large quantum

of foreign direct investments FDI started to flow into the Indian market. The

rise in business activities and its subsequent rise in financial activities led to

the need of proper and accurate financing for corporate in India. Corporate

Finance India provides businessman, investors and entrepreneurs with finance

and advice for proper and risk free investments with an eye for maximum

returns. Corporate Finance India community relies on ready-to-use data,

projections and in formations on India's economy. The projections future

movements of the financial market are based on information and data collected

from daily activities of the finance market. Corporate Financiers in India

advices their clients after taking into consideration financial environment of

the market along with important decisions taken by the Government which,

compliments the financial health of the country. Corporate Finance India

focuses on the provision of corporate advice and funding for Indian companies

who wish to take advantage of the liquidity of the Indian financial markets.

Corporate Finance India provides the following services to the Indian

Corporate Markets.

Corporate Finance.

"Debt and equity funding.

Start up and Growth capital.

Pre-IPO finance.

Real Estate Sales and Acquisition.

Company Sales and Acquisitions.

Corporate Finance India focus has been on entrepreneurial clients,

whether individuals or businesses, and on providing funding and investment in

entrepreneurial businesses. Corporate Finance India offers a complete solution

to its clients objectives through market research. Corporate Finance India

companies have an extensive network of investors and funding institutions and

group of corporate associates.

Page | 12

2.3 INTERNATIONAL BUSINESS IN INDIA

The current scenario for 'International Business in India' is more than

heartening. With stupendous growth of more than 7% annually, improvement

and stabilization of relations with neighboring countries and record setting rise

of its stock indexes, India continues to grab international attention. It is

destination of opportunity with its high-potential workforce and burgeoning

middle class and as an increasingly dynamic competitor.

India being a multi-cultural, multi-lingual and multi-religion state, it is

not advisable to formulate a uniform business strategy. The eastern part of the

country is known as the 'land of the intellectuals' and is regarded as the cultural

hub of the country. The southern part is known for its technology acumen and

western part is the commercial-capital of the country. The north is where the

political power sits and operates the country. International Business

Opportunity in India ' exists in areas like-

Information Technology and Electronics Hardware.

Telecommunication.

Pharmaceuticals and Biotechnology.

R&D.

Banking, Financial Institutions and Insurance & Pensions.

Capital Market.

Chemicals and Hydrocarbons.

Infrastructure.

Agriculture and Food Processing.

Retailing.

Logistics.

Manufacturing.

Power and Non-conventional Energy.

Sectors like Health, Education, Housing, Resource Conservation &

Management Group, Water Resources, Environment, Rural Development,

Small and Medium Enterprises (SME) and Urban Development are untapped

and offer huge scope. With highest numbers of technical, medical, business

management graduates and highest numbers of PhDs coupled with an

energetic English speaking mass India offers 'services' with 50-70% less cost

from their western counterparts. For 'International Business in India' bodies

like CII, FICCI and different Chambers of Commerce provides a variety of

business facilitation services by-

Page | 13

Closely working with Government and business promotion organizations in

India and the respective partner countries.

Also hosts high-level Government dignitaries and help build close working

relationships between Governments and business organizations.

It also exchanges business delegations, joint task forces and identifies

bilateral business co-operation potential and makes suitable policy

recommendations to Governments.

With opportunities galore for' International Business in India' the trend is

mind boggling. India International Business' community along with Indian

Domestic Business community is steadily emerging as the Knowledge Capital

of the world. The World Bank and different rating organizations have forecast

that at 7-8% of Economic growth, she will be worlds second largest economy

by 2050.

2.4 Indian Businesses

Page | 14

Indian Businesses are slowly shifting their base from agriculture major

industrialization. Numerous types of Businesses in India coming up. As India

is developing the Iron & Steel Businesses in India, IT Businesses in India,

Indian Businesses in Travel &I "tourism, Indian Businesses in Business

Process Outsourcing, Food Business market in India, Soft Drinks Businesses in

India and various other types of businesses are coming to the forefront and

taking the center stage.

The marketplace for Indian Businesses is quite varied including

industries in the field of Agriculture & Forestry, Automobiles, Business

Services, Chemicals, Computers, Construction, Education, Electrical,

Electronics, Engineering/ Machinery, Entertainment, Import & Export, Fashion

& Advertising, Food Processing, Government of India Websites, Immigration,

India Neighborhood, Intelligence, International, IT/ITes, Minerals & Metals,

Packaging & Paper, Real Estate in India, Regional Portals, Travel & Tourism

and many others. The scope of doing business in India has grown in its

magnitude.

Some of the major companies in the IT sector are Wipro, Tata

Consultancy Services, Infosys Technologies, HCL ltd, Satyam Computer

Services, Cognizant Technology Solutions, Patni Computers, BFL MphasiS,

Polaris, i-flex, IBM, Hewlett-Packard and Accenture. In general the major

Indian Businesses are the Tatas, Birlas, Ambanis and many more.

The Government has played a major role in the transformation of the

Indian Business scenario in India. The major changes initiated by the

Government for the betterment of the Indian Businesses are in the form of

macroeconomic reforms, tax reforms, finance reforms and freeing of capital

markets, reforms in the regulation of business firms, revitalization of the Indian

private sector, removal of exchange controls and convertibility, trade reforms,

and foreign direct investment. The Foreign companies are showing massive

interest in the Indian Businesses. The number of Businesses in India has

increased at an impressive rate. More and more foreign companies are having

their branches in India. They are either holding hands with the Indian

Businesses by entering into a partnership with them or they are building up

their own offices in India. The 'future of Indian Businesses looks bright and

assuring.

