You might also like

- Accounting Practices in Bangladesh: A Study On Kazi FarmsDocument19 pagesAccounting Practices in Bangladesh: A Study On Kazi FarmsMehedi HasanNo ratings yet

- Taxation Management Notes Tax Year 2020Document61 pagesTaxation Management Notes Tax Year 2020Ramsha ZahidNo ratings yet

- Special Audit of Sugar MillsDocument2 pagesSpecial Audit of Sugar MillsZoyaNo ratings yet

- Principle of Auditing AssignmentDocument6 pagesPrinciple of Auditing AssignmentranjinikpNo ratings yet

- MCQs On Transfer PricingDocument16 pagesMCQs On Transfer PricingRaksha JagatapNo ratings yet

- Job Order Costing FINALDocument11 pagesJob Order Costing FINALmannu.abhimanyu3098No ratings yet

- The Cost of Trade CreditDocument4 pagesThe Cost of Trade CreditWawex DavisNo ratings yet

- CA IPCC Cost Accounting Theory Notes On All Chapters by 4EG3XQ31Document50 pagesCA IPCC Cost Accounting Theory Notes On All Chapters by 4EG3XQ31Bala RanganathNo ratings yet

- Advanced Taxation Novmock2019 PDFDocument13 pagesAdvanced Taxation Novmock2019 PDFAndy AsanteNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- SLM-BCom-CORPORATE ACCOUNTING PDFDocument188 pagesSLM-BCom-CORPORATE ACCOUNTING PDFROHITH R MENON100% (1)

- Tax Assignment 1Document16 pagesTax Assignment 1Tunvir Islam Faisal100% (2)

- ICAI - ICMAI - ICSI - Branch Accounting PDFDocument5 pagesICAI - ICMAI - ICSI - Branch Accounting PDFRowdy RahulNo ratings yet

- CA INTER Direct Tax CASE BASED MCQs For MAY & NOV 21 by CA CS VijayDocument127 pagesCA INTER Direct Tax CASE BASED MCQs For MAY & NOV 21 by CA CS VijayHarleen Kaur0% (1)

- Auditing in BangladeshDocument60 pagesAuditing in Bangladeshaspire5572wxmi79% (24)

- Accounting For LabourDocument10 pagesAccounting For LabourTaleem Tableeg100% (1)

- Acn 305 Final AssignmentDocument17 pagesAcn 305 Final AssignmentRich KidNo ratings yet

- Job Order CostingDocument4 pagesJob Order CostingBrooke CarterNo ratings yet

- Tally Model Question PaperDocument2 pagesTally Model Question PaperMahaveer Choudhary100% (1)

- Chapter 18 OverheadsDocument23 pagesChapter 18 OverheadsAkash PatilNo ratings yet

- TdsDocument22 pagesTdsFRANCIS JOSEPHNo ratings yet

- Ma Chapter 3 Standard Costing - LabourDocument60 pagesMa Chapter 3 Standard Costing - LabourMohd Zubair KhanNo ratings yet

- Material CostingDocument20 pagesMaterial Costingrafiq5002No ratings yet

- Break Even Practice Class QuestionsDocument7 pagesBreak Even Practice Class QuestionsÃhmed AliNo ratings yet

- Yunus TextileDocument10 pagesYunus TextileSaba RizwanNo ratings yet

- Question (Apr 2012)Document49 pagesQuestion (Apr 2012)Monirul IslamNo ratings yet

- Fintax Bangladesh (Bejoy) Prepared by Excel Withholding Return Sec-177 of ITA-2023Document16 pagesFintax Bangladesh (Bejoy) Prepared by Excel Withholding Return Sec-177 of ITA-2023abu taher0% (1)

- Hypothesis Testing in Stata PDFDocument9 pagesHypothesis Testing in Stata PDFMarisela FuentesNo ratings yet

- 824 Ques Bank Mahesh Gour SirDocument143 pages824 Ques Bank Mahesh Gour SirRupesh JhanwarNo ratings yet

- Corporate Accounting AssignmentDocument6 pagesCorporate Accounting AssignmentKarthikacauraNo ratings yet

- Sir Saud Tariq: 13 Important Revision Questions On Each TopicDocument29 pagesSir Saud Tariq: 13 Important Revision Questions On Each TopicShehrozST100% (1)

