You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- CWC GuidebookDocument32 pagesCWC Guidebookpreetcivil100% (5)

- 19th EPS Mega City Part IIDocument233 pages19th EPS Mega City Part IIPatiala SinghNo ratings yet

- Ecu AudiDocument14 pagesEcu Audieduardorojas007No ratings yet

- Ias 21Document16 pagesIas 21Leonardo BritoNo ratings yet

- Ias 19Document59 pagesIas 19Leonardo BritoNo ratings yet

- IAS18Document12 pagesIAS18Ali AmirAliNo ratings yet

- Ias 17Document18 pagesIas 17Leonardo BritoNo ratings yet

- Ias 16Document21 pagesIas 16Leonardo BritoNo ratings yet

- Ias 12Document40 pagesIas 12Leonardo BritoNo ratings yet

- IAS1 Presentation of Financial StatementsDocument33 pagesIAS1 Presentation of Financial StatementsJohn Rey Batandolo ManatadNo ratings yet

- IAS7Document16 pagesIAS7Fitri Putri AndiniNo ratings yet

- Ifrs - 6: Exploration and Evaluation of Mineral ResourcesDocument8 pagesIfrs - 6: Exploration and Evaluation of Mineral ResourcesFitri Putri AndiniNo ratings yet

- IFRS3Document31 pagesIFRS3Nguyen Anh VuNo ratings yet

- Vol.10 Issue 22 September 30-October 6, 2017Document32 pagesVol.10 Issue 22 September 30-October 6, 2017Thesouthasian TimesNo ratings yet

- Different Form of Public EnterpriseDocument5 pagesDifferent Form of Public EnterpriseManikrant Kumar75% (4)

- Daily Prductivity ReportsDocument158 pagesDaily Prductivity ReportsMadhu shreeNo ratings yet

- Tax 1007-16Document67 pagesTax 1007-16jaseyNo ratings yet

- Aci 212.3R-91Document31 pagesAci 212.3R-91farhadamNo ratings yet

- How Does The Community Exchange System Work?Document6 pagesHow Does The Community Exchange System Work?高敏革No ratings yet

- Equity ResearchDocument4 pagesEquity ResearchChandanNo ratings yet

- Deloitte Economic Outlook 2010Document40 pagesDeloitte Economic Outlook 20103bandhuNo ratings yet

- Bangalore Geography Loan DsaDocument39 pagesBangalore Geography Loan DsananiNo ratings yet

- TV Channels Smdfifzk PlusDocument1,479 pagesTV Channels Smdfifzk PlusWhys ComunicaçãoNo ratings yet

- Black & Decker CorporationDocument20 pagesBlack & Decker Corporationboseuttam1No ratings yet

- Chapter 7 - Consumers, Producers, and The Efficiency of MarketsDocument37 pagesChapter 7 - Consumers, Producers, and The Efficiency of MarketsDellon-Dale BennettNo ratings yet

- SAP SD Implementation Sample Question1Document4 pagesSAP SD Implementation Sample Question1Tapas KunduNo ratings yet

- Philippine Ports Authority Updates - Presentation by PPA General Manager Atty Jay SantiagoDocument5 pagesPhilippine Ports Authority Updates - Presentation by PPA General Manager Atty Jay SantiagoPortCallsNo ratings yet

- Maruti Suzuki India LimitedDocument11 pagesMaruti Suzuki India LimitedAnurag SinghNo ratings yet

- Honda vs. TvsDocument100 pagesHonda vs. Tvsavnish100% (2)

- Overall Trends in IT Spending by IndustryDocument262 pagesOverall Trends in IT Spending by Industrynaveenkumarvr0% (1)

- Print Amortization Schedule CalculatorDocument1 pagePrint Amortization Schedule Calculatorsbb anbwNo ratings yet

- GH Purchase BillsDocument4 pagesGH Purchase BillsNavneet SoniNo ratings yet

- GS DDM Fair Value ModelDocument20 pagesGS DDM Fair Value ModelthiagopalaiaNo ratings yet

- Consumer's EquilibriumDocument4 pagesConsumer's EquilibriumMahendra ChhetriNo ratings yet

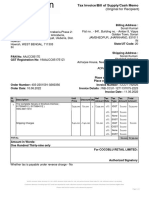

- InvoiceDocument1 pageInvoiceT SeriesNo ratings yet

- ISO 19901-5 - Weight ManagementDocument88 pagesISO 19901-5 - Weight ManagementH Anime100% (1)

- QuotationsDocument1 pageQuotationsArvinNo ratings yet

- The Post Office Act, 1898Document131 pagesThe Post Office Act, 1898Rizwan Niaz Raiyan100% (2)

- De Beer by PatelDocument12 pagesDe Beer by Patelgunnidheepatel100% (1)

- Chapter 9 The Indian Emergency - Aesthetics of State Control by Ashish Rajadhyaksha, 2008Document24 pagesChapter 9 The Indian Emergency - Aesthetics of State Control by Ashish Rajadhyaksha, 2008oahmed5100% (1)