Page | 15

3.1 Sources of Raising Finance

When a company is growing rapidly, for example when contemplating

investment in capital equipment or an acquisition, its current financial

resources may be inadequate. Few growing companies are able to finance their

expansion plans from cash flow alone. They will therefore need to consider

raising finance from other external sources. In addition, managers who are

looking to buy-in to a business ("management buy-in" or "MBI") or buyout

(management buy-out" or "MBO")a business from its owners, may not have

the resources to acquire the company. They will need to raise finance to

achieve their objectives.

There are a number of potential sources of finance to meet the needs of a

growing business or to finance an MBI or MBO:

Family and friends

Business angels

Clearing banks (overdrafts, short or medium term loans)

Factoring and invoice discounting

Hire purchase and leasing

Merchant banks (medium to longer term loans)

Venture capital

Existing shareholders and directors funds

A key consideration in choosing the source of new business finance is to

strike a balance between equity and debt to ensure the funding structure suits

the business. The main differences between borrowed money (debt) and equity

are that bankers request interest payments and capital repayments, and the

borrowed money is usually secured on business assets or the personal assets of

shareholders and/or directors. A bank also has the power to place a business

into administration or bankruptcy if it defaults on debt interest or repayments

or its prospects decline.

In contrast, equity investors take the risk of failure like other

shareholders, whilst they will benefit through participation in increasing levels

of profits and on the eventual sale of their stake. However in most

circumstances venture capitalists will also require more complex investments

(such as preference shares or loan stock) in additional to their equity stake. The

overall objective in raising finance for a company is to avoid exposing the

Page | 16

business to excessive high borrowings, but without unnecessarily diluting the

share capital. This will ensure that the financial risk of the company is kept at

an optimal level.

Business Plan

Once a need to raise finance has been identified it is then necessary to

prepare a business plan. If management intends to turn around a business or

start a new phase of growth, a business plan is an important tool to articulate

their ideas while convincing investors and other people to support it. The

business plan should be updated regularly to assist in forward planning. There

are many potential contents of a business plan. The European Venture

Capital Association suggests the following:

y Profiles of company founders directors and other key managers;

y Statistics relating to sales and markets;

y Names of potential customers and anticipated demand;

y Names of, information about and -assessment of competitors;

y Financial information required to support specific projects (for example,

major capital investment or new product development);

y Research and development information;

y Production process and sources of supply;

y Information on requirements for factory and plant;

y Regulations and laws that could affect the business product and process

protection (patents, copyrights, trademarks).

The challenge for management in preparing a business plan is to

communicate their ideas clearly and succinctly. The very process of researching

and writing the business plan should help clarify ideas and identify gaps in

management information about their business, competitors and the market.

3.2 TYPES OF FINANCE

A brief description of the key features of the main sources of business

finance is provided below.

Page | 17

Venture Capital

Venture capital is a general term to describe a range of ordinary and

preference shares where the investing institution acquires a share in the

business. Venture capital is intended for higher risks such as start up situations

and development capital for more mature investments. Replacement capital

brings in an institution in place of one of the original shareholders of a

business who wishes to realise their personal equity before the other

shareholders.

There are over 100 different venture capital funds in the UK and some

have geographical or industry preferences. There are also certain large

industrial companies which have funds available to invest in growing

businesses and this 'corporate venturing' is an additional source of equity

finance.

Grants and Soft Loans

Government, local authorities, local development agencies and the

European Union are the major sources of grants and soft loans. Grants are

normally made to facilitate the purchase of assets and either the generation of

jobs or the training of employees. Soft loans are normally subsidised by a third

party so that the terms of interest and security levels are less than the market

rate. There are over 350 initiatives from the Department of Trade and Industry

alone so it is a matter of identifying. Which sources will be Appropriate in

each case.

Invoice Discounting and Invoice Factoring

Finance can be raised against debts due from customers via invoice

discounting or invoice factoring, thus improving cash flow. Debtors are used as

the prime security for the lender and the borrower may obtain up to about 80

per cent of approved debts. In addition, a number of these sources of finance

will now lend against stock and other assets and may be more suitable then

bank lending. Invoice discounting is normally confidential (the customer is not

aware that their payments are essentially insured) whereas factoring extends

the simple discounting principle by also dealing with the administration of the

sales ledger and debtor collection.

Page | 18

Hire Purchase and Leasing

Hire purchase agreements and leasing provide finance for the acquisition

of specific assets such as cars, equipment and machinery involving a deposit

and repayments over, typically, three to ten years. Technically, ownership of

the asset remains with the lessor whereas title to the goods is eventually

transferred to the hirer in a hire purchase agreement.

Loans

Medium term loans (up to seven years) and long term loans (including

commercial mortgages) are provided for specific purposes such as acquiring an

asset, business or shares. The loan is normally secured on the asset or assets

and the interest rate may be variable or fixed. The Small Firms Loan Guarantee

Scheme can provide up to 250,000 of borrowing supported by a government

guarantee where all other sources of finance have been exhausted.

Bank Overdraft

An overdraft is an agreed sum by which a customer can overdraw their

current account. It is normally secured on current assets, repayable on demand

and used for short term working capital fluctuations. The interest cost is

normally variable and linked to bank base rate. Completing the Finance-raising

Raising finance is often a complex process. Business management need to

assess several alternatives and then negotiate terms which are acceptable to the

finance provider. The main negotiating points are often as follows:

y Whether equity investors take a seat on the board.

y Votes ascribed to equity investors.

y Level of warranties and indemnities provided by the directors.

y Financier's fees and costs.

During the finance-raising process, accountants are often called to

review the financial aspects of the plan. Their report may be formal or

informal, an overview or an extensive review of the company's management

information system, forecasting methods and their accuracy, review of latest

management accounts including working capital, pension funding and

employee contracts etc. This due diligence process is used to highlight any

fundamental problems that may exist

Page | 19

3.3 Game Theory Application for Corporate Finance

Finance in general is concerned with how the savings of investors are

allocated through financial markets and intermediaries to firms, who use them

Page | 20

to fund their activities. Finance can broadly be broken down into two fields.