- ICAB Last Year Question (Knowledge Level)Document5 pagesICAB Last Year Question (Knowledge Level)Fatema KanizNo ratings yet

- Edu-Care Professional Academy:, 243, Sundaram Coplex, Bhanwerkuan Main Road, IndoreDocument10 pagesEdu-Care Professional Academy:, 243, Sundaram Coplex, Bhanwerkuan Main Road, IndoreCA Gourav Jashnani100% (1)

- HMC Balance Sheet - Honda Motor Company, LTD PDFDocument2 pagesHMC Balance Sheet - Honda Motor Company, LTD PDFPoorvi JainNo ratings yet

- Cost and Management Accounting CIA 1.1Document5 pagesCost and Management Accounting CIA 1.1Kanika BothraNo ratings yet

- 7 Finalnew Sugg June09Document17 pages7 Finalnew Sugg June09mknatoo1963No ratings yet

- Cost AccountingDocument43 pagesCost AccountingAmina QamarNo ratings yet

- Accounting StandardsDocument376 pagesAccounting StandardsVirat VishnuNo ratings yet

- Fcma MTQSDocument11 pagesFcma MTQSRoqayya Fayyaz100% (1)

- Economic CroppedDocument267 pagesEconomic CroppedHemanth Singh RajpurohitNo ratings yet

- MCS MatH QSTN NewDocument7 pagesMCS MatH QSTN NewSrijita SahaNo ratings yet

- Bangladesh Financial Standards ReportDocument10 pagesBangladesh Financial Standards Reportmd. mofasser ahamed shaibal100% (1)

- Advance TaxDocument11 pagesAdvance TaxAdv Aastha MakkarNo ratings yet

- Tally Unit - 1Document10 pagesTally Unit - 1muni100% (1)

- Final Accounts With Adjustments - Principles of AccountingDocument9 pagesFinal Accounts With Adjustments - Principles of AccountingAbdulla Maseeh100% (1)

- Accounting Standards For NGOsDocument34 pagesAccounting Standards For NGOsMudassir IjazNo ratings yet

- 4 Sem Bcom - Cost AccountingDocument54 pages4 Sem Bcom - Cost Accountingraja chatterjeeNo ratings yet

- P-II - 2 - Advanced Accounting (Revised)Document2 pagesP-II - 2 - Advanced Accounting (Revised)Syeda AiniNo ratings yet

- Chapter 3 SolutionsDocument72 pagesChapter 3 SolutionsAshishpal SinghNo ratings yet

- Accounting Past MCQDocument108 pagesAccounting Past MCQbinalamitNo ratings yet

- FSA Course Pack Before Mid Balance Sheet PDFDocument16 pagesFSA Course Pack Before Mid Balance Sheet PDFRehman RajpootNo ratings yet

- Annual Repot 2021-22Document110 pagesAnnual Repot 2021-22Md. Ibrahim KhalilNo ratings yet

- Auditing As Profession in BangladeshDocument22 pagesAuditing As Profession in BangladeshIshan_Bhowmik33% (3)

- University of Jahangir Nagar: Institute of Business AdministrationDocument7 pagesUniversity of Jahangir Nagar: Institute of Business Administrationtabassum tasnim SinthyNo ratings yet

- University of Jahangir Nagar: Institute of Business AdministrationDocument7 pagesUniversity of Jahangir Nagar: Institute of Business Administrationtabassum tasnim SinthyNo ratings yet

- Evolution of Auditing-FullDocument4 pagesEvolution of Auditing-FullAhmad AnsariNo ratings yet

- Standard Accounting PracticesDocument41 pagesStandard Accounting PracticesSaudamini SinghNo ratings yet

- 1959 - Yasir Arafat - T&a Assignment 1Document8 pages1959 - Yasir Arafat - T&a Assignment 1Yasir ArafatNo ratings yet

- Lecture 1 Introduction To Auditing 21.11.2023Document37 pagesLecture 1 Introduction To Auditing 21.11.2023Bhawna KumariNo ratings yet

- Contemporary Issues in Accounting Mid 01 Solution Section BDocument10 pagesContemporary Issues in Accounting Mid 01 Solution Section BSALMA AKTER JUMANo ratings yet

- CH 1 Word CostDocument7 pagesCH 1 Word CostSellihom TadesseNo ratings yet

- A Term Paper On Jamuna Bank Ltd.Document64 pagesA Term Paper On Jamuna Bank Ltd.Rozina Akter Rea50% (2)