The first is asset pricing, which is concerned with the decisions of investors.

The second is corporate finance, which is concerned with the decisions of

firms. This paper will focus on the latter field and how game theory can be

used to explain certain behaviors that are regularly witnessed. Traditional

financial thinking relies on assumptions of certainty, complete knowledge and

market efficiency and in this context, financial decisions should be relatively

straightforward. In the real world though, many times what is observed

deviates greatly from what would be expected using traditional financial

thinking. This paper will show how different game theory models can be used

to more accurately explain observed financial decisions dealing with capital

structure, corporate acquisitions and initial public offerings (IPOs).

Game theory has made great strides in explaining many of the observed

phenomena falling under corporate finance. One example is the capital

structure decided upon by a firms management. Capital structure deals with

the firms decision to raise funds through debt versus equity and what ratio of

debt to equity should the firm maintain. Modigliani and Miller in 1958 showed

that in perfect capital markets (i.e. no frictions and symmetric information) and

no taxes a firm could not change its total value by altering its debt/equity ratio;

thus capital structure is irrelevant. However in the real world, capital structure

is carefully thought about by every company, and it is in fact not irrelevant

because taxes do exist and capital markets are not perfect. In the United States,

interest paid by a company is a tax-deductible expense. This tax shield creates

an incentive to take on debt. Modigliani and Miller corrected their original

model to include corporate income taxes showing that a firm could increase its

equity, or shareholder value, by taking on debt and taking advantage of tax

shields. Their model then showed all firms stood to gain the most if they were

100% debt financed; however this is not observed in reality. In fact, some

companies and industries thrive with no debt at all. Different game theory

models have been used to explain the actions of managers in determining their

companys capital structure, the most influential deals with the signaling

effects attributed to debt vs. equity financing. In 1984 Myers and Majluf

developed a model based on asymmetric information that insists managers are

better informed of the prospects of the firm than the capital markets.

If management feels that the market is currently undervaluing its firms

equity then it will be unwilling to raise money through an equity issue because

it will be selling the stock at a discount. On the other hand, management might

be eager to issue equity if it feels its stock is overvalued, because it will be

Page | 21

selling its stock at a premium. Investors are not dull and will predict that

managers are more likely to issue stock when they think it is overvalued while

optimistic managers may cancel or defer issues. Therefore, when an equity

issue is announced, investors will mark down the price of the stock

accordingly. Thus equity issues are considered a bad signal; even companies

with overvalued stock would prefer another option to raise money to avoid the

mark down in stock price. Firms prefer to use less information sensitive

sources of funds.

This leads to the pecking order of corporate financing: Retained earnings

are the most preferred, followed by debt, then hybrid securities such as

convertible bond and lastly equity. Some industries by their nature support

companies that finance most of their growth through retained earnings.

Airlines however are an example of an industry that is characterized by its high

debt level. In general, capital structure is similar within industries with

differences resulting from weighing the benefits of a higher tax shield versus

the benefits of the less information sensitive financial of retained earnings.

A second application of game theory to capital structure is concerned

with agency costs. In 1976 Jensen and Meckling described two kinds of agency

problems in corporations: One between equity holders and bondholders and the

other between managers and equity holders. The first arises because the

owners of a levered firm have an incentive to take risks at the expense of debt

holders. Stockholders of levered firms gain when business risk increases

because they receive the surplus when returns are high but the bondholders

bear the cost when default occurs. Bondholders value does not increase with

the value of the firm, thus they would like the firm to take safe bets to

minimize the risk of default. Equity holders on the other hand, receive

whatever is leftover after paying back debt holders. They would like to see the

upside potential of the company maximized and this occurs through taking on

risky projects (higher returns are generated though greater risk taking.) It is

obvious that there is a conflict of interest between equity holders desire for

business risk and bondholders aversion to business risk. Financial managers

who act strictly in the interests of shareholders will favor risky projects over

safe ones. It is important to note that this agency cost does not occur in

financially sound companies. It mainly occurs when the odds of default or high

and equity holders feel they can make one last gamble to avoid bankruptcy and

get a big payoff at the same time.

Page | 22

An average payoff would not benefit the stockholders much when the

company is near default because most of the payoff will be paid out to the debt

holders. A financially sound company would not have this agency problem

because equity holders stand to lose more from risky projects when the

company is not in risk of going bankrupt, and thus want to avoid them along

with bondholders. The second conflict arises when equity holders cannot fully

control the actions of managers. This occurs when managers have an incentive

to pursue their own interests rather than those of the equity holders. Executive

compensation in the form of option contracts can create incentives for

managers to make risky decisions in an attempt to gain the highest payoff from

the call options. Higher risk increases the value of an option, but risk can also

cause a stock price to take a nosedive. A manager with options is not hurt

nearly as much as a worker with his/her retirement savings in a company

whose stock plummets because of risky bets. Option contracts were meant to

better align the interests of managers with stockholders, but it is obvious that

this is not so easily achieved. Game theory can also be used to explain what is

observed in the course of many corporate acquisitions. If markets are efficient

then one would expect a company to pay fair value when acquiring another

company; however in many instances the acquirer pays a large premium to buy

the other company. In 1986 Shleifer and Vishny provide one explanation of

this phenomenon, the free rider problem. One of the concepts behind efficient

markets is the market for corporate control. The market for corporate control

says that in order for resources to be used efficiently, companies need to be run

by the most able and competent managers. One way to achieve this is through

corporate acquisitions.

Initial Public Offerings (IPOs) have long been known to provide a

significant positive return in the initial days of trading. This occurrence

directly conflicts with the theory of market efficiency because the companies

should be fairly valued at their IPO and any return in the initial days should be

minimal. In 1986 Rock explained that this phenomenon was due to adverse

selection between informed buyers and uninformed buyers. The informed

buyers know the true value of the stock and will only purchase shares at or

below its true value. The implication of this is that the uninformed buyers will

receive a high allocation of overpriced shares since they will be the only

people in the market when the offering price is above the true value. Knowing

this, uninformed buyers would be unwilling to purchase the stock; forcing the

informed buyers to hold onto the stock because there is no one they can sell it

to. Therefore, to induce the uninformed to participate they must be

compensated for the overpriced stock they end up buying. One way to do this

Page | 23

is to under-price the stock on average. This means that on average the

uniformed will buy a stock that started out undervalued and thus they are still

able to buy the stock at or below its true value. Since all investors know that an

IPO will likely be under priced they all try to buy the stock as quick as possible

creating a demand for the stock that results in substantial price gain in the

initial days of trading.

Another interesting implication of IPOs pointed out by Ritter in 1991 is

the fact that while they experience high returns in the short run they typically

under-perform the market in the long run. One argument for this behavior is

that the market for IPOs is subject to fads and that investment banks under-

price IPOs to create the appearance of excess demand. This leads to a high

price initially but subsequently underperformance; therefore companies with

the highest initial returns should have the lowest subsequent returns. There

exists evidence of this in the long run.

Game theory has been extremely useful in explaining certain financial

decisions. This paper has only highlighted a few of the aspects where

behavioral analysis has helped explained observed behavior. Specifically,

game theory has helped explain the reasons companies might choose various

capital structures and the agency costs between managers, equity holders, and

debt holders. In addition, the existence of free rider problems and bidding wars

in corporate acquisitions has been made clear through game theory

applications. Lastly, IPOs exhibit behavior contrary to the efficient market

theory, and game theory can be utilized to help show why this behavior occurs.

3.4 Agency Costs of Free Cash Flow and Corporate Finance

Page | 24

Corporate managers are the agents of shareholders, a relationship

fraught with conflicting interests. Agency theory, the analysis of such conflicts,

is now a major part of the economics literature. The payout of cash to

shareholders creates major conflicts that have received little attention. Payouts

to shareholders reduce the resources under managers control, thereby reducing

managers power, and making it more likely they will incur the monitoring of

the capital markets which occurs when the firm must obtain new capital.

Financing projects internally avoids this monitoring and the possibility the

funds will be unavailable or available only at high explicit prices.

Managers have incentives to cause their firms to grow beyond the

optimal size. Growth increases managers power by increasing the resources

under their control. It is also associated with increases in managers

compensation; because changes in compensation are positively related to the

growth in sales.

Competition in the product and factor markets tends to drive prices

towards minimum average cost in an activity. Managers must therefore

motivate their organizations to increase efficiency to enhance the problem of

survival. However, product and factor market disciplinary forces are often

weaker in new activities and activities that involve substantial economic rents

or quasi rents. In these cases, monitoring by the firms internal control system

and the market for corporate control are more important. Activities generating

substantial economic rents or quasi rents are the types of activities that

generate substantial amounts of free cash flow.

Free cash flow is cash flow in excess of that required to fund all projects

that have positive net present values when discounted at the relevant cost of

capital. Conflicts of interest between shareholders and managers over payout

policies are especially severe when the organization generates substantial free

cash flow. The problem is how to motivate managers to disgorge the cash

rather than investing it at below the cost of capital or wasting it on organization

inefficiencies.

The theory developed here explains 1) the benefits of debt in reducing

agency costs of free cash flows, 2) how debt can substitute for dividends, 3)

why diversification programs are more likely to generate losses than

takeovers or expansion in the same line of business or liquidation-motivated

takeovers, 4) why the factors generating takeover activity in such diverse

Page | 25

activities as broadcasting and tobacco are similar to those in oil, and 5) why

bidders and some targets tend to perform abnormally well prior to takeover.

3.5 The Role of Debt in Motivating Organisational Efficiency

Page | 26

The agency costs of debt have been widely discussed, but the benefits of

debt in motivating managers and their organizations to be efficient have been

ignored. I call these effects the control hypothesis for debt creation.

Managers with substantial free cash flow can increase dividends or repurchase

stock and thereby pay out current cash that would otherwise be invested in

low-return projects or wasted. This leaves managers with control over the use

of future free cash flows, but they can promise to pay out future cash flows by

announcing a permanent increase in the dividend. Such promises are weak

because dividends can be reduced in the future. The fact that capital markets

punish dividend cuts with large stock price reductions is consistent with the

agency costs of free cash flow.

Debt creation, without retention of the proceeds of the issue, enables

managers to effectively bond their promise to pay out future cash flows. Thus,

debt can be an effective substitute for dividends, something not generally

recognized in the corporate finance literature. By issuing debt in exchange for

stock, managers are bonding their promise to pay out future cash flows in a

way that cannot be accomplished by simple dividend increases. In doing so,

they give shareholder recipients of the debt the right to take the firm into

bankruptcy court if they do not maintain their promise to make the interest and

principal payments.

Thus debt reduces the agency costs of free cash flow by reducing the

cash flow available for spending at the discretion of managers. These control

effects of debt are a potential determinant of capital structure. Issuing large

amounts of debt to buy back stock also sets up the required organizational

incentives to motivate managers and to help them overcome normal

organizational resistance to retrenchment which the payout of free cash flow

often requires. The threat caused by failure to make debt service payments

serves as an effective motivating force to make such organizations more

efficient.

Stock repurchases for debt or cash also has tax advantages. (Interest

payments are tax deductible to the corporation, and that part of the repurchase

proceeds equal to the sellers tax basis in the stock is not taxed at all.)