- AnswersDocument6 pagesAnswersKaren CubalitNo ratings yet

- Finland Tax SystemDocument4 pagesFinland Tax SystemHitesh ChintuNo ratings yet

- TASCO-NopticeOfProspectus (69KB)Document1 pageTASCO-NopticeOfProspectus (69KB)Gs KwangNo ratings yet

- How To Get A Background Check and Credit Report On Anyone !: This SiteDocument3 pagesHow To Get A Background Check and Credit Report On Anyone !: This Sitewindo polaNo ratings yet

- Stephanie Schneider BK 11 Filing 20-22398, (D.E. 36-4)Document165 pagesStephanie Schneider BK 11 Filing 20-22398, (D.E. 36-4)larry-612445No ratings yet

- Recto LawDocument6 pagesRecto LawJenniferPizarrasCadiz-CarullaNo ratings yet

- Punjabi University Patiala FM Assignment - N BDocument8 pagesPunjabi University Patiala FM Assignment - N BVishvesh GargNo ratings yet

- Negative Interest Rate Policies NIRP-Sources and ImplicationsDocument24 pagesNegative Interest Rate Policies NIRP-Sources and ImplicationsADBI EventsNo ratings yet

- A New Approach To Measure Financial ContagionDocument57 pagesA New Approach To Measure Financial ContagionAhmedNo ratings yet

- Guide To Investing in Treasury Bills in GhanaDocument1 pageGuide To Investing in Treasury Bills in GhanaSimon SimbakkyNo ratings yet

- Black Book ProjectDocument49 pagesBlack Book Projectshubham hanbarNo ratings yet

- Sample Estate Tax ProblemDocument14 pagesSample Estate Tax ProblemAiza MadumNo ratings yet

- Internship Report MCB Marketing Virtual University VUDocument82 pagesInternship Report MCB Marketing Virtual University VUKhurram_Rao_210475% (8)

- TCS AssignmentDocument9 pagesTCS AssignmentSupriya Gunthey RanadeNo ratings yet

- Ahmedabad Municipal Corporation Mahanagar Sevasadan Form 3Document1 pageAhmedabad Municipal Corporation Mahanagar Sevasadan Form 3Jugal PrajapatiNo ratings yet

- RENT AGREEMENT FormatDocument2 pagesRENT AGREEMENT Formatkaushal sharmaNo ratings yet

- Saurabh Mishra Mini Project 2 Report MBA 2nd Semester 2 1Document50 pagesSaurabh Mishra Mini Project 2 Report MBA 2nd Semester 2 1Akash KatiyarNo ratings yet

- 2130 E BRIARLEAF Ave, RedfinDocument1 page2130 E BRIARLEAF Ave, RedfinKrystal MNo ratings yet

- Final Preboard ExamsDocument5 pagesFinal Preboard ExamsRandy PaderesNo ratings yet

- Suarez, Francis - FORM 1 - 2009 PDFDocument3 pagesSuarez, Francis - FORM 1 - 2009 PDFal_crespoNo ratings yet

- Fractal Trading System 196Document5 pagesFractal Trading System 196Ajit Mishra50% (2)

- Deed of Assignment Shares - TemplateDocument3 pagesDeed of Assignment Shares - TemplateHomer Lopez Pablo100% (1)

- Presentation To The Danish Society For Construction and Consulting LawDocument48 pagesPresentation To The Danish Society For Construction and Consulting LawManish Gupta100% (4)

- Balakrishnan MGRL Solutions Ch05Document67 pagesBalakrishnan MGRL Solutions Ch05deeNo ratings yet

- Revaluation UUCMS - Unified University College Management SystemDocument2 pagesRevaluation UUCMS - Unified University College Management SystemMateen PathanNo ratings yet

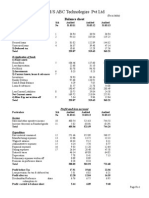

- Balance Sheet of M/S ABC Technologies PVT LTDDocument3 pagesBalance Sheet of M/S ABC Technologies PVT LTDSmitha RajNo ratings yet

- D0683SP Ans2Document18 pagesD0683SP Ans2Tanmay SanchetiNo ratings yet

- Adhar Address Update - Document-List - SSUPDocument1 pageAdhar Address Update - Document-List - SSUPDhanraj PatilNo ratings yet