Increased leverage also has costs. As leverage increases, the usual agency costs

of debt rise, including bankruptcy costs. The optimal debt-equity ratio is the

point at which firm value is maximized, the point where the marginal costs of

debt just offset the marginal benefits.

Page | 27

The control hypothesis does not imply that debt issues will always have

positive control effects. For example, these effects will not be as important for

rapidly growing organizations with large and highly profitable investment

projects but no free cash flow. Such organizations will have to go regularly to

the financial markets to obtain capital.

At these times the markets have an opportunity to evaluate the company,

its management, and its proposed projects. Investment bankers and analysts

play an important role in this monitoring, and the markets assessment is made

evident by the price investors pay for the financial claims. The control function

of debt is more important in organizations that generate large cash flows but

have low growth prospects, and even more important in organizations that

must shrink. In these organizations the pressures to waste cash flows by

investing them in uneconomic projects is most serious.

Financial Statement of Cairns Ltd

4.1 In the Books of Cairns Ltd

Page | 28

Income Statement for year ended 31

st

march 2009

PARTICULARS AMOUNT AMOUNT

Net Sales 37,331

OPERATING EXPENSES

Administrative Expenses

Staff Cost 2,12,519

Data Acquisition 36,235

Other Administrative 7,20,544

Amortisation 365

Unsuccessful Exploration cost 8,13,568

Selling & Distribution

Advertisement 14,385

Publicity 42,959

Sponsorship 15,666

Financial Expenses

Bank Charges 3,058

Other Interest 388

18,59,687

PORFIT BEFORE INTEREST (18,22,356)

Less :- 0

PROFIT AFTER INTEREST (18,22,356)

Add :- Non Operating Income

Interest on Deposit 1,31,377

Dividend 2,00,225

Profit on Sale Of Investment 12,45,686

Special Gains 1,55,723

Other Income 61

29,43,072

PROFIT BEFORE TAX 11,20,716

Less : -

Current Tax 5,43,800

other tax 34,509

5,78,309

Profit After Tax 5,42,407

In the books of Cairns Ltd

Balance sheet as at 31

st

march 2009

Page | 29

PARTICULARS Amount Amount Amount

I) SORCES OF FUNDS

1) SHAREHOLDERS FUNDS

a) Share Capital

Equity Share Capital 1,89,66,678

Preference Share Capital 0

Stock Options Outstanding 3,88,978

19355656

b) Reserve & Surplus

Securities Premium A/C 30,10,90,274

(-) c) Miscellaneous Expenses

P/L Debit Expenses 5,38,000

300552274

2) Borrowed Funds

Capital Employed 31,99,07,930

II) APPLICATION OF FUNDS

1) FIXED ASSETS

Computers 609

Work in Progress 5,40,299

540908

2) INVESTMENT

Investment in Companies 29,22,53,966

29,27,94,478

3) Working Capital

Current Assets

Debtors 17 942

Cash & bank Balance 2,76,32,762

Other Current Assets 6,33,645

Loans & Advances 2,20,814

28505163

Less :- Current Liabilities

Creditors 8,75,666

Other Liabilities 2,01,068

Provisions 3,15,373

1392107

Sub-total (d) 2,71,13,056

Funds Used ( c+d) 31,99,07,930

In the Books of Cairns Ltd

Comparative Balance sheet as at 31

st

Dec 2007 &31

st

march 2009

Page | 30

PARTICULARS 31-12-2007 31-03-2009 INCREASE /

DECREASE

% CHANGE

I) SORCES OF FUNDS

1) SHAREHOLDERS FUNDS

a) Share Capital

Equity Share Capital 1,77,83,994 1,89,66,678 11,82,684 6.65%

Preference Share Capital 0 0 0 0

Stock Options Outstanding 9,47,084 3,88,978 (5,58,106) -58.92%

b) Reserve & Surplus

Securities Premium A/C 27,60,84,115 30,10,90,274 2,50,06,159 9.05%

Sub Total (a) 29,48,15,193 32,04,45,930 2,56,30,737 8.69%

c) Miscellaneous Expenses

P/L Debit Expenses 10,80,407 5,38,000 (5,42,407) -50.20%

Sub Total (b) 29,37,34,786 31,99,07,930 2,61,73,144 8.91%

2) Borrowed Funds

Capital Employed 29,97,34,786 31,99,07,930 2,01,73,144 6.73%

II) APPLICATION OF FUNDS

1) FIXED ASSETS

Computers 0 609 609 100%

Work in Progress 0 5,40,299 5,40,299 100%

2) INVESTMENT

Investment in Companies 29,41,37,285 29,22,53,966 (18,83,319) -0.64%

Page | 31

Sub-Total 29,41,37,285 29,27,94,478 (13,42,807) -0.45%

3) Working Capital

Current Assets

Debtors 12,708 17,942 5,234 41.18%

Cash & bank Balance 7,757 2,76,32,762 2,76,25,005 3,56,130 %

Closing Stock 0 6,33,645 6,33,645 100%

Bills Receivable 35,950 2,20,814 1,84,846 514.17%

Less :- Current Liabilities

Creditors 1,36,964 8,75,666 7,38,702 539.34%

Other Liabilities 1,446 2,01,068 1,99,622 13805%

Provisions 3,20,504 3,15,373 -5,131 -1.60%

Sub-total (d) (4,02,499) 2,71,13,056 2,67,10,557 66.36%

Funds Used ( c+d) 29,97,34,786 31,99,07,930 2,01,73,144 6.73%

4.2 Accounting Ratios

Balance Sheet Ratios

Page | 32

1. Current ratio =

(Current Asset) / (Current Liability)

28505163 / 1392107

= 20.47

The standard ratio is 2:1. It indicates the short term solvency of

the company here the companys current ratio is very excellent as to

every 1 liability they have 20.47 assets.

2. Quick ratio

(Current Asset Stock Prepaid Exp) / (Current liability

Bank Overdraft)

27237873 / 1392107

= 19.56

The standard ratio is 1:1. It indicates immediate solvency of the

company here the company has 19.56 assets as compare to 1 liability

each.

3. Proprietary ratio =

[(Proprietors fund) / (Total Assets) ] *100

[3199079 30/ 321300037] *100

= 99.56 %

The Share of proprietor in companys fund is 99.56 % which is

very good so this shows a strong backup for the company.

4. Stock turnover ratio =

Page | 33

[(Closing Stock) / (Working Capital)] *100

[633645 / 27113056] *100

= 2.33%

The standard ratio is 200 % here the ratio is only 2.33%. this

shows that the company will face certain problems in near future.

Income Statement Ratio

Page | 34

1. Gross profit ratio =

[ (Gross profit) / (Net Sales) ] *100

[-1043076 / 37331] * 100

= -2794 %

Here the company is earning losses so thats why the gross profit

ratio is in minus.

2. Net Profit Ratio=

Net profit before tax / Net Sales *100

[40399 / 37331] *100

=108.21 %

It is very good but the business surviving only through non

operating income

3. Net Profit After tax ratio=

Net Profit After tax / Net Sales *100

[542407 / 37331] *100

=1452 %

This ratio is also good as it shows 1452 % ratio.

4. Operating Ratio =

Page | 35

(Cost of Goods sold + Operating Exp) / Net Sales *100

[1859687 / 37331] * 100

=4981 %

It is bad because the expenses are more than the sales.

Mixed Ratios

Page | 36

1. Debtors Turnover Ratio=

Credit sales / Average ( Debtors +Bills Receivable)

[37331 / 238756 ]

= 0.15 times

It is not good because the sales is very less

2. Average Collection Period =

12 months / Debtors turnover ratio

[12 / 0.15]

= 80 months

It shows that the company will face shortage of funds in the

future because they will not be able to recover their money quickly as

they will recover only after 80 months.

3. Earnings Per Share=

(Net Profit after tax- Preference Dividend) / No. of Equity shares

[5,42,407 / 1876199069]

= 0.29

The earning per share ratio some what ok as it shows 0.29

return.

4. Price Earning Ratio =

Page | 37

Market Price per share / Earning per share

[10 / 0.29]

= 34.48

Assuming that the market price is 10. The price earning is

also good.

5. Return On Capital Employed =

(Profit Before Interest) / Capital Employed *100

[1822356) / 319907930] * 100

= -0.56 %

It is very bad as it shows negative balance of 0.56 %.

Page | 38

4.3 Case Study on General Mills

A. General Mills Consolidated Statements of Earnings:

1. The recorded sale amount of almost $8 billion is not the actual amount of

cash collected. The amount of $8 billion includes cash and credit sales.

2. Sales increased each year from 2000 to 2002. The difference between the

year 2000 and 2001 was a 5.35% increase (5,450-5,173/5,173 = .0535).

The difference between the year 2001 and 2002 was a 45.85% increase

(7,949-5,450/5,450 = .4585).

3. The largest expense for General Mills for the years 2000, 2001, and 2002

was the same; over 50% of the revenue each year went towards the cost

of sales. Sales in 2002 were the largest, about 7% more than the two

previous years. 2000: (2,698/5,173) = .522 = 52.2% 2001: (2,841/5,450

= .521 = 52.1% 2002: (4,767/7,949) = .599 = 59.9%

4. Net Income: 2000: $614 million 2001: $665 million 2002: $458 million

When comparing the net income figures for the past three years, it is seen

that between 2000 and 2001, the net income increased by $51 million,

but between 2001 and 2002, the net income decreased by $207 million.

5. A company's stock price is usually influenced by the amount of net

income because when finding the price of the stock, you must divide the

number of stocks by the net income. So, the higher the net income, the

lower the price of stocks, which is what buyers look for (means better

profit).

6. Even though General Mills paid dividends in 2000, 2001 and 2002, the

corresponding total dividend payments did not appear as an expense on

the income statement because dividends are not an expense; they are a

financing activity that is reported on the statement of stockholder's

equity. They are payments that are made to only the owners of the

company.

B. General Mills Consolidated Balance Sheets:

Page | 39

7. A company has assets so that they have a location and equipment to

operate/create a business. Assets are resources that are controlled by a

business. Without assets, one cannot produce and/or run a company. The

purpose of assets are to keep track of expenses, what a company owns,

like equipment, inventory, cash etc., and creates value for the company.

8. The total amount of assets at the end of 2002 was $16,540 million.

9. When comparing the assets from the beginning of 2002 to the end, we

found that the percentage increase in assets was 224.89% (16,540-

5,091/5,091 = 2.2489 = 224.89%). Goodwill is the type of asset that is

responsible for the increase.

10. The two groups that have contributed assets to General Mills and claims

on the assets are shareholders and lenders. Shareholders have about

$5,733 million in claims and the lenders have a claim of $5,591 million.

C. General Mills Consolidated Statement of Stockholder's Equity:

11. The General Mill's total stockholders increased significantly from May

27, 2001 to May 26, 2002 because they sold more stock.

12. Comprehensive income is the change in a company's owner's equity

during a period that is the result of all transactions and activities that are

not by the owner. These can include profits from operating activities,

foreign currency, and net income, events that change owner's equity

except those from the company's own stockholders and selling stock or

paying dividends.

D. General Mills Consolidated Statement of Cash Flows:

Page | 40

13. There are three categories of cash flows shown on the company's cash

flow statement. They are the following:

1. Operating activities 2. Investing activities 3. Financial

activities.

14. When comparing the net income figure to the amount of net cash

provided by operating activities for each of the three years, one observes

that the net income went up in the first two years and than decreased

between the second and the third year. The net cash from operating

activities increased each year, but its greatest growth was between the

second and the third year. So, when the net income was the lowest, the

net cash from operating activities was the greatest.

15. Net cash provided by Net cash used by operating activities investment

activities 2000: $722 million (564 million) 2001: $737 million (460

million) 2002: $913 million (3,271 million) It is clear to see that in the

year 2000 and 2001, operating activities was large enough to cover the

investing cash outflow, but in 2002, the investing cash outflow exceeded

far past the amount of net cash provided by operating activities. Loans

were used to make up the difference.

16. When comparing the dividend payments to the income amounts for the

current year, we found that the dividend payout ratio for 2002 was 78.2%

(358/458 = .7816 = 78.2) E. General Mills Report of Management

Responsibilities and Reports of Independent Public Accountants:

17. The management of General Mills, Inc. is responsible for the accounting

numbers in the annual report.

18. For safeguards, General Mills used internal controls to ensure the

accuracy of the reported numbers, including: an audit program, a

separation of duties and responsibilities, and instated policies that

demand ethical behavior from employees.

19. The independent accountant does not say that the reported amounts are

correct, but does state that they are reported fairly. "We believe these

consolidated financial statements do not misstate or omit any material

Page | 41

facts... In our opinion, the consolidated financial statements referred to

above present fairly, in all material respects..." The CPA assures that the

statements are in accordance with the GAAP.

20. General Mills hired a CPA (Certified Public Accountant) to audit the

financial statements to ensure accuracy and to verify that the numbers on

the statements (disclosures made by the management in its reports) are

consistent with the company's actual financial position, cash flow, and

results from its operating activities.

21. General Mills hired KPMG LLP as their accountant to audit their

financial statements. The report of the independent accountants that

performed this was signed on June 24, 2002.

F. General Mills Financial Statements:

22. General Mills major operating activities during 2002 were net sales,

selling, general, and administrative, and cost of goods. The major

difference between accrual and the cash flow of these activities is that

accrual includes cash and credit, where these major operating activities

only include cash. Accrual accounts for all, while the cash flow doesn't

account for credit sales until the money is collected.

23. General Mills return on total assets for 2001 was 13.1% (665/5,091=

.1306) and in 2002, the return on total assets was 2.8% (458/16,540 =

.0276). The return on total assets deteriorated from 2001 by 10.3%

(.1306-.0276 = .103)

24. If you owned 10,000 of the company's common stock in 2002, your

claim on the company's earnings would be $13,800 (10,000 x 1.38 (EPS-

basic) = 13,800). If you were to own 10,000 of the company's common

stock in 2001, your claim would be greater than your claim if you would

to purchase them in 2002 by $9,600, making your claim in 2001 $23,400.

(10,000 x 2.34 (EPS-basic) = 23,400).

Page | 42

25. The major source of cash for General Mills in 2002 was the issuance of

long-term debt. With the cash they received, they were able to purchase

Pillsbury (acquired in a stock and cash transaction).

26. Major financing activities performed in 2002 were the change in long-

term debt. They increased their amount of debt while paying off some of

their notes payable. They also purchased some treasury stocks. In the

year 2002, their net cash increased incredibly, by about $3,500 million,

which was one of the biggest increases recorded over the previous years

for net cash.

27. A major investing activity that occurred in 2002 was when General Mills

purchased Pillsbury.

28. At the end of 2002, the company's most important assets were:

inventories, goodwill, receivables, and land, buildings, and equipment.

Other resources that might be important that aren't reported on the

balance sheet are the skills and level of intelligence of the management

and the employees, as well as the value of the brand name 29. If asked to

assess the company's financial performance of General Mills in 2002, I

would have to say that they were very successful. Their financial

activities show that they are a growing and prosperous company; their

operating and financing activities are increasing and the investing cash

flows decreasing, keeping the inflow larger than the outflow. Their

successfulness opens many new opportunities for them in the future.

Page | 43

CONCLUSION

Arguably, the role of a corporation's management is to increase the value

of the firm to its shareholders while observing applicable laws and

responsibilities. Corporate finance deals with the strategic financial issues

associated with achieving this goal, such as how the corporation should raise

and manage its capital, what investments the firm should make, what portion

of profits should be returned to shareholders in the form of dividends, and

whether it makes sense to merge with or acquire another firm.

If the role of management is to increase the shareholder value, then

managers can make better decisions if they can predict the impact of those

decisions on the firm's value. By observing the difference in the firm's equity

value at different points in time, one can better evaluate the effectiveness of

financial decisions. A rudimentary way of valuing the equity of a company is

simply to take its balance sheet and subtract liabilities from assets to arrive at

the equity value. However, this book value has little resemblance to the real

value of the company. First, the assets are recorded at historical costs, which

may be much greater than or much less their present market values. Second,

assets such as patents, trademarks, loyal customers, and talented managers do

not appear on the balance sheet but may have a significant impact on the firm's

ability to generate future profits. So while the balance sheet method is simple,

it is not accurate; there are better ways of accomplishing the task of valuation.

Another way to value the firm is to consider the future flow of cash.

Since cash today is worth more than the same amount of cash tomorrow, a

valuation model based on cash flow can discount the value of cash received in

future years, thus providing a more accurate picture of the true impact of

financial decisions.

The primary goal of corporate finance is to maximize corporate value

while managing the firm's financial risks. Although it is in principle different

from managerial finance which studies the financial decisions of all firms,

rather than corporations alone, the main concepts in the study of corporate

finance are applicable to the financial problems of all kinds of firms.

Page | 44

The distinction between cash and equity shareholders' equity is the sum

of common stock at par value, additional paid-in capital, and retained earnings.

Some people have been known to picture retained earnings as money sitting in

a shoe box or bank account. But shareholders' equity is on the opposite side of

the balance sheet from cash. In fact, retained earnings represent shareholders'

claims on the assets of the firm, and do not represent cash that can be used if

the cash balance gets too low. In this regard, one can say that retained earnings

represent cash that already has been spent.

Shareholder equity changes due to three things:

y net income or losses

y payment of dividends

y share issuance or repurchase.

Changes in cash are reported by the cash flow statement, which

organizes the sources and uses of cash into three categories: operating

activities, investing activities, and financing activities.

The primary goal of corporate finance is to maximize corporate value

while managing the firm's financial risks. Although it is in principle different

from managerial finance which studies the financial decisions of all firms,

rather than corporations alone, the main concepts in the study of corporate

finance are applicable to the financial problems of all kinds of firms.

In the process of Corporate Finance the main factor plays an

important role that is Financial Risk Management. It is the process of

measuring risk and then developing and implementing strategies to manage

that risk. Financial risk management focuses on risks that can be managed

("hedged") using traded financial instruments (typically changes in

commodity prices, interest rates, foreign exchange rates and stock prices).

Financial risk management will also play an important role in cash

management.

Page | 45

Financial decisions, the analysis and tools that are required to reach

these conclusions is what corporation finance is all about. The objective of this

is to improve the value of the company while simultaneously reducing any

financial risks. In addition it oversees that the company gets maximum returns

on whatever ventures they have invested in. Corporate finance can be

categorized into short and long term decisions.

Short term decisions like capital management deal with current liabilities

and asset balance. This is basically management of cash, inventories and

lending on a short term basis. The long term category deals with investments

of capital in relation to projects and the techniques required to fund them.

Corporate finance is also associated with investment banking. The investment

banker is in charge of evaluating the different projects that are brought to the

bank and making appropriate investment decisions.

For the company to be able to achieve their objectives, they need to have

a proper financial structure in place. It has to be able to accommodate the

various financial options that are available. These sources could be a

combination of equity and also debt. When a business or project is funded

through equity, there is a lower risk in terms of the cash flow. The one done

through debt is more of a liability to the company which needs to be assessed.

This automatically affects the cash flow even if the project turns out to be a

success.

The company must try to equate the invest merge with the asset being

financed as much as possible. When a company is adequately financed, it has

enough in its reserves for any contingencies.

Page | 46

Bibliography

www.google.com

www.scribd.com

www.indiatimes.com

www.rediffmail.com

www.wikipedia.org

You might also like

- Business Income and Expense Report InstructionsDocument4 pagesBusiness Income and Expense Report InstructionsMOUHSINE BETONOVNo ratings yet

- Home Office and Branch AccountingDocument12 pagesHome Office and Branch AccountingKrizia Mae FloresNo ratings yet

- Case Study On Lenovo and Ibm Lenovo Mergers and AcquisitionsDocument28 pagesCase Study On Lenovo and Ibm Lenovo Mergers and AcquisitionsLê Trần CảnhNo ratings yet

- Exchange Control RegulationDocument5 pagesExchange Control RegulationArjun lal KumawatNo ratings yet

- Fera and Fema: Foreign Exchange Regulation Act & Foreign Exchange Management ActDocument8 pagesFera and Fema: Foreign Exchange Regulation Act & Foreign Exchange Management ActMayank JainNo ratings yet

- Axis BankDocument14 pagesAxis BankNikhil Kapoor50% (2)

- Bales Et Al (2004)Document6 pagesBales Et Al (2004)eraldoboechatNo ratings yet

- Capital Budgeting TechniquesDocument10 pagesCapital Budgeting TechniqueslehnehNo ratings yet

- SEBI Takeover Code - UpdatedDocument24 pagesSEBI Takeover Code - UpdatedSagarNo ratings yet

- Foreign Exchange Risk Management in IndiaDocument13 pagesForeign Exchange Risk Management in IndiaRaman Sehgal100% (1)

- Security Analysis and Portfolio Management Unit-1 InvestmentDocument27 pagesSecurity Analysis and Portfolio Management Unit-1 InvestmentMadhu dollyNo ratings yet

- Predicting Financial Distress of Pharmaceutical Companies in India Using Altman Z Score ModelDocument4 pagesPredicting Financial Distress of Pharmaceutical Companies in India Using Altman Z Score ModelInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- FDRM AssignmentDocument3 pagesFDRM AssignmentAmit K SharmaNo ratings yet

- Quarterly Report On The Results For The Second Quarter and Half Year Ended September 30, 2012Document54 pagesQuarterly Report On The Results For The Second Quarter and Half Year Ended September 30, 2012mayur860No ratings yet

- Project On Derivative MarketDocument42 pagesProject On Derivative MarketbrijeshkynNo ratings yet

- As 13 Accounting of InvestmentsDocument6 pagesAs 13 Accounting of InvestmentsSamridhi SinghalNo ratings yet

- Importance of Mutual FundsDocument14 pagesImportance of Mutual FundsMukesh Kumar SinghNo ratings yet

- Futures and Options in IndiaDocument13 pagesFutures and Options in IndiaAsmita SodekarNo ratings yet

- Structure of Capital Market: Dr. Deepa Soni Assistant Professor Department of Economics Mlsu (Ucssh) UdaipurDocument5 pagesStructure of Capital Market: Dr. Deepa Soni Assistant Professor Department of Economics Mlsu (Ucssh) UdaipurAnonymous 1ClGHbiT0J0% (1)

- Echange Rate Mechanism: 1. Direct Quote 2. Indirect QuoteDocument4 pagesEchange Rate Mechanism: 1. Direct Quote 2. Indirect QuoteanjankumarNo ratings yet

- Nov 2019Document39 pagesNov 2019amitha g.sNo ratings yet

- Financial Markets and InstrumentsDocument110 pagesFinancial Markets and InstrumentsPUTTU GURU PRASAD SENGUNTHA MUDALIARNo ratings yet